What is the Document Analysis Market Overview – definition, scope, and significance?

The Document Analysis Market encompasses solutions and services that enable organizations to automatically extract, classify, and interpret data from structured and unstructured documents. This includes optical character recognition (OCR), intelligent character recognition (ICR), natural language processing (NLP), and machine‑learning algorithms that transform paper‑based or digital files into actionable information. The scope spans core technologies (software engines, APIs, and platforms), deployment models (cloud and on‑premise), and end‑use verticals such as banking, government, healthcare, retail, and manufacturing. Its significance lies in accelerating digital transformation, reducing manual data‑entry costs, improving compliance, and unlocking hidden insights from legacy documents that are critical for decision‑making and operational efficiency.

What are the key drivers, restraints, challenges, and opportunities shaping the Document Analysis Market?

Growth is driven by escalating volumes of digital content, stricter regulatory requirements, and the need for faster, error‑free data processing. Enterprises are increasingly adopting automation to improve customer experience and cut operational expenses, fueling demand for advanced document‑analysis solutions. Restraints include data‑privacy concerns, especially in highly regulated sectors, and the initial integration complexity of AI‑based tools with legacy systems. Challenges revolve around model accuracy across diverse document types and languages, as well as the shortage of skilled AI talent. Opportunities emerge from the expansion of cloud‑native services, the rise of low‑code/no‑code platforms that democratize adoption, and the potential to combine document analysis with broader intelligent process automation (IPA) suites.

What current and emerging growth trends are influencing the Document Analysis Market?

Current trends include the convergence of document analysis with robotic process automation (RPA) and hyper‑automation strategies, allowing end‑to‑end workflow automation. Cloud adoption is accelerating, offering scalable compute resources and subscription pricing that lower entry barriers. Emerging trends feature the integration of large language models (LLMs) to enhance contextual understanding, and the use of edge AI for on‑device processing where latency or bandwidth is a concern. Additionally, sector‑specific pre‑trained models—such as for healthcare claim forms or financial statements—are gaining traction, delivering higher accuracy out of the box.

How did COVID‑19 impact the Document Analysis Market, and what is the recovery trajectory?

The pandemic forced organizations to shift to remote operations, dramatically increasing reliance on digital document handling and accelerating the adoption of cloud‑based analysis tools. While short‑term disruptions affected on‑premise deployments, the overall effect was a net boost to market momentum. Recovery is characterized by sustained investment in digital workflows, with companies prioritizing resilient, scalable solutions that can support hybrid work environments. This post‑COVID momentum underpins the strong growth outlook for the market.

Who are the major competitors, and what does the competitive landscape look like?

