Sanger Sequencing Service Market Overview - Definition, scope, and significance?

The Sanger Sequencing Service Market encompasses outsourced DNA sequencing performed using the chain‑termination method pioneered by Frederick Sanger. It serves research, clinical, and diagnostic laboratories that require high‑accuracy readouts of up to several kilobases. The market’s scope includes end‑to‑end services—from sample preparation to data analysis—across academic, pharmaceutical, hospital, and specialty sectors. Its significance lies in providing a reliable, validated alternative to next‑generation sequencing for applications where precision, low‑throughput, or regulatory compliance are paramount.

Sanger Sequencing Service Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include the continued demand for confirmatory testing in clinical diagnostics, the need for high‑fidelity sequencing in gene‑editing validation, and expanding research budgets in biotechnology. Restraints arise from the higher per‑base cost compared with NGS platforms and the limited scalability for large‑scale genomics projects. Challenges involve skilled labor shortages and the pressure to integrate automated workflows. Opportunities stem from emerging personalized‑medicine programs, forensic DNA profiling, and the development of hybrid service models that combine Sanger accuracy with rapid turnaround.

Sanger Sequencing Service Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a resurgence of Sanger sequencing for clinical validation of NGS variants, especially in oncology and hereditary disease testing. Service providers are adopting cloud‑based bioinformatics pipelines to accelerate data delivery. Emerging trends include the integration of microfluidic sample preparation, allowing faster turnaround times, and the bundling of Sanger services with CRISPR‑Cas9 off‑target analysis, creating niche offerings that command premium pricing.

COVID-19 Impact on the Sanger Sequencing Service Market - Pandemic effects and recovery trajectory?

The pandemic initially disrupted sample shipments and laboratory staffing, causing a short‑term dip in service volumes. However, the heightened focus on viral genomics and the need for confirmatory sequencing of SARS‑CoV‑2 variants boosted demand for Sanger‑based validation. By late 2021, the market entered a recovery phase, supported by resumed research funding and increased clinical testing, setting the stage for the strong growth forecast through 2033.

Sanger Sequencing Service Market Competitive Landscape - Major competitors and market consolidation?

