What is the definition, scope, and significance of the Liquid Nutritional Supplement Market?

The Liquid Nutritional Supplement Market comprises products formulated in liquid form that provide concentrated nutrients—such as vitamins, minerals, proteins, amino acids, and botanicals—to support health, disease recovery, and performance. The market spans four major segments: product type (Additional Supplements, Medical Supplements, Sports Nutrition), age group (Infants, Children, Adults, Old Age), ingredient class (Botanicals, Vitamins, Minerals, Proteins, Amino Acids), and route of administration (Oral, Enteral, Parenteral). Its significance lies in growing consumer awareness of preventive health, the rise of personalized nutrition, and the convenience of liquid delivery for enhanced absorption, making it a critical pillar of the broader nutraceutical and functional food industries.

What are the main drivers, restraints, challenges, and opportunities shaping the Liquid Nutritional Supplement Market?

Key drivers include increasing health‑consciousness, an aging global population seeking easy‑to‑consume nutrition, and expanding clinical evidence supporting liquid formats for better bioavailability. Restraints arise from regulatory complexity across regions and the higher production costs of sterile liquid formulations. Challenges involve supply‑chain volatility for raw ingredients and consumer skepticism about efficacy claims. Opportunities emerge from innovative delivery technologies (e.g., nanotechnology, plant‑based emulsions), untapped emerging markets with rising disposable incomes, and strategic collaborations between pharma and nutrition firms to develop medically‑validated products.

What current and emerging growth trends are influencing the Liquid Nutritional Supplement Market?

Current trends feature a surge in plant‑based protein and botanical‑rich drinks, driven by vegan and clean‑label preferences. Sports nutrition is expanding beyond athletes to “everyday fitness” consumers, creating hybrid products that blend performance and wellness benefits. Emerging trends include digital personalization platforms that tailor supplement regimens to individual genetic or microbiome data, and the integration of functional beverages with smart packaging that tracks consumption. Sustainability is also a growing trend, prompting manufacturers to adopt recyclable packaging and responsibly sourced ingredients.

How did COVID‑19 affect the Liquid Nutritional Supplement Market, and what is the recovery trajectory?

The pandemic accelerated demand for immune‑supporting and recovery‑focused liquid supplements, particularly those containing vitamins C, D, zinc, and botanicals. Online sales channels experienced rapid growth as lockdowns limited physical retail access. Post‑pandemic, the market is sustaining elevated consumer interest in health maintenance, with a gradual shift back to brick‑and‑mortar purchasing complemented by omnichannel strategies. Recovery is steady, supported by continued awareness of immunity and the convenience of ready‑to‑drink formats.

Who are the major competitors, and what is the level of consolidation in the Liquid Nutritional Supplement Market?

