1. What is the Antibody Discovery Market and why is it significant?

The Antibody Discovery Market encompasses all technologies, services, and solutions used to identify and develop therapeutic and diagnostic antibodies. Its scope includes platforms such as phage display, hybridoma, transgenic animal models, single‑cell screening, and yeast display, as well as the generation of humanized, chimeric, and murine antibodies. The market is significant because antibodies remain the dominant modality for treating cancer, autoimmune disorders, infectious diseases, and emerging pathogens, driving substantial R&D investment and clinical pipelines worldwide.

2. What are the main drivers, restraints, challenges, and opportunities shaping the Antibody Discovery Market?

Key drivers include rising prevalence of chronic and rare diseases, increasing biotech financing, and advances in high‑throughput screening that shorten discovery timelines. Restraints stem from high development costs, regulatory complexity, and the need for specialized expertise. Challenges involve escalating competition for novel epitopes and maintaining antibody stability and manufacturability. Opportunities arise from novel formats such as bispecifics, antibody‑drug conjugates, and AI‑enabled target identification, which expand the therapeutic landscape and open new revenue streams.

3. Which growth trends are currently influencing the Antibody Discovery Market?

Current trends feature a shift toward fully human and humanized antibodies to reduce immunogenicity, the integration of next‑generation sequencing for repertoire analysis, and the adoption of cloud‑based data platforms that accelerate candidate selection. Emerging trends include the use of microfluidics for single‑cell isolation, CRISPR‑engineered transgenic animals for diverse repertoires, and expanding collaborations between academic institutes and contract research organizations to de‑risk early discovery phases.

4. How did COVID‑19 affect the Antibody Discovery Market and what is the recovery trajectory?

COVID‑19 catalyzed rapid investment in antibody platforms for neutralizing SARS‑CoV‑2, boosting demand for phage‑display and single‑cell technologies. While many projects experienced temporary delays due to laboratory access restrictions, the pandemic also accelerated digital adoption, remote screening, and virtual collaborations. Post‑pandemic, the market is on a strong rebound, with sustained interest in pandemic preparedness and a broader pipeline of infectious‑disease antibodies reinforcing growth.