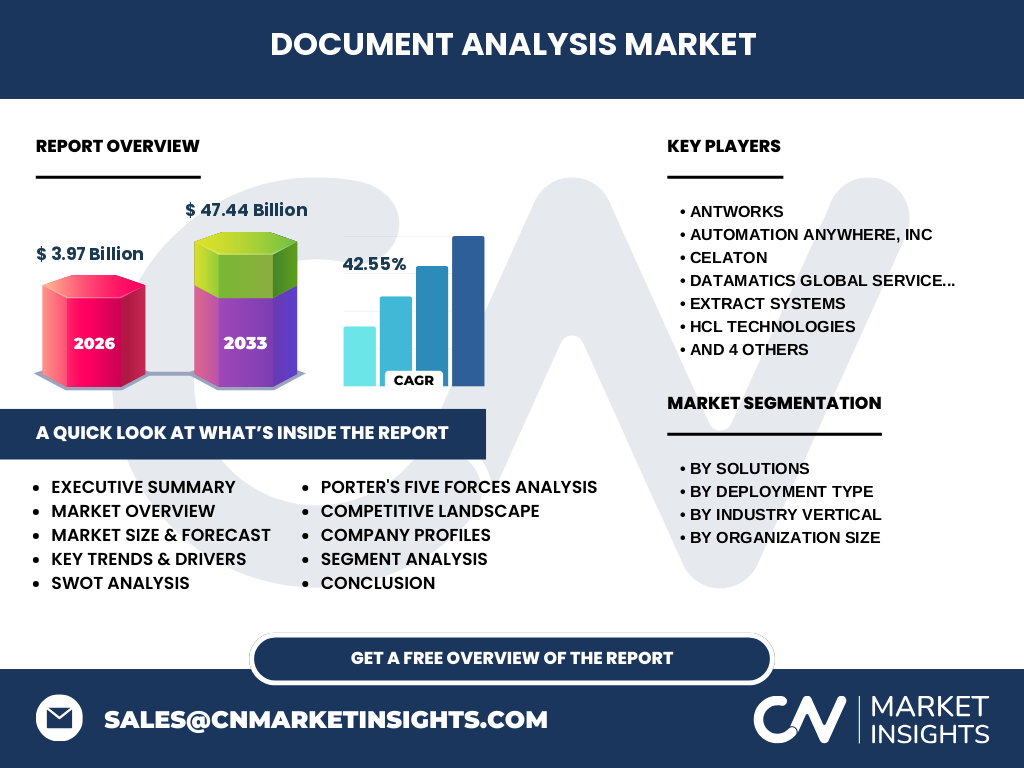

The market is fragmented with a mix of global technology leaders and niche specialists. Key players include AntWorks, Automation Anywhere, Inc., Celaton, Datamatics Global Services Limited, Extract Systems, HCL Technologies, HYPERSCIENCE, Hyland Software, Inc., IBM Corporation, and OpenText Corporation. Companies compete on AI accuracy, integration flexibility, deployment options, and industry‑specific solutions. Recent consolidation activity—such as strategic acquisitions and partnership agreements—has intensified competition, prompting firms to broaden their portfolios through bundled RPA, AI, and content‑management offerings.

What are the high‑level findings presented in the Executive Summary?

The Executive Summary highlights a rapidly expanding Document Analysis Market valued at $3.97 billion in 2026, with a forecast reaching $47.44 billion by 2033, driven by a 42.55 % CAGR. Growth is propelled by digital transformation initiatives, cloud migration, and the merging of document analysis with broader automation ecosystems. Key insights reveal strong demand across BFSI, government, healthcare, retail, and manufacturing, with cloud deployments outpacing on‑premise solutions. Competitive dynamics are shaped by a blend of established IT giants and agile AI specialists, all pursuing product innovation, strategic partnerships, and geographic expansion.

What is the projected market outlook for 2025‑2032?

Forecasts indicate a sustained upward trajectory, with the market expected to multiply more than tenfold between 2025 and 2032. The robust CAGR of 42.55 % reflects accelerating adoption of AI‑driven analysis, expanding use cases in compliance and customer onboarding, and increasing budgets for intelligent automation. By 2032, cloud‑based solutions are projected to dominate, while vertical‑specific offerings will further differentiate vendors and capture higher-margin segments.

How is the market sized and shared across the defined segments?

Segmentation is based on solutions, deployment type, industry vertical, and organization size. Solutions are split between products (software licenses, SaaS platforms) and services (implementation, customization, and support). Deployment options include cloud and on‑premise, with cloud gaining traction due to scalability and lower upfront costs. Industry verticals—BFSI, government, healthcare, retail, and manufacturing—each exhibit unique document‑processing needs, influencing solution design and pricing. Finally, the market distinguishes between large enterprises, which often require extensive integration and compliance features, and small‑ and medium‑sized enterprises (SMEs), which favor out‑of‑the‑box, cost‑effective cloud offerings.

What is the global market size and share by region?

While specific regional dollar figures are not disclosed, the market exhibits a worldwide footprint with strong presence in North America, Europe, APAC, and emerging growth in Latin America and the Middle East. North America leads in early adoption of AI and cloud services, Europe follows with a focus on regulatory compliance, and APAC displays the fastest growth rate due to rapid digitization in manufacturing and banking sectors.

What does the regional analysis reveal about market performance?

North America’s mature enterprise landscape drives high per‑company spend on advanced analytics and security‑focused document solutions. Europe’s stringent data‑privacy laws (e.g., GDPR) stimulate demand for secure, on‑premise, and hybrid deployments. APAC’s large, cost‑sensitive SME base fuels cloud‑centric offerings, while government modernization programs in India and China boost public‑sector adoption. Latin America and the Middle East show emerging opportunities as organizations initiate digital transformation projects.

Which companies lead the market, and what are their strategic initiatives?