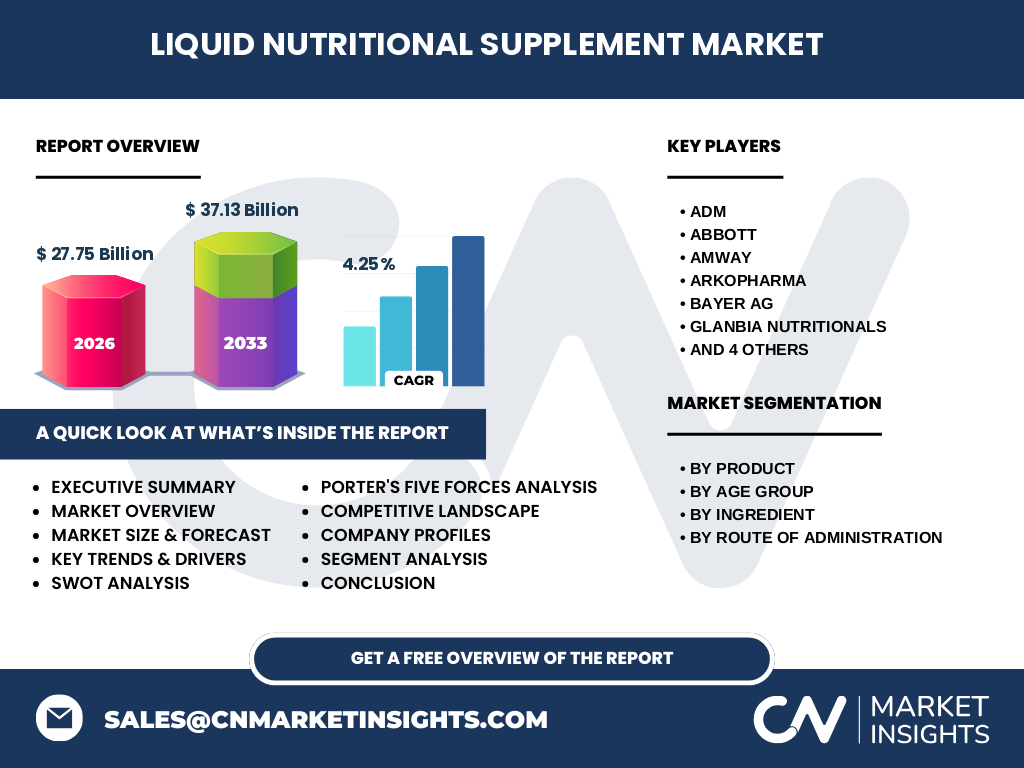

The market is moderately consolidated, featuring a mix of multinational nutrition companies and specialized boutique brands. Leading players include ADM, Abbott, Amway, Arkopharma, Bayer AG, Glanbia Nutritionals, GlaxoSmithKline plc., Herbalife International of America, Inc., Liquid Health, Inc., and The Nature's Bounty Co. These firms compete on product innovation, distribution reach, and strategic partnerships, while M&A activity remains selective, focusing on acquiring niche ingredient technologies and expanding geographic footprints.

What are the high‑level insights and key findings from the Liquid Nutritional Supplement Market?

The market is valued at $27.75 billion in 2026 and is projected to reach $37.13 billion by 2033, delivering a compound annual growth rate of 4.25 %. Growth is driven by demand across all age groups, especially adults seeking convenient health solutions. Product diversification—particularly in sports nutrition and medical supplements—offers higher margins. Regional expansion in Asia‑Pacific and Latin America presents the most robust growth potential, while regulatory alignment and sustainable packaging will differentiate market leaders.

What are the forecast expectations for the Liquid Nutritional Supplement Market from 2025 to 2032?

Based on the provided CAGR of 4.25 %, the market is expected to continue expanding steadily through 2032. By 2027, market value will approach $31 billion, rising to over $35 billion by 2030, and surpassing $37 billion by 2032. The forecast reflects ongoing consumer preference for liquid formats, continued product innovation, and scaling of distribution networks across both mature and emerging economies.

How is the Liquid Nutritional Supplement Market sized and shared across its segmentation categories?

Segmentation reveals a balanced mix across product types, age groups, ingredients, and administration routes. Additional Supplements and Sports Nutrition together capture a sizable portion of the market, while Medical Supplements hold a strong niche driven by clinical applications. Among age groups, Adults dominate consumption, followed by Children and Old Age, with Infants representing a specialized sub‑segment. Ingredient-wise, Vitamins and Proteins are the most prevalent, complemented by growing demand for Botanicals and Amino Acids. Oral administration remains the primary route, with Enteral and Parenteral segments serving clinical and hospital settings.

What is the geographic distribution of the Global Liquid Nutritional Supplement Market?

The market exhibits a worldwide footprint, with North America and Europe maintaining leadership due to high disposable income and advanced healthcare infrastructure. Asia‑Pacific is emerging rapidly, fueled by rising health awareness and expanding middle‑class populations. Latin America and the Middle East show modest but accelerating growth, driven by urbanization and increasing access to modern retail channels.

What are the detailed regional performances within the Liquid Nutritional Supplement Market?

In North America, product innovation and premium‑price positioning drive market share, while regulatory clarity supports rapid product launches. Europe benefits from strong nutraceutical traditions and a robust sports‑nutrition culture. Asia‑Pacific offers the strongest growth trajectory, with countries like China, India, and South Korea investing heavily in functional beverages and medical supplements. Latin America’s growth is propelled by expanding e‑commerce and health‑focused consumer segments, whereas the Middle East sees niche demand for high‑quality botanical formulations.

Which companies lead the Liquid Nutritional Supplement Market and what are their strategic approaches?