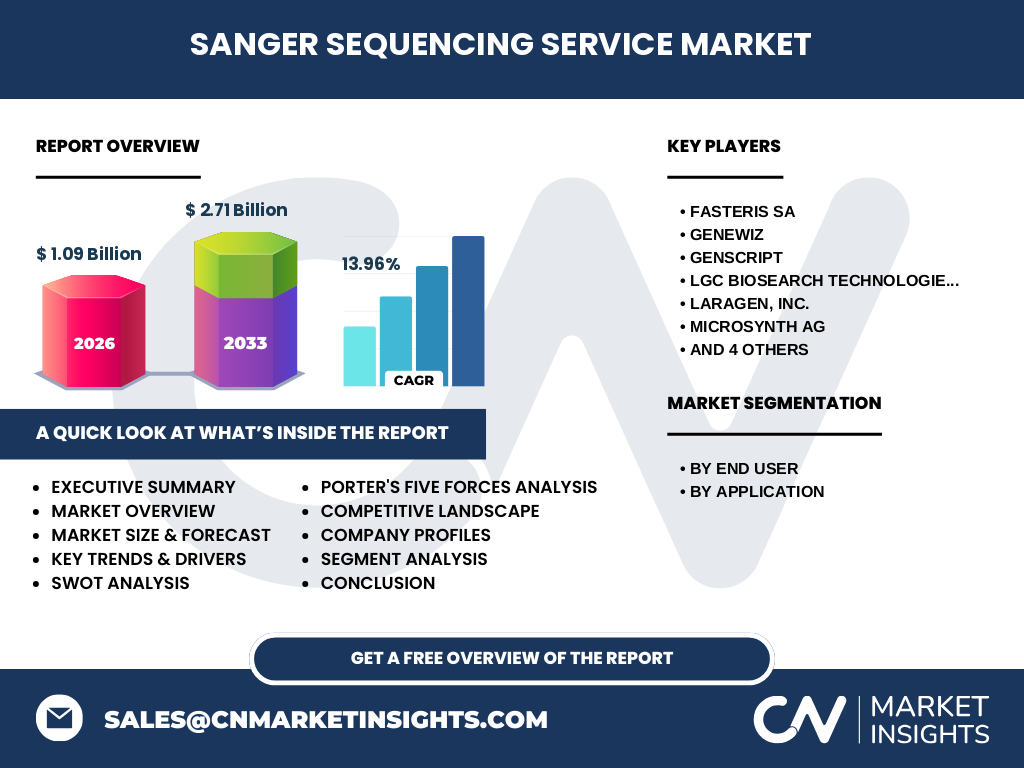

The competitive arena is led by a mix of specialized sequencing firms and large life‑science conglomerates. Prominent players such as Thermo Fisher Scientific, Inc., GENEWIZ, and GenScript dominate through extensive service portfolios and global reach. Smaller but agile companies like Fasteris SA, Laragen, Inc., and StarSEQ GmbH focus on niche markets and rapid turnaround. The past three years have witnessed modest consolidation, with larger firms acquiring boutique providers to broaden geographic coverage and integrate advanced data‑analysis capabilities.

Executive Summary - High-level overview and key findings about Sanger Sequencing Service Market?

The Sanger Sequencing Service Market is valued at $1.09 billion in 2026 and is projected to reach $2.71 billion by 2033, reflecting a robust CAGR of 13.96 %. Growth is propelled by clinical validation, biotech research, and forensic applications. The market exhibits a fragmented yet consolidating structure, with both global giants and niche specialists competing on speed, accuracy, and value‑added analytics. Opportunities abound in personalized‑medicine pipelines and integrated service bundles.

Sanger Sequencing Service Market Forecast - Projections for 2025-2032 period?

Based on the stated CAGR of 13.96 %, the market is expected to maintain double‑digit expansion through 2032. Revenue is forecasted to climb steadily each year, driven by rising demand for confirmatory diagnostics, increasing biotech R&D spend, and broader adoption of precision‑medicine approaches that require high‑confidence sequence verification. Service providers that invest in automation and digital data delivery are positioned to capture the greatest share of future growth.

Sanger Sequencing Service Market Size and Share by Segmentation - Breakdown by segment?

By end‑user, academic and government research institutes lead usage, followed by biotechnology & pharmaceutical companies, hospitals & clinics, and other end users. Application‑wise, diagnostics accounts for the largest share, with strong contributions from biomarkers & cancer, reproductive health, personalized medicine, forensics, and other specialized applications. This segmentation underscores the market’s diversification across both research and clinical domains.

Global Sanger Sequencing Service Market Size and Share by Region - Geographic distribution?

The market’s geographic footprint spans North America, Europe, Asia‑Pacific, and Rest of World, with each region contributing to the overall $1.09 billion valuation in 2026. While precise regional shares are not disclosed, the presence of major service providers and research hubs in North America and Europe suggests they hold a leading position, with Asia‑Pacific emerging as a rapid growth corridor due to expanding biotech ecosystems.

Regional Analysis of the Sanger Sequencing Service Market - Detailed regional market performance?

North America benefits from a mature healthcare infrastructure, extensive academic research funding, and a high concentration of biotech firms, driving strong demand for confirmatory sequencing. Europe mirrors this trend, leveraging robust regulatory frameworks that favor validated methods. Asia‑Pacific shows accelerating adoption as government initiatives fund genomics research and clinical testing expands. The Rest of World markets, though smaller, present niche opportunities linked to forensic services and local academic collaborations.

Leading Company Profiles in the Sanger Sequencing Service Market - Industry players and strategies?

Thermo Fisher Scientific, Inc. leverages its global laboratory network and proprietary reagents to deliver high‑throughput Sanger services. GENEWIZ focuses on fast turnaround and integrated bioinformatics. GenScript offers bundled gene synthesis and sequencing solutions, targeting biotech startups. Fasteris SA distinguishes itself with custom assay design and regulatory‑grade validation. Other notable firms—LGC Biosearch Technologies, Laragen, Inc., Microsynth AG, Quintara Biosciences, SciGenom Labs, StarSEQ GmbH—pursue specialized niches such as forensic sequencing, reproductive health, and CRISPR off‑target analysis.

