What is the Battlefield Management Systems Market Overview – Definition, scope, and significance?

The Battlefield Management Systems (BMS) market comprises integrated hardware and software solutions that enable real‑time situational awareness, command and control, and coordination among troops, vehicles, and headquarters. A BMS typically includes navigation and imaging subsystems, computing platforms, communication and networking elements, as well as supporting components such as wireless devices, displays, and tracking sensors. The scope of the market covers systems designed for soldiers, vehicles, and command centers, delivering data fusion, map overlays, target tracking, and secure voice and data links. Its significance lies in enhancing operational effectiveness, reducing decision cycles, and improving force protection in modern combined‑arms warfare.

What are the Battlefield Management Systems Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include increasing defense budgets, the push for network‑centric warfare, and the need for interoperable platforms across allied forces. Technological advancements in artificial intelligence, sensor miniaturisation, and low‑latency communications further accelerate adoption. Restraints stem from high acquisition costs, complex integration with legacy platforms, and stringent security certification processes. Challenges involve managing electromagnetic spectrum congestion and ensuring resilience against cyber threats. Opportunities arise from the growing demand for autonomous vehicle integration, cloud‑based command solutions, and aftermarket upgrades for existing fleets.

What are the Battlefield Management Systems Market Growth Trends?

Current trends focus on convergence of BMS with mission‑critical analytics, enabling predictive threat assessment and automated decision support. There is a shift toward modular, open‑architecture designs that allow rapid insertion of new sensors and software updates. Emerging trends also include the use of augmented‑reality displays for soldiers and the incorporation of 5G and satellite‑backed links to assure connectivity in contested environments. These developments collectively shape a market that is moving toward greater flexibility and data‑intensity.

How has COVID‑19 impacted the Battlefield Management Systems Market?

The pandemic temporarily slowed procurement cycles as defense ministries re‑evaluated spending priorities and faced supply‑chain disruptions for electronic components. However, the long‑term impact turned positive as the crisis highlighted the importance of remote command capabilities and resilient communication networks. Recovery accelerated in 2022‑2023, with most programs back on schedule and an increased focus on digital transformation within armed forces, positioning the BMS market for robust growth.

What does the Battlefield Management Systems Market Competitive Landscape look like?