Leading firms such as IBM and OpenText leverage extensive content‑management ecosystems to embed document analysis across enterprise workflows. Automation Anywhere expands its RPA suite with AI‑powered document bots. AntWorks focuses on low‑code platforms that accelerate deployment for SMEs. HCL Technologies and Datamatics offer end‑to‑end services, from consulting to managed operations. Recent strategic moves include acquisitions of niche AI startups, partnership with cloud providers, and the launch of industry‑specific solution bundles for healthcare claims and banking KYC processes.

How does Porter’s Five Forces model apply to the Document Analysis Market?

Threat of new entrants is moderate; cloud platforms lower entry barriers, but high AI expertise and data‑security requirements deter many. Bargaining power of buyers is increasing as more vendors offer comparable AI accuracy, prompting procurement teams to negotiate on price and integration flexibility. Bargaining power of suppliers—primarily AI talent and cloud infrastructure—remains high, influencing cost structures. Threat of substitutes is low; manual data entry is inefficient, and generic OCR tools lack the intelligence of modern analysis platforms. Industry rivalry is intense, with competition focused on technology differentiation, vertical specialization, and ecosystem partnerships.

What are the SWOT analysis highlights for the Document Analysis Market?

Strengths: rapid AI advancements, strong demand for automation, and clear ROI through cost reduction. Weaknesses: data‑privacy concerns and integration complexity. Opportunities: expansion into emerging economies, development of LLM‑enhanced contextual analysis, and creation of turnkey vertical solutions. Threats: evolving regulatory landscapes, potential AI model bias, and cybersecurity risks associated with cloud deployments.

What does the value‑chain analysis reveal about the industry structure?

The value chain begins with data acquisition (scanning, ingestion), proceeds to preprocessing (image enhancement, de‑skewing), then core AI processing (OCR, NLP, classification), followed by output integration (API delivery, workflow orchestration). Supporting activities include cloud infrastructure provisioning, model training with domain‑specific datasets, and post‑deployment support. Vendors that excel in end‑to‑end orchestration—combining robust AI engines with seamless integration layers—capture higher margins and customer loyalty.

What key investment insights can be derived for stakeholders?

Investors should prioritize companies with strong AI R&D pipelines, diversified vertical portfolios, and scalable cloud offerings. Strategic acquisitions of niche AI talent or domain‑specific data assets can accelerate market share gains. Partnerships with major cloud providers enhance global reach and simplify compliance for multinational clients. Additionally, focusing on SME‑friendly pricing models and low‑code deployment tools can unlock large, untapped market segments.

What conclusions can be drawn from the Document Analysis Market study?

The market is on a steep growth trajectory, underpinned by the convergence of AI, cloud, and automation. Organizations across all major industries recognize the strategic value of converting unstructured documents into structured, actionable data. While challenges around privacy and integration persist, the opportunities—particularly in emerging regions and vertical‑specific solutions—outweigh the risks. Companies that combine technological excellence with flexible deployment and strong industry expertise are positioned to lead the market.

How was the research methodology designed and executed?

The study employed a mixed‑method approach: primary interviews with senior executives from leading vendors and end‑users, secondary data collection from industry reports, financial filings, and reputable market databases, followed by triangulation to validate findings. Quantitative modeling used the provided base year market size ($3.97 billion) and forecast ($47.44 billion) to calculate the CAGR (42.55 %). Qualitative analysis addressed trends, competitive dynamics, and strategic implications.

What is the scope of the research, and what limitations were acknowledged?

The research covers global Document Analysis solutions across all major deployment models, industry verticals, and organization sizes. It focuses on AI‑driven capabilities and excludes legacy, rule‑based OCR tools not integrated with intelligent automation. Geographic scope includes all key regions, though granular country‑level revenue breakdowns are outside the current scope.

Which key companies and recent developments are shaping the Document Analysis Market?

Notable players include AntWorks (launch of a low‑code AI platform), Automation Anywhere (integration of document bots into its RPA suite), Celaton (partnership with cloud providers for scalable services), Datamatics (acquisition of a niche NLP startup), Extract Systems (release of a healthcare‑focused claim‑processing engine), HCL Technologies (expansion of managed AI services), HYPERSCIENCE (introduction of real‑time edge AI document capture), Hyland Software (enhanced content‑management integration), IBM (upgrade of Watson Discovery for document insight), and OpenText (bundling of AI with its Documentum suite). These initiatives underscore a market moving toward holistic, industry‑specific automation ecosystems.