1. North America 5G Chipset Market Overview - Definition, scope, and significance?

The North America 5G chipset market encompasses the design, manufacturing, and supply of semiconductor components that enable fifth‑generation wireless connectivity in a variety of devices and infrastructure. The scope covers chipsets for smartphones, tablets, autonomous‑vehicle modules, industrial IoT gateways, healthcare monitors, retail point‑of‑sale systems, building‑automation controllers, and core network equipment such as base stations and antennas. This market is significant because 5G delivers ultra‑low latency, higher bandwidth, and massive device density, which are essential for emerging applications like real‑time remote surgery, connected‑car ecosystems, smart grids, and immersive AR/VR experiences. In North America, the rapid rollout of carrier‑grade 5G networks and strong consumer adoption of advanced mobile devices amplify demand for high‑performance chipsets, positioning the region as a pivotal growth engine for the global 5G ecosystem.

2. North America 5G Chipset Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Drivers include aggressive network deployments by major carriers, robust consumer demand for 5G‑enabled smartphones, and increased spending on industrial automation that relies on high‑speed wireless links. Government incentives for broadband expansion and the growing need for low‑latency communication in autonomous‑vehicle testing bolster the market. Restraints stem from high R&D costs and supply‑chain constraints for advanced silicon wafers, which can limit short‑term capacity. Challenges involve intense competition among chipset vendors, the need for compliance with evolving spectrum allocations (sub‑6 GHz, 26‑39 GHz, >39 GHz), and security concerns for critical‑infrastructure deployments. Opportunities arise from expanding 5G use cases in healthcare (remote monitoring, tele‑medicine), edge‑computing platforms, and public‑safety surveillance that require rugged, low‑power chipsets capable of operating across multiple frequency bands.

3. North America 5G Chipset Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a shift toward integrated System‑on‑Chip (SoC) solutions that combine RF front‑end, baseband, and AI accelerators on a single die, reducing power consumption and form factor. Multi‑band designs covering sub‑6 GHz and millimeter‑wave (26‑39 GHz and >39 GHz) are becoming standard to support carrier aggregation. Emerging trends include the rise of open‑radio access network (O‑RAN) architectures, which demand flexible, programmable chipsets, and the convergence of 5G with Wi‑Fi 6/6E in consumer electronics. Additionally, the adoption of silicon‑photonic interconnects in network‑infrastructure equipment is gaining traction, promising higher data‑throughput while maintaining low latency.

4. COVID-19 Impact on the North America 5G Chipset Market - Pandemic effects and recovery trajectory?

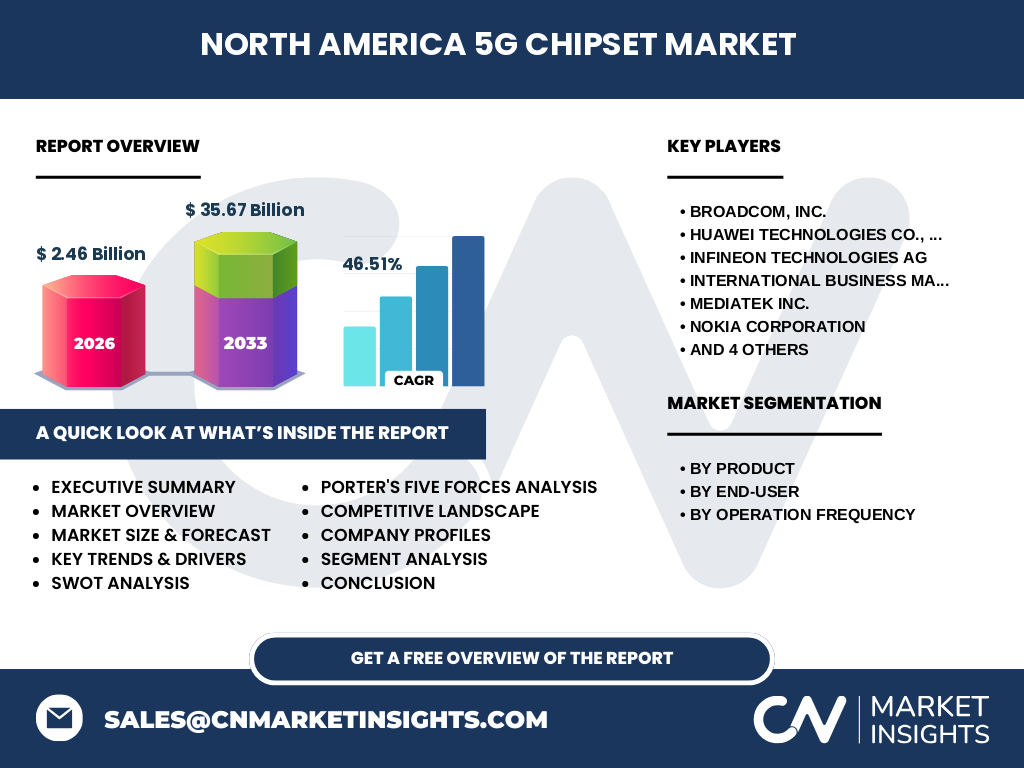

The pandemic initially slowed supply‑chain logistics, causing temporary shortages of semiconductor raw materials and delaying certain network‑equipment rollouts. However, the surge in remote work, tele‑health, and digital entertainment accelerated demand for 5G‑enabled devices, partially offsetting the slowdown. By late 2021, most manufacturers rebounded, and 5G rollout timelines were advanced to meet heightened consumer expectations. The market’s recovery trajectory has been strong, reflected in the projected CAGR of 46.51% and the leap from a 2026 market size of $2.46 billion to a forecasted $35.67 billion for 2027‑2033, indicating robust post‑COVID growth.

