What is the Enterprise Labelling Software Market Overview – definition, scope, and significance?

The Enterprise Labelling Software Market comprises solutions that enable organizations to design, generate, print, and manage product labels across complex supply chains. It spans software platforms, associated services, and deployment models (cloud or on‑premise) tailored for various enterprise sizes. The market is significant because accurate labeling ensures regulatory compliance, enhances traceability, reduces errors, and supports brand consistency in high‑volume sectors such as FMCG, healthcare, and manufacturing.

What are the key drivers, restraints, challenges, and opportunities influencing the Enterprise Labelling Software Market?

Key drivers include heightened regulatory scrutiny, the rise of automated warehouses, and the need for real‑time data integration. Restraints stem from legacy system inertia and high upfront costs for large deployments. Challenges involve data security concerns in cloud environments and the complexity of multi‑language label requirements. Opportunities arise from AI‑enhanced label verification, IoT‑linked barcode systems, and expanding demand in emerging markets seeking digital transformation.

Which growth trends are currently shaping the Enterprise Labelling Software Market?

Current trends feature a shift toward cloud‑based platforms for scalability, increased adoption of AI for error detection, and integration with ERP and WMS solutions. Emerging trends include low‑code label designers that empower business users, subscription‑based pricing models, and the use of blockchain for immutable label provenance, especially in pharma and food safety.

How did COVID‑19 impact the Enterprise Labelling Software Market and what is the recovery trajectory?

The pandemic accelerated digital adoption as companies needed remote label management and fast‑track supply‑chain visibility. Demand surged for cloud solutions that support distributed workforces. Post‑COVID, the market has continued its upward trajectory, benefitting from renewed investment in automation and the ongoing shift to e‑commerce, which demands accurate, compliant labeling at speed.

Who are the major competitors in the Enterprise Labelling Software Market and how is the competitive landscape evolving?

Leading players include CYBRA Corporation, Loftware Inc, Zebra Technologies Corp, and Esko‑Graphics BV, among others. The landscape is marked by strategic partnerships, acquisitions of niche AI startups, and expanding service portfolios. Consolidation is evident as larger firms acquire specialized labeling vendors to broaden end‑to‑end offering and lock in enterprise contracts.

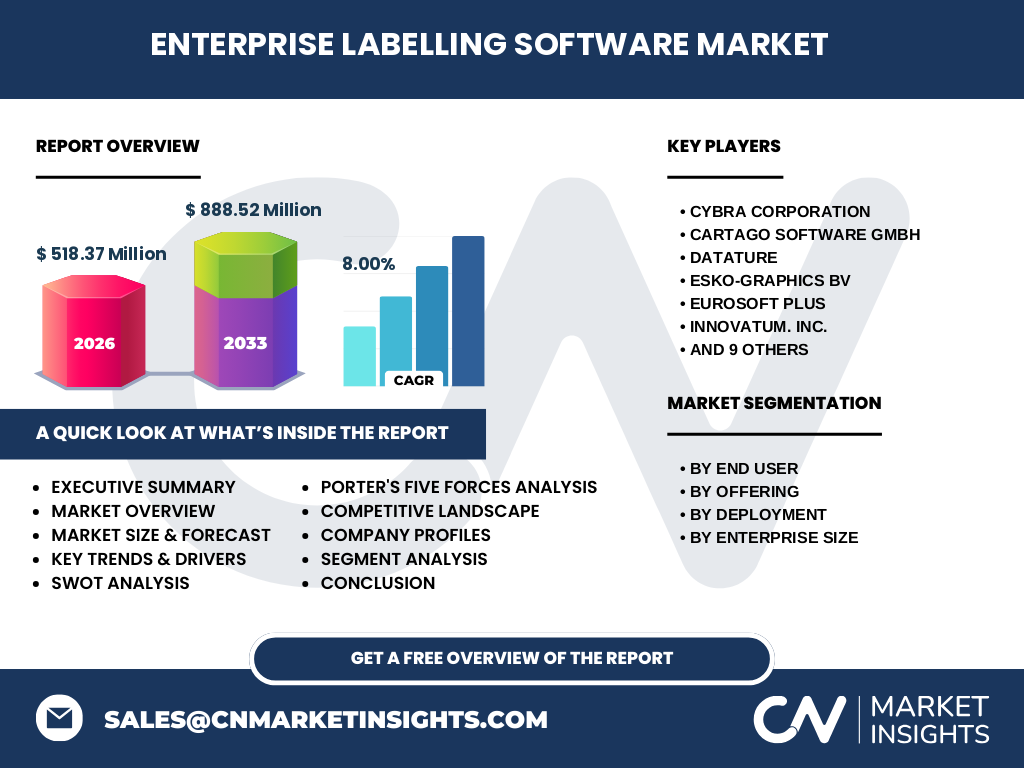

What are the key findings in the Executive Summary of the Enterprise Labelling Software Market?

The market is projected to grow from a 2026 size of $518.37 million to $888.52 million by 2033, reflecting an 8 % CAGR. Growth is driven by digital transformation, regulatory pressure, and the need for integrated label management across multiple end users. Cloud deployment is gaining share, while large enterprises dominate spend, though SMEs are rapidly adopting SaaS models.

What are the forecast expectations for the Enterprise Labelling Software Market for 2025‑2032?

