In-vehicle Infotainment Market Overview - Definition, scope, and significance

In-vehicle infotainment (IVI) systems represent the convergence of entertainment, information, and communication technologies within automotive environments. These sophisticated systems integrate multiple functionalities including audio and video entertainment, navigation, connectivity features, and vehicle diagnostics into a unified interface. The scope of the IVI market encompasses hardware components such as displays, processors, and connectivity modules, as well as software platforms that manage user interfaces and applications. The significance of this market lies in its ability to enhance driver experience, improve safety through hands-free operations, and serve as a platform for future autonomous driving technologies. As vehicles become increasingly connected and intelligent, IVI systems have evolved from luxury features to essential components that influence purchasing decisions and brand differentiation in the automotive industry.

In-vehicle Infotainment Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The primary drivers of the IVI market include increasing consumer demand for connected vehicles, advancements in smartphone integration technologies, and the growing trend toward autonomous driving. Rising disposable incomes and the desire for enhanced driving experiences have accelerated adoption across both premium and mid-range vehicle segments. However, the market faces several restraints including high implementation costs, cybersecurity concerns, and the complexity of integrating multiple systems. Challenges such as driver distraction, regulatory compliance requirements, and the need for seamless cross-platform compatibility continue to impact market growth. Opportunities exist in the development of voice-activated controls, artificial intelligence integration, and personalized user experiences. The expansion of 5G networks and the emergence of electric vehicles present additional avenues for innovation and market expansion.

In-vehicle Infotainment Market Growth Trends - Current and emerging trends shaping the market

Current growth trends in the IVI market are characterized by the rapid adoption of touch-based interfaces, which dominate the interaction type segment. Voice-enabled systems are experiencing significant growth as manufacturers prioritize hands-free operation and safety. The market is witnessing a shift toward open-source operating systems, particularly Linux-based platforms, due to their flexibility and cost-effectiveness. Emerging trends include the integration of augmented reality displays, biometric authentication systems, and predictive maintenance features. The convergence of IVI systems with advanced driver assistance systems (ADAS) is creating new opportunities for enhanced functionality. Additionally, the trend toward over-the-air updates is enabling continuous improvement of system capabilities without requiring physical modifications to vehicles.

COVID-19 Impact on the In-vehicle Infotainment Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially disrupted the IVI market through supply chain interruptions, manufacturing slowdowns, and reduced consumer spending on automotive purchases. However, the crisis also accelerated certain trends, including the demand for contactless interfaces and enhanced connectivity features for remote work and entertainment. The recovery trajectory has been shaped by pent-up demand for vehicles, increased focus on personal mobility, and the accelerated adoption of digital technologies in automotive applications. Manufacturers have responded by streamlining their product offerings and focusing on cost-effective solutions that maintain premium features while addressing budget-conscious consumers. The pandemic has also highlighted the importance of robust connectivity infrastructure and the need for systems that can support both work and entertainment functions.

In-vehicle Infotainment Market Competitive Landscape - Major competitors and market consolidation

The IVI market features a mix of traditional automotive suppliers and technology companies competing for market share. Major players include Alpine Electronics, Clarion, Continental AG, Denso Ten Limited, Garmin, Harman International, JVC Kenwood, Panasonic, Pioneer, and Visteon Corporation. The competitive landscape is characterized by strategic partnerships between automotive manufacturers and technology providers, as well as ongoing consolidation through mergers and acquisitions. Companies are differentiating themselves through proprietary software platforms, exclusive content partnerships, and advanced user interface designs. The market has seen increased collaboration between hardware manufacturers and software developers to create integrated solutions that address both technical requirements and user experience expectations.

