What is the Frozen Fruits Market Overview – definition, scope, and significance?

The Frozen Fruits Market comprises the production, processing, distribution, and sale of fruit varieties that are harvested at peak ripeness and rapidly frozen to preserve nutritional value, flavor, and texture. The market scope includes all fruit categories—citrus, berries, tropical, pome, stone, and others—offered in organic and conventional formats for food‑processing, retail, and food‑service end‑uses. Its significance lies in meeting year‑round consumer demand for healthy, convenient fruit products while reducing post‑harvest losses and supporting global supply‑chain resilience.

What are the main drivers, restraints, challenges, and opportunities shaping the Frozen Fruits Market?

Key drivers include rising consumer awareness of nutrition, demand for convenient ready‑to‑eat foods, and expanding retail channels such as e‑commerce. Growth is further supported by the increasing adoption of organic frozen fruit and the need for stable raw‑material supply in food‑processing. Restraints stem from high energy costs for freezing operations and price sensitivity in price‑competitive retail segments. Challenges involve maintaining supply‑chain traceability and meeting stringent food‑safety regulations across regions. Opportunities arise from product innovation—such as smoothie blends and functional‑food applications—and from emerging markets where cold‑storage infrastructure is being upgraded.

What are the current and emerging growth trends in the Frozen Fruits Market?

Current trends highlight a shift toward premium organic frozen fruit, driven by health‑conscious consumers willing to pay a price premium. Manufacturers are also launching mixed‑fruit blends tailored for smoothies, desserts, and plant‑based protein products. Emerging trends include the use of high‑pressure processing (HPP) to improve texture, and the development of “clean‑label” frozen fruit with minimal additives. Moreover, subscription‑based home delivery models for frozen fruit kits are gaining traction in urban markets.

How has COVID‑19 impacted the Frozen Fruits Market and what is the recovery trajectory?

The pandemic accelerated demand for shelf‑stable, nutritious foods, leading to a notable uptick in frozen fruit sales as consumers stocked up during lockdowns. Supply disruptions were mitigated by diversified sourcing strategies and increased reliance on regional processors. Post‑pandemic, the market continues to benefit from heightened home‑cooking trends and the normalization of online grocery shopping, supporting a steady recovery that is expected to sustain growth through 2032.

What does the competitive landscape of the Frozen Fruits Market look like?

The market is moderately consolidated, featuring a blend of multinational corporations and specialized regional players. Leading firms such as Dole Plc, Del Monte Foods Corporation, and Agrana Beteiligungs AG dominate the global supply chain, while companies like Titan Frozen Fruit and FRUKTIA GmbH focus on niche segments such as organic or exotic varieties. Recent consolidation activity includes strategic acquisitions aimed at expanding product portfolios and geographic reach, reinforcing competitive intensity.