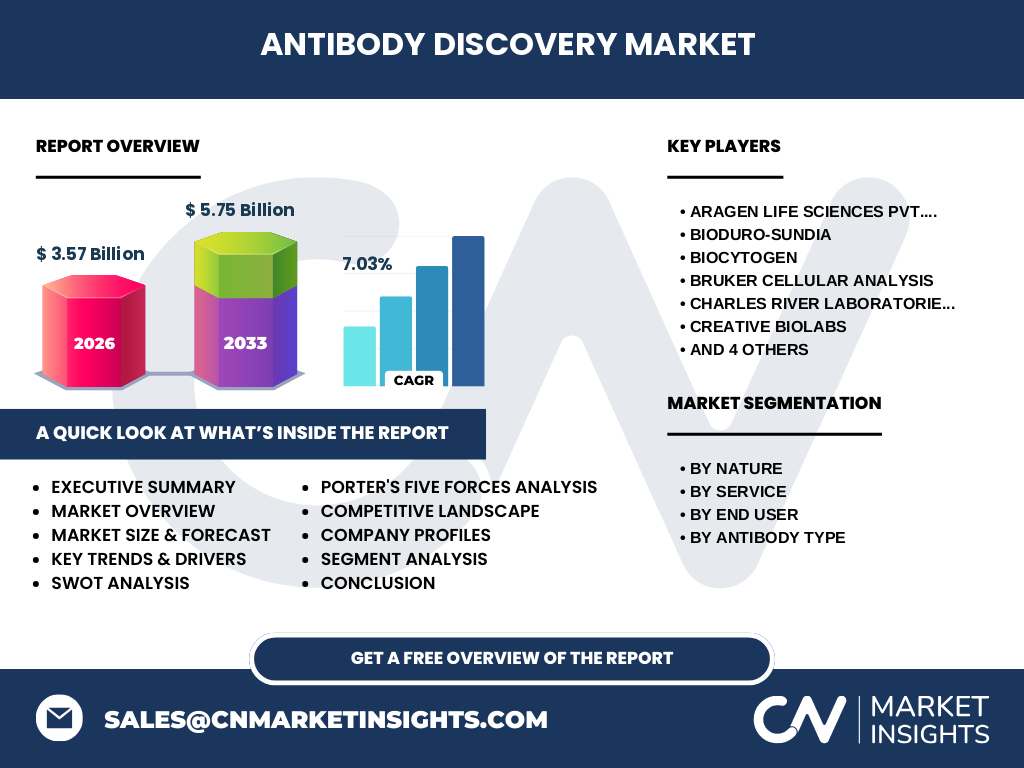

5. Who are the major competitors in the Antibody Discovery Market and how is the market consolidating?

Leading competitors include Aragen Life Sciences, BioDuro‑Sundia, Biocytogen, Bruker Cellular Analysis, Charles River Laboratories, Creative Biolabs, Evotec, NanoCellect Biomedical, Sartorius AG, and Twist Bioscience. Consolidation is occurring through strategic acquisitions of niche platform providers, joint ventures that combine screening capabilities with manufacturing expertise, and partnership agreements that extend geographic reach. This consolidation enhances service breadth while creating integrated value propositions for pharmaceutical and biotech customers.

6. What are the key take‑aways from the Executive Summary of the Antibody Discovery Market?

The market is valued at $3.57 billion in 2026 and is projected to reach $5.75 billion by 2033, reflecting a 7.03 % CAGR. Growth is propelled by expanding therapeutic indications, advanced discovery platforms, and increasing outsourcing to specialized service providers. Regional demand is strongest in North America and Europe, with Asia‑Pacific emerging rapidly. Competitive dynamics favor firms that combine technology breadth with data‑driven analytics, positioning them for long‑term leadership.

7. What are the forecast expectations for the Antibody Discovery Market from 2025 to 2032?

Based on the provided CAGR of 7.03 %, the market is expected to grow steadily, surpassing the $5.75 billion mark by 2033. This trajectory suggests a compound increase of roughly $0.5 billion per year, driven by ongoing adoption of high‑throughput platforms, rising biotech funding, and the expansion of antibody‑based therapies into new therapeutic areas such as neuro‑degeneration and rare genetic disorders.

8. How is the Antibody Discovery Market sized and shared across its primary segments?

Segmentation by nature divides the market into Human and Humanized, Chimeric, and Murine antibodies, reflecting the preference for reduced immunogenicity. Service‑based segmentation includes Phage Display, Hybridoma, Transgenic Animal, Single Cell, and Yeast Display, each contributing to the overall mix based on project requirements. End‑user segmentation separates Pharmaceutical & Biotechnology Companies from Research Laboratories, while antibody type splits the market between Monoclonal and Polyclonal antibodies. Together, these dimensions illustrate a diversified landscape where no single segment dominates, enabling service providers to target niche needs.

9. What is the geographic distribution of the Antibody Discovery Market?

The market’s global footprint is anchored by North America, which hosts a dense concentration of biotech hubs and leading research institutions. Europe follows closely, benefitting from robust public funding and regulatory frameworks supportive of biologics. Asia‑Pacific is emerging as a growth engine, driven by expanding pharmaceutical pipelines, increasing R&D expenditure, and government incentives for biologics innovation. These regions collectively shape the market’s revenue allocation.

10. How do regional markets perform within the Antibody Discovery sector?

North America leads in terms of absolute revenue, propelled by extensive clinical pipelines and high adoption of cutting‑edge platforms. Europe demonstrates strong performance through collaborative networks and a mature biotech ecosystem. Asia‑Pacific shows the highest growth rate, with countries such as China, India, and Japan investing heavily in antibody engineering capabilities and outsourcing services. The Middle East and Latin America present niche opportunities, primarily in contract research services.