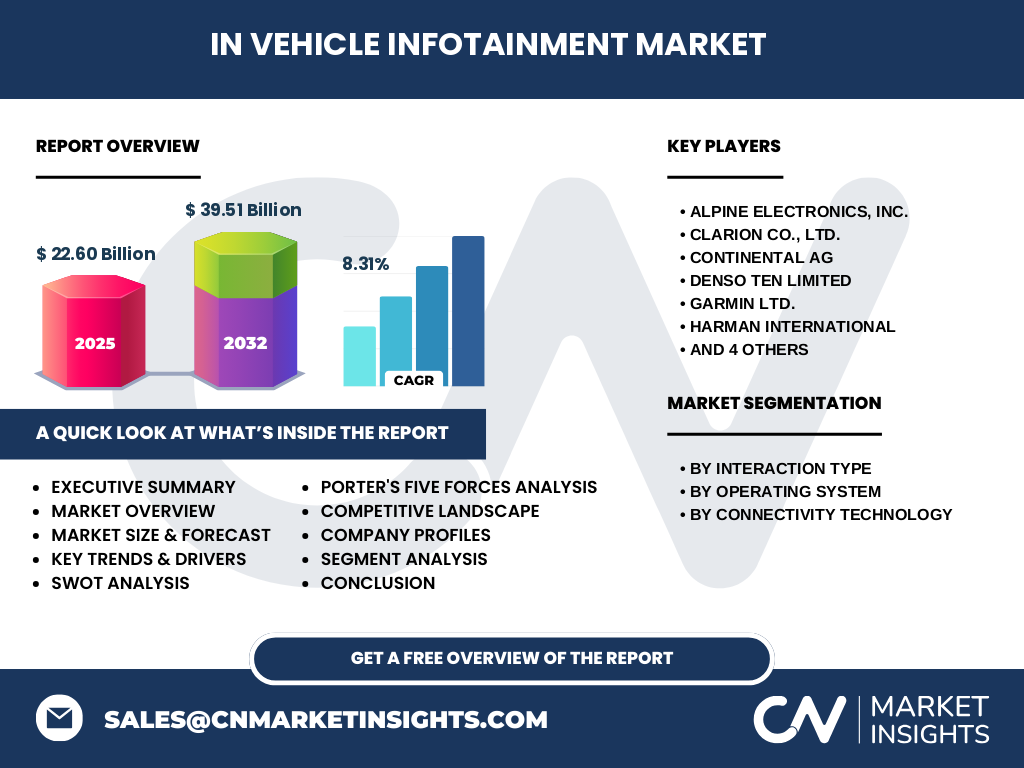

Executive Summary - High-level overview and key findings about In-vehicle Infotainment Market

The global IVI market demonstrates robust growth potential, with market size projected to increase from $22.60 billion in 2025 to $39.51 billion by 2032, representing a compound annual growth rate of 8.31%. Touch-based interaction systems currently dominate the market, while voice-enabled systems show the fastest growth trajectory. The operating system landscape is diverse, with Microsoft, QNX, and Linux platforms competing for market share. Connectivity technologies are evolving, with Wi-Fi, Bluetooth, and NFC integration becoming standard features. The market's growth is driven by technological advancements, increasing consumer expectations, and the automotive industry's shift toward connected and autonomous vehicles. Key challenges include balancing functionality with safety considerations and managing the complexity of integrated systems.

In-vehicle Infotainment Market Forecast - Projections for 2025-2032 period

Based on current market analysis, the IVI market is positioned for substantial growth over the forecast period. The market is expected to maintain a steady compound annual growth rate of 8.31%, reaching $39.51 billion by 2032. This growth will be driven by increasing vehicle production, particularly in emerging markets, and the continued integration of advanced features in both premium and mainstream vehicles. The forecast period will likely see accelerated adoption of voice-enabled systems and gesture controls, while traditional button-based interfaces gradually decline. The expansion of 5G networks and the development of autonomous driving technologies will create new opportunities for market growth and innovation in system capabilities.

In-vehicle Infotainment Market Size and Share by Segmentation - Breakdown by {segmentData}

The IVI market segmentation reveals distinct patterns in consumer preferences and technological adoption. Touch-based systems currently hold the largest market share due to their intuitive interface and widespread acceptance. Voice-enabled systems represent the fastest-growing segment, driven by advancements in natural language processing and increasing focus on driver safety. Physically button-controlled systems and gesture-based interfaces occupy smaller market segments but continue to serve specific use cases and consumer preferences. The operating system segment shows Microsoft maintaining a significant presence in enterprise applications, while QNX dominates in real-time control systems. Linux-based platforms are gaining traction due to their open-source nature and customization capabilities. Connectivity technology adoption varies by region and vehicle segment, with Bluetooth and NFC becoming standard features across most vehicle categories.