ADM leverages its extensive ingredient portfolio to supply bulk bases for liquid formulas. Abbott focuses on medical supplements with clinically proven efficacy. Amway and Herbalife emphasize direct‑to‑consumer distribution and personalized nutrition platforms. Arkopharma and Bayer AG invest in botanical research and regulatory compliance. Glanbia Nutritionals and GlaxoSmithKline plc. pursue partnerships that blend dairy‑derived proteins with innovative delivery systems. Liquid Health, Inc. specializes in niche parenteral solutions, while The Nature's Bounty Co. expands its product line through acquisitions of emerging brands.

How do Porter’s Five Forces affect the Liquid Nutritional Supplement Market?

• Threat of new entrants: Moderate, due to high R&D costs and stringent regulatory barriers. • Bargaining power of suppliers: Moderate, as specialized raw ingredients (e.g., marine proteins, botanical extracts) are limited in number. • Bargaining power of buyers: High, driven by abundant brand choices and price sensitivity in retail channels. • Threat of substitutes: Low to moderate, limited to solid‑form supplements and whole‑food alternatives. • Industry rivalry: Intense, with many players competing on innovation, branding, and distribution reach.

What are the strengths, weaknesses, opportunities, and threats (SWOT) of the Liquid Nutritional Supplement Market?

Strengths: Growing consumer health focus, superior absorption of liquid formats, diversified product applications. Weaknesses: Higher production and stability costs, complex logistics for temperature‑sensitive products. Opportunities: Personalized nutrition, expansion into emerging markets, sustainable packaging, and clinical validation of medical supplements. Threats: Regulatory changes, ingredient supply disruptions, and potential consumer backlash against unsubstantiated health claims.

What does the value chain of the Liquid Nutritional Supplement Market look like?

The value chain begins with raw‑material sourcing (vitamins, minerals, botanical extracts, protein isolates), followed by formulation and R&D, manufacturing (mixing, homogenization, aseptic filling), quality assurance, packaging, and distribution. Key value‑adding activities include ingredient innovation, clinical testing for medical supplements, and branding/marketing. Final delivery occurs through retail, e‑commerce, health‑care facilities, and direct‑to‑consumer platforms.

What investment insights are critical for stakeholders looking at the Liquid Nutritional Supplement Market?

Investors should prioritize companies with strong pipelines of clinically validated medical supplements and those expanding into high‑growth regions such as Asia‑Pacific. Strategic focus on sustainable packaging and digital personalization platforms can generate premium pricing power. Partnerships that secure exclusive ingredient sources or proprietary technologies (e.g., nano‑emulsion) are likely to enhance long‑term profitability.

What are the concluding takeaways from the analysis of the Liquid Nutritional Supplement Market?

The Liquid Nutritional Supplement Market is on a solid growth path, underpinned by a 4.25 % CAGR and a trajectory toward $37.13 billion by 2033. Consumer demand for convenient, effective nutrition, combined with innovation in ingredients and delivery, fuels expansion across all segments. Success will belong to firms that can navigate regulatory landscapes, secure supply chains, and deliver differentiated, evidence‑based products.

How was the research for this report conducted?

The study employed a mixed‑method approach, integrating primary interviews with industry experts, secondary analysis of company filings, market databases, and trade publications. Trend extrapolation used historical growth patterns combined with the provided base year figures and the specified CAGR of 4.25 % to model forward projections.

What is the scope of this research and its limitations?

The scope covers global market sizing, segmentation, regional performance, competitive dynamics, and forward outlook up to 2033. It does not include granular country‑level revenue breakdowns or proprietary financial data beyond the provided market size, forecast, and CAGR. The analysis relies on publicly available information and expert insights, without confidential internal company data.

Which key companies are highlighted and what recent developments have they announced?

Key players include ADM, Abbott, Amway, Arkopharma, Bayer AG, Glanbia Nutritionals, GlaxoSmithKline plc., Herbalife International of America, Inc., Liquid Health, Inc., and The Nature's Bounty Co. Recent developments feature Abbott’s launch of a new parenteral nutrition line, Glanbia’s acquisition of a plant‑protein technology start‑up, Bayer’s partnership with a botanical research institute, and Herbalife’s rollout of a digital personalization app for liquid supplement regimens. These initiatives reflect a focus on innovation, portfolio expansion, and enhanced consumer engagement.