Based on the 8 % annual growth rate, the market is expected to expand steadily each year, reaching near $900 million by the early 2030s. The forecast anticipates continued acceleration in cloud adoption, higher penetration in healthcare and logistics, and incremental revenue from value‑added services such as AI validation and analytics.

How is the Enterprise Labelling Software Market sized and shared by segmentation?

Segmentation by end user shows strong demand from FMCG and retail, followed by healthcare, warehousing and logistics, automotive, manufacturing, and others. By offering, software accounts for the majority of spend, while services add a complementary revenue stream for implementation and support. Deployment splits between cloud and on‑premise, with cloud gaining momentum. Enterprise size segmentation reveals larger revenues from large enterprises, with growing SaaS uptake among small and medium businesses.

What is the global geographic distribution of the Enterprise Labelling Software Market?

The market exhibits a worldwide footprint, with North America and Europe leading due to mature regulatory frameworks and advanced supply‑chain automation. Asia‑Pacific is emerging rapidly as manufacturers digitalize operations, while Latin America and the Middle East show modest but steady adoption, driven by expanding consumer goods sectors.

What are the detailed regional performances in the Enterprise Labelling Software Market?

In North America, high compliance standards in healthcare and food drive adoption. Europe’s strong emphasis on traceability sustains demand, especially in automotive and pharma. Asia‑Pacific’s growth is fueled by large‑scale manufacturing hubs and rising e‑commerce. Latin America sees incremental uptake as retail chains modernize, while the Middle East benefits from logistics hubs investing in smart labeling.

Which companies lead the Enterprise Labelling Software Market and what strategies are they pursuing?

Key leaders—CYBRA Corporation, Loftware Inc, Zebra Technologies Corp, and Esko‑Graphics BV—focus on expanding cloud portfolios, acquiring AI‑focused firms, and forming alliances with ERP providers. Others such as Cartago Software GmbH and Innovatum Inc. differentiate through niche vertical solutions and robust service networks. Across the board, firms are increasing R&D spending to embed analytics and IoT connectivity.

How does Porter’s Five Forces model apply to the Enterprise Labelling Software Market?

Threat of new entrants is moderate due to high development costs and the need for regulatory expertise. Bargaining power of buyers is rising as enterprises demand integrated, scalable solutions. Supplier power is low because most components are software‑based. Threat of substitutes remains limited; alternative manual processes are inefficient. Industry rivalry is intense, driven by innovation, pricing models, and service differentiation.

What are the SWOT insights for the Enterprise Labelling Software Market?

Strengths: Critical role in compliance, strong integration with supply‑chain systems. Weaknesses: Complex implementation and reliance on legacy infrastructure in some segments. Opportunities: AI‑driven validation, blockchain traceability, expansion into emerging economies. Threats: Cybersecurity risks of cloud deployments and potential regulatory changes that could reshape requirements.

How is the value chain structured in the Enterprise Labelling Software Market?

The value chain begins with software development and R&D, followed by integration services, deployment (cloud or on‑premise), and ongoing support. Upstream, data providers supply product master data, while downstream, end users generate printed or digital labels. Ancillary services—training, compliance audits, and analytics—add value and create recurring revenue streams.

What investment insights can be drawn for stakeholders in the Enterprise Labelling Software Market?

Investors should target companies with strong cloud platforms, AI capabilities, and proven integration with major ERP systems. Partnerships with logistics and IoT providers can unlock new revenue channels. Acquiring niche AI or blockchain startups offers fast entry into high‑growth sub‑segments. Emphasis on recurring SaaS revenue models reduces risk and improves cash flow.

What are the concluding takeaways for the Enterprise Labelling Software Market?

The market is on a robust growth path, propelled by regulatory demand and digital supply‑chain initiatives. Cloud adoption and AI‑enhanced validation are reshaping the competitive arena. Companies that invest in integrated, secure, and scalable solutions are positioned to capture the expanding $888.52 million forecasted market by 2033.

Which research methodology was employed to compile this Enterprise Labelling Software Market report?

The study combined primary interviews with industry executives, secondary data from company filings, market databases, and regulatory sources. Market sizing used a top‑down approach anchored on the 2026 baseline of $518.37 million, applying the disclosed 8 % CAGR for forward projections. Segmentation analysis leveraged vendor product portfolios and end‑user adoption surveys.

What is the scope of this research and any defined limitations?

The scope covers global market dynamics, segmentation by end user, offering, deployment, and enterprise size, and regional performance across major continents. It focuses on the period 2025‑2032 and utilizes only the provided financial figures. While comprehensive, the analysis does not quantify regional market shares beyond qualitative trends.

Who are the key companies and what recent developments have they announced?

Prominent firms include CYBRA Corporation, Cartago Software GmbH, Datature, Esko‑Graphics BV, Eurosoft Plus, Innovatum Inc., Kallik Ltd, Loftware Inc, MHC Automation, OPAL ASSOCIATES HOLDING AG, Seagull Software LLC, SuperAnnotate AI Inc., TKX Corp SAS, ValuTrack Corporation, and Zebra Technologies Corp. Recent activities feature Loftware’s launch of a cloud‑first label suite, Zebra’s partnership with a logistics AI platform, and SuperAnnotate’s integration of computer‑vision labeling verification, illustrating a market shift toward intelligent, cloud‑based solutions.