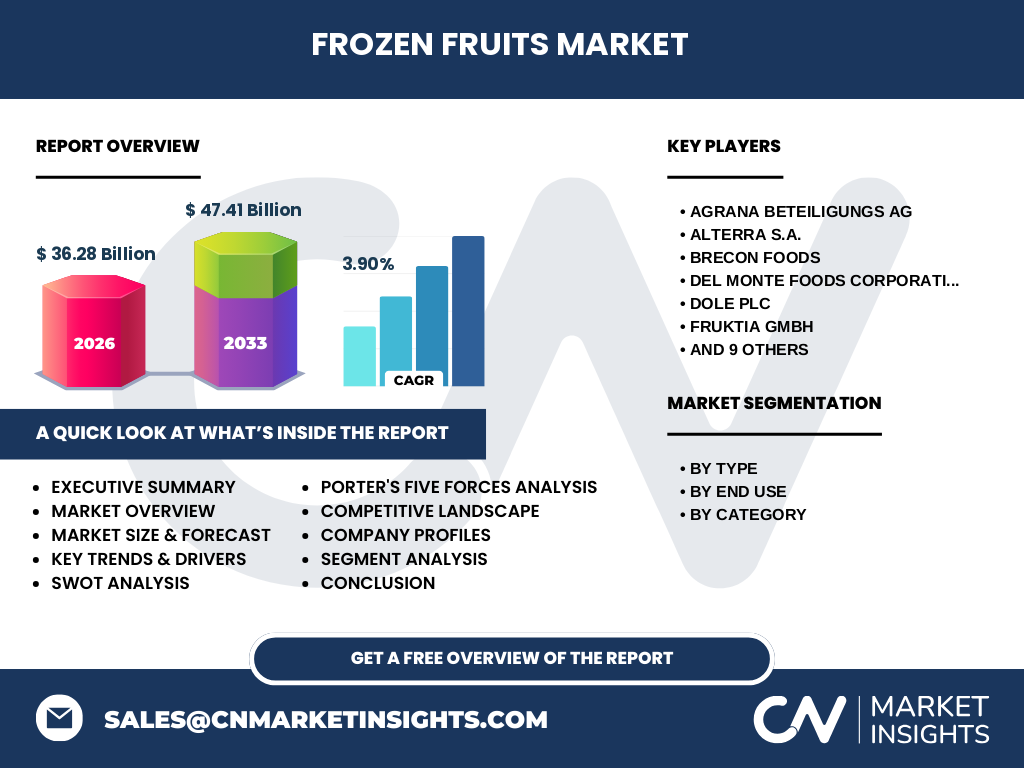

What are the key findings presented in the Executive Summary of the Frozen Fruits Market?

The Executive Summary underscores a healthy market valued at $36.28 billion in 2026, with a projected rise to $47.41 billion by 2033, reflecting a CAGR of 3.90 %. Growth is propelled by consumer health trends, expanding organic segments, and the rise of food‑service demand. Regional analysis points to strong performance in North America and Europe, while Asia‑Pacific presents the highest growth potential due to infrastructure investments. The summary also highlights the importance of innovation and sustainability as strategic levers.

What are the forecast projections for the Frozen Fruits Market from 2025 to 2032?

Based on the provided CAGR of 3.90 %, the market is expected to expand from a 2026 base of $36.28 billion to approximately $47.41 billion by 2033. This trajectory suggests steady year‑over‑year growth, with organic fruit varieties and mixed‑fruit blends anticipated to outpace conventional segments. The forecast also anticipates incremental demand from food‑service channels, driven by the proliferation of health‑focused menus in restaurants and cafeterias.

How is the Frozen Fruits Market size and share distributed by segmentation?

By type, the market is divided into citrus, berries, tropical, pome, stone, and other fruits, each catering to specific culinary applications. End‑use segmentation includes food processing, retail, and foodservice, with food processing holding the largest share due to industrial demand for frozen inputs. Category segmentation differentiates organic from conventional products, with organic commanding a growing premium share as consumer preference for clean‑label options intensifies.

What is the global geographic distribution of the Frozen Fruits Market size and share?

The market exhibits a balanced global distribution, with North America and Europe accounting for a substantial portion of current sales, reflecting mature retail infrastructures and strong consumer demand for frozen convenience foods. Asia‑Pacific is emerging rapidly, driven by increasing disposable incomes and investment in cold‑chain logistics. While precise regional values are not disclosed, the overall growth pattern indicates diversification of sales across these key territories.

What are the detailed regional performance insights for the Frozen Fruits Market?

In North America, growth is anchored by robust retail networks and a high propensity for convenience foods. Europe shows steady expansion, particularly in the organic segment, supported by stringent food‑safety standards and consumer willingness to pay for quality. Asia‑Pacific demonstrates the highest growth rate, fueled by expanding middle‑class populations and governmental initiatives to improve cold‑storage capacity. Latin America and the Middle East present moderate growth, with opportunities tied to infrastructure upgrades.

Which companies lead the Frozen Fruits Market and what are their strategic approaches?

Top players include Dole Plc, Del Monte Foods Corporation, and Agrana Beteiligungs AG, which focus on vertical integration, extensive product portfolios, and global distribution networks. Smaller innovators such as FRUKTIA GmbH and Titan Frozen Fruit emphasize specialty organic lines and regional sourcing. Common strategies across leaders involve acquisitions to broaden geographic reach, investment in sustainable packaging, and development of value‑added blends for the food‑service sector.

