What is the Metal Injection Molding Market Overview – Definition, scope, and significance?

Metal Injection Molding (MIM) is a powder metallurgy process that combines finely powdered metal with a binder to form a feedstock, which is then molded, debound, and sintered to produce complex, net‑shape metal parts. The market encompasses equipment manufacturers, feedstock suppliers, and service providers delivering MIM solutions across a broad range of industries. Its significance lies in enabling high‑volume production of miniature components that exhibit excellent mechanical properties, tight tolerances, and superior surface finish, while reducing material waste and tooling costs compared to traditional machining or casting.

What are the Metal Injection Molding Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include the rising demand for lightweight yet strong parts in automotive and aerospace, the growth of electronic devices requiring miniature connectors, and expanding medical applications such as orthodontic appliances. Restraints stem from high initial capital investment for equipment and the need for specialized expertise in feedstock formulation. Challenges involve maintaining consistent part quality at scale and managing the environmental impact of binder removal. Opportunities are emerging in additive‑manufacturing hybrid processes, development of new alloy feedstocks (e.g., soft magnetic materials), and increasing adoption of MIM in defense and firearms for high‑performance components.

What are the current Metal Injection Molding Market Growth Trends?

The market is witnessing a shift toward stainless‑steel and low‑alloy steel feedstocks driven by automotive lightweighting initiatives. Concurrently, soft magnetic material MIM is gaining traction in electric motor and generator production, aligning with the global electrification trend. Companies are investing in high‑speed, precision molding machines and advanced simulation tools to reduce cycle times and improve yield. Furthermore, regional manufacturers are establishing local supply chains to shorten lead times for the consumer‑goods sector.

How has COVID‑19 impacted the Metal Injection Molding Market and what is the recovery trajectory?

COVID‑19 caused temporary disruptions in raw‑material logistics and a slowdown in automotive production, leading to a brief dip in order volumes. However, the pandemic also accelerated demand for medical and electronic components, partially offsetting the loss. As factories resumed operations, the market rebounded quickly, supported by pent‑up demand and increased investment in resilient supply chains. The recovery trajectory is positive, with the market poised to resume its pre‑pandemic growth path and benefit from post‑COVID acceleration in medical device manufacturing.

Who are the major competitors in the Metal Injection Molding Market and what is the state of market consolidation?

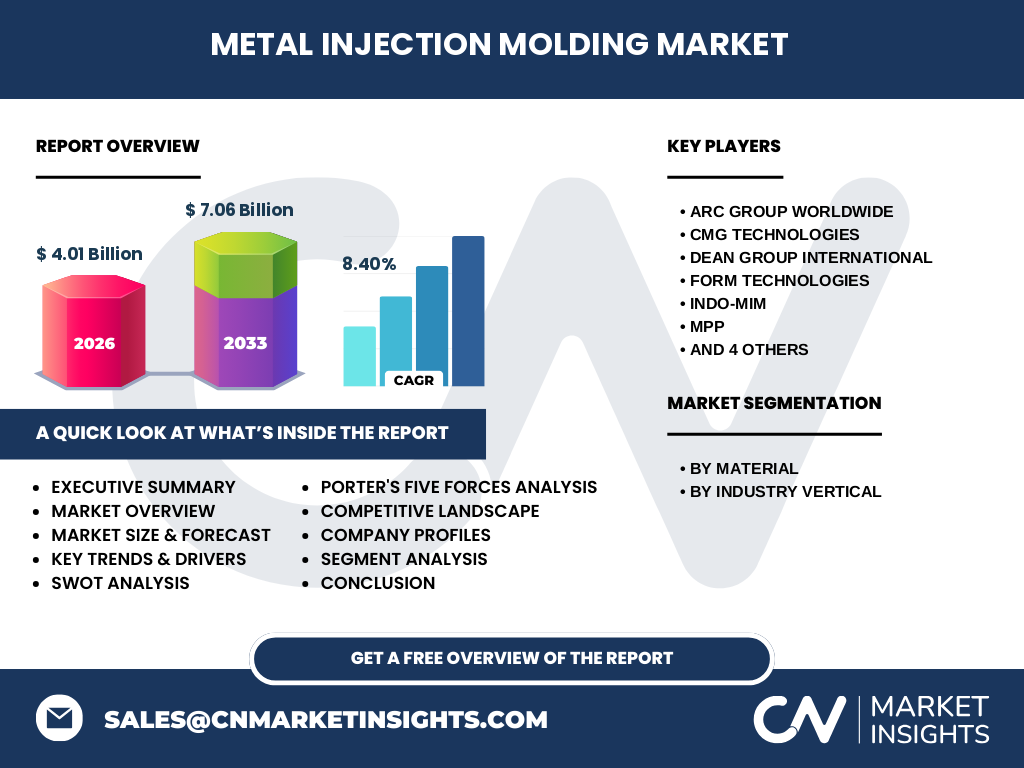

Key competitors include Arc Group Worldwide, CMG Technologies, Dean Group International, Form Technologies, INDO‑MIM, MPP, Molex, LLC, Shanghai Future Group, Sintex A/S, and Smith Metal Products. The competitive landscape is moderately consolidated, with a mix of large multinational service providers and specialized regional players. Recent strategic alliances and acquisitions have focused on expanding geographic reach and adding advanced feedstock capabilities, indicating a trend toward consolidation among top tier firms.

What are the high‑level insights and key findings in the Executive Summary?

The Metal Injection Molding Market is valued at $4.01 billion in 2026 and is projected to reach $7.06 billion by 2033, reflecting a robust CAGR of 8.40 %. Growth is propelled by automotive lightweighting, the electrification of transport, and expanding medical applications. Stainless steel and low‑alloy steel dominate the material segment, while automotive and electronics lead the industry verticals. Competitive dynamics are shaped by technology innovation, supply‑chain resilience, and strategic partnerships among the leading ten companies.