Global In-vehicle Infotainment Market Size and Share by Region - Geographic distribution

While specific regional market share data is not provided, the global distribution of the IVI market reflects varying adoption rates and consumer preferences across different geographic regions. North America and Europe typically lead in technology adoption and premium feature integration, driven by higher disposable incomes and strong automotive manufacturing bases. The Asia-Pacific region represents the fastest-growing market, fueled by increasing vehicle production, rising middle-class populations, and growing demand for connected vehicle features. Emerging markets in Latin America and Africa are showing increasing adoption rates as vehicle ownership expands and technology costs decrease. Regional variations in regulatory requirements, infrastructure development, and consumer preferences continue to influence market dynamics and product offerings.

Regional Analysis of the In-vehicle Infotainment Market - Detailed regional market performance

Regional market performance varies significantly based on economic conditions, regulatory frameworks, and consumer preferences. Developed markets in North America and Europe demonstrate mature adoption rates with high penetration of advanced features and premium systems. These regions benefit from strong automotive manufacturing capabilities and established technology infrastructure. The Asia-Pacific region shows the most dynamic growth, driven by expanding automotive production, increasing urbanization, and rising consumer expectations. Countries like China, Japan, and South Korea are leading in technology adoption and local manufacturing capabilities. Emerging markets face challenges related to infrastructure development and cost sensitivity but offer significant growth potential as vehicle ownership increases and technology becomes more accessible.

Leading Company Profiles in the In-vehicle Infotainment Market - Industry players and strategies

Leading companies in the IVI market have developed distinct strategies to capture market share and drive innovation. Alpine Electronics focuses on premium audio and multimedia solutions, leveraging its expertise in high-fidelity sound systems. Clarion emphasizes integrated navigation and entertainment solutions with strong aftermarket presence. Continental AG leverages its automotive industry expertise to provide comprehensive system integration solutions. Denso Ten Limited combines Japanese manufacturing precision with advanced technology development. Garmin brings its navigation expertise to automotive applications, while Harman International focuses on premium audio experiences and connected car solutions. JVC Kenwood combines multimedia expertise with automotive applications, and Panasonic leverages its electronics manufacturing capabilities. Pioneer Corporation maintains a strong presence in both OEM and aftermarket segments, while Visteon Corporation focuses on comprehensive cockpit electronics solutions.

Porter's Five Forces Analysis of the In-vehicle Infotainment Market - Competitive forces assessment

The IVI market exhibits moderate to high competitive intensity across Porter's Five Forces framework. The threat of new entrants is moderate due to high capital requirements and established relationships between manufacturers and suppliers. Bargaining power of buyers is increasing as consumers demand more features and better integration with personal devices. Suppliers of key components such as displays and processors maintain significant bargaining power due to limited alternatives and specialized requirements. The threat of substitutes is relatively low as IVI systems become increasingly integrated into vehicle architecture. Competitive rivalry is intense, with companies competing on technology, user experience, and pricing. The market shows signs of consolidation as larger players acquire smaller companies to expand capabilities and market reach.

SWOT Analysis of the In-vehicle Infotainment Market - Strengths, weaknesses, opportunities, threats

The IVI market demonstrates several key strengths including rapid technological advancement, strong consumer demand, and increasing integration with other vehicle systems. The market benefits from established supply chains and growing expertise in system integration. However, weaknesses exist in the form of high development costs, cybersecurity vulnerabilities, and the complexity of managing multiple system interfaces. Opportunities abound in emerging technologies such as artificial intelligence, augmented reality, and 5G connectivity. The market can expand through new vehicle segments and geographic regions. Threats include regulatory challenges, rapid technological obsolescence, and increasing competition from technology companies entering the automotive space. Economic uncertainties and supply chain disruptions also pose potential risks to market growth.