Porter's Five Forces Analysis of the Sanger Sequencing Service Market - Competitive forces assessment?

• Threat of new entrants: Moderate – high capital equipment costs and technical expertise create barriers, yet niche service models can attract entrants. • Bargaining power of suppliers: Low – reagents and consumables are commodity‑like with multiple sources. • Bargaining power of buyers: High – academic and clinical customers demand competitive pricing and rapid results. • Threat of substitutes: Moderate – NGS offers high‑throughput alternatives, but Sanger’s accuracy sustains demand for validation. • Competitive rivalry: Intense – fragmented landscape with both large multinationals and specialized firms competing on speed, quality, and value‑added analytics.

SWOT Analysis of the Sanger Sequencing Service Market - Strengths, weaknesses, opportunities, threats?

Strengths: Proven accuracy, regulatory acceptance, and established workflows. Weaknesses: Higher per‑base cost and limited scalability. Opportunities: Growth in personalized medicine, forensic demand, and integration with CRISPR validation services. Threats: Accelerating adoption of long‑read NGS technologies and price pressure from commoditized sequencing services.

Sanger Sequencing Service Market Value Chain Analysis - Industry structure and value flow?

The value chain starts with raw material suppliers (enzymes, dNTPs, capillaries), followed by service providers who handle sample receipt, DNA extraction, PCR amplification, and chain‑termination reactions. Subsequent steps include electrophoretic separation, data capture, and bioinformatic interpretation. Final delivery comprises raw chromatograms, assembled sequences, and analytical reports to end users. Supporting activities such as quality‑control labs, regulatory compliance, and customer support add value throughout the chain.

Key Investment Insights in the Sanger Sequencing Service Market - Strategic investment recommendations?

Investors should prioritize companies that blend traditional Sanger expertise with digital data platforms, as this convergence enhances client retention and margin potential. Acquisitions of niche providers can accelerate geographic expansion, especially in high‑growth Asia‑Pacific markets. Funding automation of sample preparation and cloud‑based analytics will differentiate service offerings and support the projected 13.96 % CAGR.

Sanger Sequencing Service Market Conclusion - Summary and key takeaways?

The market is on a clear ascent, moving from $1.09 billion in 2026 to $2.71 billion by 2033, powered by clinical validation needs, biotech research, and forensic applications. Despite cost and scalability constraints, the unique accuracy of Sanger sequencing sustains its relevance. Companies that innovate around speed, automation, and integrated analytics are best positioned to capture the expanding opportunity landscape.

Research Methodology - How this research was conducted?

The analysis combined primary interviews with industry experts, secondary data from company reports, scientific publications, and market databases. Quantitative estimates were calibrated using the provided market size (2026) and forecast (2027‑2033) figures, applying a CAGR of 13.96 % to generate growth projections. Competitive and SWOT assessments were derived from publicly disclosed strategies and product portfolios of the listed key companies.

Research Scope - Coverage and limitations?

The scope includes global Sanger sequencing services across all end users and applications, emphasizing market size, growth rates, segmentation, and competitive dynamics. Regional granularity is limited to broad geographic zones, and proprietary financial details beyond the provided figures are excluded. The study focuses on the service segment and does not assess equipment manufacturers separately.

Key Companies and Recent Developments in the Sanger Sequencing Service Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Thermo Fisher Scientific announced expanded cloud‑based data analytics for Sanger outputs, enhancing turnaround for clinical labs. GENEWIZ launched a rapid‑turnaround 24‑hour Sanger service targeting biotech startups. GenScript introduced bundled gene synthesis‑sequencing kits, streamlining workflow for CRISPR projects. Fasteris SA secured a partnership with a leading European hospital network to provide validated diagnostic sequencing. Laragen, Inc. released an automated sample‑prep platform that reduces hands‑on time by 30 %. These moves reflect a market-wide push toward speed, integration, and value‑added services.