What is the South and Central America Genomics Market Overview – definition, scope, and significance?

The South and Central America Genomics Market encompasses the development, production, and deployment of genomic technologies—including sequencing, microarrays, PCR, and nucleic‑acid extraction—in research centers, hospitals, clinics, and pharmaceutical/biotechnology firms across the region. Its scope covers instruments, consumables, and related services applied to diagnostics, drug discovery, precision medicine, and agricultural research. The market is significant because it underpins advances in personalized healthcare, improves disease‑control strategies, and drives biotechnological innovation that can boost regional economic growth.

What are the market drivers, restraints, challenges, and opportunities in South and Central America?

Key drivers include rising demand for precision medicine, increasing government funding for biomedical research, and expanding biotech ecosystems in Brazil, Mexico, and Argentina. Restraints stem from limited reimbursement frameworks and high capital costs for advanced sequencers. Challenges involve fragmented regulatory environments and a shortage of skilled genomics professionals. Opportunities arise from growing agricultural genomics, public‑private partnerships, and the rollout of low‑cost portable sequencing platforms that can serve remote populations.

What growth trends are shaping the South and Central America Genomics Market?

Current trends feature a shift toward next‑generation sequencing (NGS) over traditional Sanger methods, accelerated adoption of cloud‑based bioinformatics, and integration of genomics with AI for predictive diagnostics. Emerging trends include the use of CRISPR‑based diagnostics, increased focus on microbiome sequencing for personalized nutrition, and the expansion of genomics services into tele‑health platforms, especially in underserved rural areas.

How has COVID‑19 impacted the South and Central America Genomics Market and what is the recovery trajectory?

The pandemic highlighted the value of rapid genomic surveillance, prompting urgent investments in sequencing capacity for SARS‑CoV‑2 variant tracking. While elective research projects slowed in 2020, governmental stimulus and collaborations with international health agencies accelerated infrastructure upgrades. Recovery is now strong, with a renewed emphasis on pandemic preparedness and a spill‑over effect that boosts downstream applications such as oncology and infectious‑disease diagnostics.

Who are the major competitors and what is the consolidation landscape in the South and Central America Genomics Market?

Dominant players include Illumina, Inc., Thermo Fisher Scientific Inc., QIAGEN, BIO‑RAD Laboratories Inc., Danaher, F. Hoffmann‑La Roche Ltd., and General Electric Company. The market has seen strategic mergers and acquisitions, such as Illumina’s acquisition of smaller NGS service firms and Thermo Fisher’s expansion of its consumables portfolio. Consolidation is driven by the need to offer end‑to‑end solutions that combine instruments, reagents, and data‑analysis services.

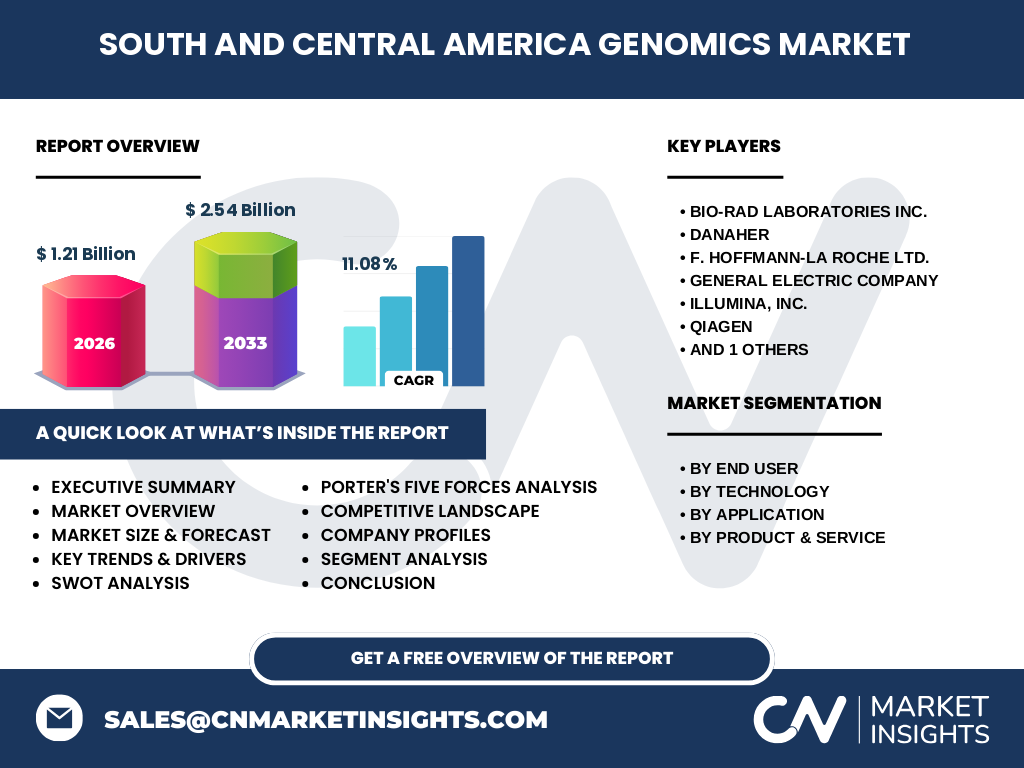

What are the key findings in the executive summary of the South and Central America Genomics Market?

The market is valued at USD 1.21 billion in 2026 and is projected to reach USD 2.54 billion by 2033, delivering a CAGR of 11.08 %. Growth is powered by expanding research activities, rising clinical adoption of genomics, and increasing public‑sector support. Competitive dynamics favor integrated solution providers, while emerging applications in agriculture and personalized medicine present high‑margin opportunities.

What are the forecast projections for the South and Central America Genomics Market from 2025 to 2032?