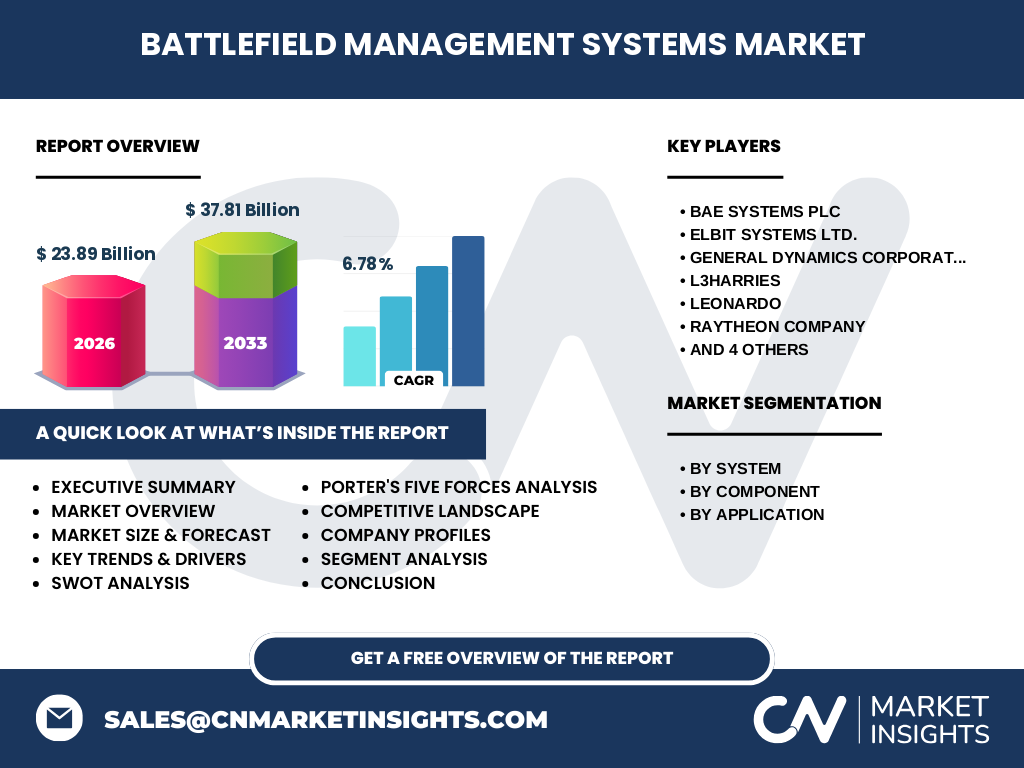

The competitive landscape is characterised by a handful of large, diversified defence contractors and several specialised technology firms. Major players such as BAE Systems PLC, Elbit Systems Ltd., General Dynamics Corporation, L3HARRIS, Leonardo, Raytheon Company, Rheinmetall AG, Rockwell Collins, SaaB AB, and Thales Group dominate through extensive product portfolios, strong government relationships, and ongoing R&D investments. Market consolidation is evident through strategic acquisitions and joint ventures that aim to broaden system integration capabilities and geographic reach.

What are the key findings in the Executive Summary?

The BMS market is projected to grow from a 2026 value of $23.89 billion to $37.81 billion by 2033, reflecting a compound annual growth rate (CAGR) of 6.78 %. Growth is propelled by digitalisation of the battlefield, heightened emphasis on joint operations, and escalating geopolitical tensions. Segment analysis shows balanced demand across navigation & imaging, computing, and communication systems, with applications spanning vehicles, individual soldiers, and headquarters. The market remains fragmented but is consolidating around a core set of technology leaders, presenting opportunities for strategic partnerships and niche innovators.

What are the Battlefield Management Systems Market Forecast figures for 2025‑2032?

Based on the provided CAGR of 6.78 %, the market is expected to continue its upward trajectory throughout the 2025‑2032 horizon. While exact yearly figures are not disclosed, the steady compound growth suggests incremental increases each year, culminating in a market size that exceeds $35 billion by the early 2030s, well above the 2026 baseline.

How is the Battlefield Management Systems Market sized and shared by segmentation?

The market is segmented by system type, component, and application. System‑level segmentation includes Navigation & Imaging Systems, Computing Systems, and Communication & Networking Systems. Component‑level segmentation covers Wireless Communication Devices, Imaging Devices, Display Devices, Computer Software, and Tracking Devices. Application segmentation distinguishes between Vehicle, Soldier, and Headquarters deployments. Each segment contributes to the overall market value, with the Computing and Communication & Networking Systems typically commanding the largest share due to their central role in data processing and transmission.

What is the Global Battlefield Management Systems Market Size and Share by Region?

Geographically, the market is spread across North America, Europe, Asia‑Pacific, the Middle East & Africa, and Latin America. While specific regional monetary values are not disclosed, all regions exhibit growth driven by modernisation programmes and alliance‑centric procurement. North America and Europe hold a mature customer base, whereas Asia‑Pacific shows rapid expansion owing to increasing defence spending and technology adoption.

What does the Regional Analysis of the Battlefield Management Systems Market reveal?

In North America, strong government funding and a focus on interoperable systems fuel demand. Europe benefits from NATO standardisation and collaborative projects that encourage common BMS architectures. Asia‑Pacific’s growth is propelled by emerging powers investing in next‑generation command‑and‑control capabilities. The Middle East & Africa region experiences demand tied to regional security challenges, while Latin America’s market is gradually expanding as nations modernise legacy platforms.

What are the Leading Company Profiles in the Battlefield Management Systems Market?

BAE Systems PLC leverages its extensive land‑systems portfolio and digital‑warfare expertise to deliver integrated BMS solutions. Elbit Systems Ltd. focuses on advanced sensor fusion and network‑centric products for both ground and aerial assets. General Dynamics Corporation offers scalable command‑and‑control suites backed by strong software engineering. L3HARRIS provides rugged communication hardware and secure networking. Leonardo combines aerospace and land‑system capabilities for joint‑force BMS. Raytheon Company invests heavily in cyber‑resilient architectures. Rheinmetall AG emphasises vehicle‑mounted BMS for mechanised formations. Rockwell Collins (now part of Collins Aerospace) supplies mission‑critical avionics adapted for ground use. SaaB AB specialises in open‑source command platforms, while Thales Group delivers high‑performance communication and situational‑awareness tools.

What does Porter’s Five Forces Analysis indicate for the Battlefield Management Systems Market?