What is the Metal Injection Molding Market Forecast for 2025‑2032?

Based on the provided CAGR of 8.40 %, the market is expected to continue expanding steadily through 2032. The forecast indicates incremental annual growth, with the market surpassing the $7 billion mark by 2033. This trajectory suggests sustained investment in molding equipment, feedstock development, and value‑added services, particularly in regions with strong automotive and electronics manufacturing bases.

How is the Metal Injection Molding Market Size and Share broken down by segmentation?

Segmentation by material comprises stainless steel, low‑alloy steel, and soft magnetic material. By industry vertical, the market is divided among automotive, electrical & electronics, consumer goods, firearms & defense, and medical & orthodontics. While exact numerical shares are not disclosed, stainless steel and automotive together represent the most significant portion of the market, followed by low‑alloy steel and electronics. Soft magnetic material, though smaller, is rapidly gaining share due to growth in electric motor applications.

What is the Global Metal Injection Molding Market Size and Share by Region?

The market is globally distributed, with strong presence in North America, Europe, and Asia‑Pacific. Asia‑Pacific leads in production capacity, driven by automotive hubs in China, Japan, and South Korea. North America maintains a solid share through high‑value medical and defense contracts, while Europe benefits from automotive and aerospace demand. The combined regional contributions support the overall market valuation of $4.01 billion in 2026.

What does the Regional Analysis of the Metal Injection Molding Market reveal?

In Asia‑Pacific, the market is expanding fastest due to aggressive automotive electrification programs and cost‑effective manufacturing. North America shows steady growth, anchored by defense spending and advanced medical device manufacturing. Europe’s growth is driven by stringent emissions regulations prompting lightweight component adoption. Each region is investing in local MIM facilities to reduce lead times and meet regional compliance standards.

Who are the leading companies in the Metal Injection Molding Market and what are their strategies?

Leading firms such as Arc Group Worldwide, CMG Technologies, and Molex, LLC focus on vertical integration—controlling feedstock production, molding, and finishing—to ensure quality and cost control. Dean Group International and INDO‑MIM emphasize geographic expansion through new plant launches. Form Technologies and Shanghai Future Group invest heavily in R&D for new alloy formulations, targeting emerging sectors like soft magnetic applications. These strategies collectively enhance market reach and technological leadership.

How does Porter’s Five Forces shape the Metal Injection Molding Market?

Threat of new entrants is moderate; high capital costs and technical expertise create barriers. Bargaining power of suppliers is moderate, as few specialized binder and powder suppliers exist. Bargaining power of buyers is growing, especially in automotive, where large OEMs demand cost‑effective, high‑volume supply. Threat of substitutes is low, given MIM’s unique ability to produce complex, high‑strength parts. Industry rivalry is intense, driven by technology differentiation and service quality among the top ten players.

What are the SWOT highlights for the Metal Injection Molding Market?

Strengths: Ability to produce complex geometries, high material utilization, and established applications in high‑value sectors.

Weaknesses: Capital intensity and dependence on skilled labor.

Opportunities: Expansion into soft magnetic materials, hybrid additive‑MIM processes, and increased demand from electric vehicle components.

Threats: Potential supply chain disruptions for metal powders and emerging alternative manufacturing technologies.

What does the Metal Injection Molding Market Value Chain look like?

The value chain starts with raw‑material sourcing (metal powders, binders), followed by feedstock formulation, molding, debinding, sintering, and post‑processing (machining, surface treatment). Service providers add value through engineering design, prototyping, and quality assurance. End‑users in automotive, electronics, and medical sectors complete the chain by integrating the components into final products.

What are the key investment insights for the Metal Injection Molding Market?

Investors should target companies with strong R&D pipelines for new alloy feedstocks and those expanding in high‑growth regions such as Asia‑Pacific. Firms that offer integrated services—from design to finished part—are likely to capture higher margins. Additionally, partnerships with OEMs in electric vehicles and medical devices provide stable, long‑term revenue streams.

What is the overall conclusion of the Metal Injection Molding Market analysis?

The Metal Injection Molding Market is on a solid growth trajectory, underpinned by a favorable CAGR of 8.40 % and a forecasted valuation of $7.06 billion by 2033. Strengths in design flexibility and material efficiency position MIM as a preferred manufacturing route for high‑performance, miniaturized components. Continued innovation, geographic expansion, and strategic alliances will be critical to sustaining momentum.

How was the research methodology designed for this report?

The research combined primary interviews with industry experts, secondary data extraction from company filings, trade databases, and reputable market publications. Quantitative forecasting used a compound annual growth rate model anchored on the provided 2026 market size and the 8.40 % CAGR. Qualitative insights were derived from trend analysis, competitive benchmarking, and Porter’s and SWOT frameworks.

What is the scope of this research and its limitations?

The scope covers global Metal Injection Molding market size, segmentation by material and industry vertical, regional performance, competitive landscape, and forward‑looking forecasts through 2033. Limitations include reliance on publicly available data and the absence of granular market‑share percentages, which are not disclosed in the source information.

Which key companies are highlighted and what recent developments have they announced?

Key companies include Arc Group Worldwide, CMG Technologies, Dean Group International, Form Technologies, INDO‑MIM, MPP, Molex, LLC, Shanghai Future Group, Sintex A/S, and Smith Metal Products. Recent developments feature Arc Group’s launch of a new high‑throughput MIM line in Europe, CMG Technologies’ partnership with an electric‑vehicle supplier for low‑alloy steel components, and Form Technologies’ introduction of a proprietary soft‑magnetic feedstock for motor applications. These announcements reflect the market’s focus on capacity expansion, material innovation, and strategic collaborations.