11. Which companies are leading the Antibody Discovery Market and what strategies are they employing?

Aragen Life Sciences leverages an integrated platform combining AI‑driven target identification with downstream development. BioDuro‑Sundia focuses on scalable phage‑display libraries. Biocytogen expands its portfolio through strategic collaborations with pharma partners. Charles River Laboratories differentiates via end‑to‑end services from discovery to preclinical testing. Twist Bioscience emphasizes high‑throughput DNA synthesis for rapid antibody gene construction. Across the board, leaders pursue acquisitions, partnership models, and technology diversification to capture greater market share.

12. What does Porter’s Five Forces analysis reveal about the Antibody Discovery Market?

Threat of new entrants is moderate; high capital costs and technical expertise create barriers, yet contract research growth attracts niche players. Bargaining power of suppliers is low because key reagents and instruments are widely available from multiple vendors. Bargaining power of buyers is high, as large pharma and biotech firms demand cost‑effective, rapid discovery solutions. Threat of substitutes is limited; alternative modalities like small molecules cannot fully replace antibody specificity. Competitive rivalry is intense, driven by rapid innovation, IP battles, and service differentiation.

13. What are the SWOT attributes of the Antibody Discovery Market?

Strengths: Proven therapeutic efficacy, strong pipeline pipelines, and mature technology platforms. Weaknesses: High development costs and complex regulatory pathways. Opportunities: AI‑enabled discovery, bispecific and ADC formats, and expanding applications in infectious disease and rare disorders. Threats: Market saturation, emerging alternative biologics, and potential reimbursement pressures.

14. How is value created and transferred within the Antibody Discovery value chain?

The value chain starts with target identification, proceeds to library generation (phage, yeast, transgenic animal), followed by high‑throughput screening and lead optimization. Subsequent stages include candidate validation, preclinical testing, and hand‑off to manufacturing partners. Service providers add value at each node by offering specialized expertise, data analytics, and rapid turnaround, while end users (pharma/biotech) focus on clinical translation and commercialization.

15. What investment insights should stakeholders consider for the Antibody Discovery Market?

Investors should prioritize companies with diversified platform portfolios, strong IP positions, and established collaborations with major pharma players. Funding opportunities exist in AI‑driven discovery tools, single‑cell technologies, and emerging markets in Asia‑Pacific. Strategic investments in contract research organizations that provide end‑to‑end services can capture recurring revenue streams as outsourcing continues to rise.

16. What conclusions can be drawn from the Antibody Discovery Market analysis?

The Antibody Discovery Market is on a robust growth trajectory, underpinned by therapeutic demand, technological advances, and a supportive investment climate. While cost and regulatory complexities remain, the expansion of novel formats and digital tools creates a resilient outlook. Companies that integrate multiple discovery modalities and foster strategic alliances are best positioned to lead the market through 2033.

17. How was the research for this Antibody Discovery Market report conducted?

The study combined primary interviews with industry experts, secondary data from published market reports, company financial statements, and scientific literature. Trend analysis employed quantitative modeling based on the provided market size of $3.57 billion (2026) and the forecast of $5.75 billion (2033) with a 7.03 % CAGR. Competitive intelligence was gathered through press releases, patent filings, and partnership announcements.

18. What is the scope of this research and its limitations?

The scope covers global market sizing, segmentation by nature, service, end‑user, and antibody type, as well as regional performance, competitive landscape, and strategic analysis. Limitations include reliance on publicly available data, which may not capture confidential pipeline details, and the exclusion of granular regional revenue figures beyond the overarching geographic trends described.

19. Which key companies have made notable recent developments in the Antibody Discovery Market?

Aragen Life Sciences announced a partnership with a leading oncology biotech to co‑develop humanized antibodies using its AI platform. BioDuro‑Sundia launched an expanded phage‑display library targeting viral epitopes. Biocytogen disclosed a new bispecific antibody pipeline in collaboration with a European pharma firm. Charles River Laboratories introduced a fully integrated discovery‑to‑preclinical service suite. Twist Bioscience released a high‑throughput DNA synthesis platform that reduces antibody gene construction time by 30 %.