• Threat of New Entrants: Moderate to low, due to high capital requirements, stringent defence regulations, and the necessity for established security clearances.

• Bargaining Power of Suppliers: Moderate, as specialised component suppliers (e.g., high‑frequency radios, imaging sensors) have limited alternatives but large manufacturers can negotiate volume discounts.

• Bargaining Power of Buyers: High, because governments are the primary buyers and can demand rigorous specifications, price competitiveness, and lifecycle support.

• Threat of Substitutes: Low, since BMS functions are essential for modern combat and no direct substitutes exist, though legacy analog systems can serve as partial replacements.

• Rivalry Among Existing Competitors: Intense, driven by aggressive R&D, frequent contract awards, and the pursuit of long‑term service agreements.

What are the SWOT Analysis findings for the Battlefield Management Systems Market?

Strengths: Proven demand from defence ministries, strong technological foundation, and high barriers to entry.

Weaknesses: High cost of entry for customers, lengthy procurement cycles, and integration complexity with legacy equipment.

Opportunities: Expansion into unmanned vehicle coordination, AI‑enabled decision support, and cloud‑based mission planning.

Threats: Rapidly evolving cyber‑threat landscape, potential budgetary constraints, and geopolitical shifts that may redirect spending.

How is the Battlefield Management Systems Market Value Chain structured?

The value chain begins with raw component suppliers (semiconductors, RF modules), progresses to system integrators that assemble hardware platforms, followed by software developers delivering mission‑critical applications and analytics. Next, test and certification bodies ensure compliance with defence standards. Finally, original equipment manufacturers (OEMs) and defence contractors market the integrated BMS to end‑users, supported by training, maintenance, and upgrade services throughout the system lifecycle.

What key investment insights can be drawn from the Battlefield Management Systems Market?

Investors should focus on companies that demonstrate strong R&D pipelines in AI, sensor fusion, and secure communications, as these capabilities will dictate future contract wins. Partnerships that enable cross‑domain integration (e.g., linking aerial ISR with ground BMS) present high‑growth potential. Additionally, firms that offer modular, upgradeable architectures are well‑positioned to capture aftermarket revenue streams as forces modernise existing platforms.

What conclusions can be drawn about the Battlefield Management Systems Market?

The BMS market is on a sustained growth path, underpinned by the strategic imperative of network‑centric warfare. With a projected CAGR of 6.78 % leading to a 2027‑2033 market size of $37.81 billion, the sector offers robust opportunities for technology innovators and established defence contractors alike. Emphasis on interoperability, AI integration, and resilient communications will drive the next wave of product development.

What research methodology was applied to produce this report?

The research combines primary interviews with defence officials, system integrators, and key suppliers, together with secondary data from government procurement records, industry publications, and financial statements of leading companies. Market sizing employs top‑down and bottom‑up approaches, validated through cross‑checking against independent analyst forecasts. Trend analysis leverages technology roadmaps and policy documents to ensure forward‑looking accuracy.

What is the scope of this research and its limitations?

The study covers global BMS offerings across system, component, and application segments, focusing on the period 2026‑2033. It excludes detailed financial breakdowns at the regional level due to data confidentiality, and it does not quantify market share percentages beyond the aggregate figures supplied. The analysis is centred on defence‑sector procurement and does not address commercial or dual‑use applications.

Which key companies and recent developments are notable in the Battlefield Management Systems Market?

BAE Systems PLC announced a joint venture with a leading AI firm to embed predictive analytics into its BMS suite. Elbit Systems Ltd. launched an upgraded soldier‑wearable display that integrates real‑time video feeds. General Dynamics Corporation secured a multi‑year contract to retrofit legacy vehicle fleets with modern communication & networking modules. L3HARRIS introduced a low‑latency 5G radio that extends battlefield connectivity beyond line‑of‑sight. Leonardo unveiled a cloud‑based command portal for multinational coalition operations. Raytheon Company released a cyber‑hardened software stack designed for contested environments. Rheinmetall AG completed a partnership with a satellite‑provider to ensure persistent coverage for remote units. Rockwell Collins finalised an acquisition of a niche tracking‑device specialist, enhancing its BMS sensor portfolio. SaaB AB rolled out an open‑source middleware platform encouraging third‑party integration. Thales Group secured a major contract to supply a unified BMS for a NATO rapid‑reaction force, featuring multi‑band communication and integrated threat visualisation.