Based on the provided CAGR of 11.08 %, the market is expected to continue expanding steadily through 2032, maintaining double‑digit growth each year. The forecast reflects sustained investment in infrastructure, growing demand for NGS‑based diagnostics, and expanding biotech pipelines that require genomic data. Stakeholders can anticipate robust revenue streams across instruments, consumables, and services.

How is the market size and share divided by segmentation?

By end‑user, research centers command the largest share, followed by hospitals and clinics, and then pharmaceutical & biotechnology companies. Technology segmentation shows sequencing as the dominant segment, with microarray, PCR, and nucleic‑acid extraction each holding smaller but growing portions. Application‑wise, diagnostics leads, while drug discovery, precision medicine, and agriculture & animal research each contribute progressively larger shares as the market matures. Product‑service segmentation is led by instruments/systems, with consumables and services providing complementary revenue streams.

What is the geographic distribution of the South and Central America Genomics Market?

The market is primarily concentrated in Brazil, Mexico, and Argentina, which together host the majority of research institutions, hospitals, and biotech firms. Secondary markets include Chile, Colombia, and Peru, where emerging agricultural genomics projects are gaining traction. While exact regional share percentages are not disclosed, the overall regional outlook remains positive due to supportive policy frameworks and growing private investment.

What does the regional analysis reveal about market performance?

Brazil leads with the highest absolute spend on sequencing platforms and a strong pipeline of genomics‑driven drug programs. Mexico shows rapid growth in hospital‑based diagnostic genomics, driven by private health networks. Argentina’s research centers are expanding microarray and PCR capabilities for agricultural genomics. Smaller economies are benefiting from regional collaborations and shared sequencing facilities, which help offset high capital expenditures.

What are the profiles of leading companies operating in the market?

Illumina, Inc. dominates with its NGS platforms and a broad consumables catalogue. Thermo Fisher Scientific Inc. offers a complete suite of instruments, reagents, and services, emphasizing integration. QIAGEN focuses on sample‑prep and molecular testing kits. BIO‑RAD Laboratories Inc. supplies PCR and microarray solutions for both clinical and research settings. Danaher, F. Hoffmann‑La Roche Ltd., and General Electric Company contribute complementary technologies and diagnostics that enhance overall market depth.

How does Porter’s Five Forces model apply to the South and Central America Genomics Market?

Threat of new entrants is moderate due to high capital requirements and regulatory barriers. Supplier power is relatively high because a few global manufacturers control critical components such as high‑throughput sequencers. Buyer power is increasing as hospitals and research institutions negotiate bulk pricing for consumables. The risk of substitutes remains low, given the unique value of genomic data. Competitive rivalry is intense, with firms competing on technology innovation, cost, and service ecosystems.

What are the SWOT observations for the market?

Strengths: Robust growth potential, strong scientific talent pool, and rising healthcare expenditure. Weaknesses: High upfront costs and fragmented reimbursement policies. Opportunities: Expansion into agricultural genomics, development of low‑cost portable sequencers, and growth of tele‑genomics services. Threats: Economic volatility in some countries, potential supply‑chain disruptions for high‑precision components, and evolving data‑privacy regulations.

What does the value‑chain analysis reveal about the industry structure?

The value chain starts with R&D of core sequencing and detection technologies, followed by manufacturing of instruments and consumables. Next comes distribution through regional distributors and direct sales to research centers and hospitals. Service layers—bioinformatics, data storage, and analysis—add high‑margin value, while end‑users generate revenue through diagnostics, drug development, and agricultural applications. Partnerships across the chain are increasingly common to accelerate time‑to‑market.

What key investment insights can be drawn for stakeholders?

Investors should prioritize companies offering integrated platforms that bundle hardware, reagents, and analytics, as these generate recurring revenue. Funding opportunities exist in niche segments such as portable sequencing for field diagnostics and genomics‑enabled crop improvement. Strategic M&A targeting regional service providers can accelerate market penetration, while public‑sector grants provide low‑risk capital for expanding sequencing capacity in under‑served areas.

What are the main conclusions of the market analysis?

The South and Central America Genomics Market is on a strong growth trajectory, driven by rising demand for precision health and biotechnology innovation. With a projected market size of USD 2.54 billion by 2033 and an 11.08 % CAGR, the region offers attractive opportunities for technology providers, consumable manufacturers, and service firms. Success will depend on navigating regulatory environments, delivering cost‑effective solutions, and leveraging partnerships to broaden access.

How was the research methodology conducted?

The study combined primary interviews with industry experts, surveys of leading laboratories, and secondary data from government reports, financial statements, and reputable market databases. Quantitative forecasts were derived using CAGR calculations based on the 2026 baseline of USD 1.21 billion and the 2033 target of USD 2.54 billion. Qualitative insights stemmed from trend analysis, competitive benchmarking, and scenario planning.

What is the scope of the research and its limitations?

The research covers the entire South and Central America region, focusing on end‑users, technologies, applications, and product‑service categories defined in the brief. Limitations include the unavailability of country‑level revenue breakdowns and the exclusion of informal market activity. The analysis does not project currency fluctuations or macro‑economic shocks beyond the provided CAGR.

Which key companies have recent developments in the South and Central America Genomics Market?

Illumina, Inc. announced a partnership with a Brazilian university to establish a national NGS core facility. Thermo Fisher Scientific launched a new low‑cost sequencer tailored for diagnostic labs in Mexico. QIAGEN introduced a rapid‑prep kit for agricultural samples, targeting Argentine growers. BIO‑RAD Laboratories expanded its PCR product line in Chile. Danaher and GE Healthcare announced joint workshops on integrating genomics data with imaging technologies across the region.