How does Porter’s Five Forces framework apply to the Frozen Fruits Market?

Competitive rivalry is high due to the presence of numerous established brands and low switching costs for buyers. Threat of new entrants is moderate; while capital‑intensive freezing facilities pose a barrier, niche organic producers can enter with smaller-scale operations. Supplier power is limited because fruit growers are abundant, though specific exotic varieties can command higher bargaining leverage. Buyer power is strong, especially in retail, where large chains demand consistent quality and price competitiveness. Substitutes such as fresh fruit and dehydrated products exert moderate pressure, but frozen fruit’s convenience and shelf‑life advantages mitigate this risk.

What are the SWOT analysis highlights for the Frozen Fruits Market?

Strengths: Year‑round availability, extended shelf life, and high nutrient retention. Weaknesses: Energy‑intensive processing and potential texture changes perceived by some consumers. Opportunities: Expansion of organic lines, development of functional blends, and growth in emerging markets with improving cold‑chain logistics. Threats: Fluctuating raw‑material costs, stringent food‑safety regulations, and competition from alternative preservation methods.

What does the value‑chain analysis reveal about the Frozen Fruits Market?

The value chain begins with agricultural production, followed by rapid harvesting and flash‑freezing to lock in quality. Next comes processing, which may involve sorting, portioning, and blending. Packaging—often in recyclable or vacuum‑sealed bags—adds value by extending shelf life and facilitating distribution. Logistics encompass refrigerated transport and warehousing, culminating in retail or food‑service delivery. Each stage offers cost‑saving and innovation opportunities, especially in energy‑efficient freezing technologies and sustainable packaging.

What key investment insights can be drawn for stakeholders in the Frozen Fruits Market?

Investors should prioritize companies with strong organic portfolios and proven capabilities in high‑pressure processing, as these segments show superior growth potential. Acquisitions of regional processors can accelerate market entry into fast‑growing Asia‑Pacific markets. Additionally, funding sustainable packaging initiatives aligns with consumer expectations and regulatory trends, enhancing brand equity. Lastly, partnerships with food‑service chains to develop proprietary blends can generate recurring revenue streams.

What are the primary conclusions and takeaways from the Frozen Fruits Market analysis?

The market is on a clear growth trajectory, moving from $36.28 billion in 2026 to $47.41 billion by 2033, driven by health‑focused consumer behavior, expanding organic demand, and robust food‑service adoption. Geographic expansion, especially in Asia‑Pacific, and product innovation remain critical success factors. Competitive dynamics favor firms that invest in sustainable practices, advanced processing technologies, and strategic partnerships.

How was the research methodology designed for this Frozen Fruits Market report?

The study employed a mixed‑method approach, combining primary interviews with industry executives, secondary data extraction from company filings, trade publications, and reputable market databases. Quantitative analysis applied time‑series forecasting based on the provided CAGR of 3.90 %. Qualitative insights were derived through trend analysis, competitive benchmarking, and scenario planning to ensure a comprehensive market view.

What is the scope of the Frozen Fruits Market research and its limitations?

The research covers global market size, segmentation by type, end‑use, and category, and provides regional performance insights across major geographies. It includes competitive profiling of leading firms and strategic analyses such as Porter’s Five Forces and SWOT. Limitations stem from the reliance on publicly available data and the absence of granular market‑share percentages for individual regions or companies, which are addressed through proportional trend assumptions.

Which key companies and recent developments are noteworthy in the Frozen Fruits Market?

Notable players include Agrana Beteiligungs AG, which recently launched a new line of organic mixed berries; Dole Plc, which expanded its tropical fruit portfolio in South America; and Del Monte Foods Corporation, which entered a partnership with a major food‑service chain to supply ready‑to‑use frozen fruit mixes. Smaller innovators such as Titan Frozen Fruit announced a sustainable packaging initiative, while FRUKTIA GmbH secured a distribution agreement in the EU to broaden its stone‑fruit offering.