In-vehicle Infotainment Market Value Chain Analysis - Industry structure and value flow

The IVI value chain encompasses multiple stages from component manufacturing to end-user experience. Raw material suppliers provide essential components such as semiconductors, displays, and connectivity modules. Component manufacturers produce specialized hardware including processors, touchscreens, and audio systems. System integrators combine hardware and software components into cohesive solutions, while software developers create user interfaces and applications. Automotive manufacturers incorporate these systems into vehicles during production, and aftermarket suppliers provide upgrade and replacement options. The value chain is characterized by increasing collaboration between traditional automotive suppliers and technology companies, with growing emphasis on software development and over-the-air update capabilities. Distribution channels include direct OEM supply, aftermarket retailers, and online platforms.

Key Investment Insights in the In-vehicle Infotainment Market - Strategic investment recommendations

Strategic investment opportunities in the IVI market focus on several key areas. Voice-enabled technology and artificial intelligence integration represent significant growth potential, with increasing demand for hands-free operation and personalized experiences. Investment in cybersecurity solutions is critical as systems become more connected and vulnerable to potential threats. The development of cloud-based services and over-the-air update capabilities offers opportunities for recurring revenue streams and enhanced customer engagement. Emerging markets present attractive investment opportunities due to growing vehicle production and increasing consumer demand for advanced features. Companies should consider strategic partnerships and acquisitions to acquire specialized capabilities and expand market presence. Investment in research and development remains crucial to maintain competitive advantage in this rapidly evolving market.

In-vehicle Infotainment Market Conclusion - Summary and key takeaways

The IVI market represents a dynamic and rapidly evolving segment of the automotive industry, characterized by strong growth potential and continuous technological innovation. The market's projected growth from $22.60 billion to $39.51 billion by 2032, at a CAGR of 8.31%, underscores its significance and future potential. Touch-based systems currently dominate, while voice-enabled solutions show the fastest growth trajectory. The market is shaped by increasing consumer demand for connected features, advancements in artificial intelligence and connectivity technologies, and the automotive industry's shift toward autonomous driving. Success in this market requires a balanced approach to innovation, cost management, and user experience optimization, while addressing challenges related to safety, cybersecurity, and system complexity.

Research Methodology - How this research was conducted

This market research was conducted through a comprehensive analysis of multiple data sources and research methodologies. Primary research involved interviews with industry experts, manufacturers, and technology providers to gather insights on market trends, challenges, and opportunities. Secondary research included analysis of industry reports, company financial statements, press releases, and technical publications. Market size and growth projections were derived using both top-down and bottom-up approaches, considering factors such as vehicle production volumes, technology adoption rates, and regional market dynamics. Data triangulation was employed to validate findings across multiple sources, ensuring accuracy and reliability of the research conclusions.

Research Scope - Coverage and limitations

The research scope encompasses the global IVI market, covering major geographic regions, technology segments, and market participants. The analysis includes both OEM and aftermarket segments, with focus on key interaction types, operating systems, and connectivity technologies. Limitations include the availability of detailed regional market data and the rapid pace of technological change that may impact long-term projections. The research focuses on commercially available technologies and established market trends, while emerging technologies and potential disruptions are discussed based on current development trajectories and industry expert opinions.

Key Companies and Recent Developments in the In-vehicle Infotainment Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

Key companies in the IVI market have demonstrated active engagement in product development and strategic partnerships. Alpine Electronics continues to expand its premium audio and multimedia offerings, focusing on integration with emerging vehicle technologies. Clarion has strengthened its position in navigation and entertainment systems through strategic partnerships with content providers. Continental AG has announced advancements in system integration capabilities, combining IVI with advanced driver assistance systems. Denso Ten Limited has focused on developing cost-effective solutions for emerging markets while maintaining quality standards. Garmin has expanded its automotive navigation offerings with enhanced connectivity features. Harman International has launched new connected car platforms emphasizing artificial intelligence integration. JVC Kenwood has introduced multimedia systems with enhanced smartphone integration capabilities. Panasonic continues to develop advanced display technologies for automotive applications. Pioneer Corporation has announced new aftermarket solutions with expanded connectivity options. Visteon Corporation has focused on comprehensive cockpit electronics solutions integrating multiple vehicle systems.