5. North America 5G Chipset Market Competitive Landscape - Major competitors and market consolidation?

The competitive arena is dominated by a blend of established semiconductor giants and agile fabless innovators. Key players include Broadcom, Qualcomm, MediaTek, Samsung, Intel (through IBM’s collaboration), and Xilinx, alongside telecom‑focused firms such as Nokia, Ericsson, and Huawei. Recent consolidation activity features strategic acquisitions aimed at expanding AI‑accelerator portfolios and securing mmWave expertise, while joint‑development agreements between chipset vendors and network operators are increasing to accelerate time‑to‑market for carrier‑grade solutions.

6. Executive Summary - High-level overview and key findings about North America 5G Chipset Market?

The North America 5G chipset market is poised for exponential growth, driven by aggressive carrier deployments, strong consumer demand, and expanding industrial use cases. With a 2026 valuation of $2.46 billion and a projected CAGR of 46.51% through 2033, the market is expected to reach $35.67 billion. Multi‑band, AI‑enabled SoCs dominate the product landscape, while key end‑users include automotive, healthcare, and industrial automation. Competitive pressures are intense, but opportunities abound in O‑RAN, edge computing, and public‑safety applications. Investment in advanced R&D and strategic partnerships will be critical for firms seeking market leadership.

7. North America 5G Chipset Market Forecast - Projections for 2025-2032 period?

Based on the disclosed CAGR of 46.51%, the market is projected to expand rapidly from the 2026 baseline of $2.46 billion to an estimated $35.67 billion by the 2027‑2033 horizon. This trajectory implies sustained double‑digit growth throughout 2025‑2032, fueled by continued carrier spectrum releases, widespread adoption of 5G‑enabled IoT devices, and the emergence of new verticals such as smart‑city infrastructure and autonomous logistics. The forecast underscores a shift from early‑stage device adoption to mature, enterprise‑wide deployments across multiple frequency bands.

8. North America 5G Chipset Market Size and Share by Segmentation - Breakdown by segment?

By Product: Devices (smartphones, tablets, wearables) command the largest share, owing to consumer demand for high‑speed mobile broadband. Customer Premises Equipment (CPE) such as 5G routers and gateways follows, supporting home and small‑business connectivity. Network‑Infrastructure Equipment—base stations, small cells, and core‑network processors—captures a growing portion as carriers densify coverage.

By End‑User: Consumer Electronics leads the market, driven by rapid smartphone refresh cycles. Automotive & Transportation is the fastest‑growing vertical, with automakers integrating 5G for vehicle‑to‑everything (V2X) communication. Healthcare, Retail, Building Automation, Industrial Automation, Energy & Utilities, and Public Safety & Surveillance each exhibit steady demand as sector‑specific 5G solutions mature.

By Operation Frequency: Sub‑6 GHz chipsets retain the broadest deployment due to favorable propagation characteristics. The 26‑39 GHz millimeter‑wave segment is expanding rapidly for high‑capacity urban hotspots and fixed‑wireless access. Above 39 GHz remains niche, primarily serving ultra‑high‑throughput backhaul and specialty radar applications.

9. Global North America 5G Chipset Market Size and Share by Region - Geographic distribution?

Within the global 5G chipset ecosystem, North America accounts for a substantial share thanks to early carrier rollouts, high disposable income, and a mature technology ecosystem. While precise regional percentages are not disclosed, the region’s $2.46 billion 2026 valuation positions it as a leading market alongside Europe and Asia‑Pacific, with growth driven by both consumer and enterprise adoption.

10. Regional Analysis of the North America 5G Chipset Market - Detailed regional market performance?

In the United States, the market is propelled by the three major carriers’ nationwide 5G expansions, extensive 5G‑enabled device launches, and robust venture‑capital funding for chipset startups. Canada’s market growth is fueled by governmental broadband programs and increasing demand for low‑latency connectivity in the mining and energy sectors. The overall regional performance reflects strong alignment between carrier spectrum auctions, device ecosystem readiness, and industry‑specific pilots that together create a fertile environment for chipset sales.

11. Leading Company Profiles in the North America 5G Chipset Market - Industry players and strategies?

Broadcom, Inc. focuses on high‑performance RF front‑end modules and integrated baseband solutions for network equipment. Qualcomm Incorporated leads with Snapdragon 5G SoCs that combine AI, graphics, and multi‑band RF, targeting smartphones and edge devices. MediaTek Inc. leverages cost‑effective SoCs for mid‑range consumer electronics, expanding into automotive telematics. Samsung Electronics supplies advanced mmWave transceivers and memory‑centric chipsets for both consumer and infrastructure segments. Nokia Corporation and Telefonaktiebolaget LM Ericsson develop chipset platforms optimized for O‑RAN and carrier‑grade base stations. Huawei Technologies continues to innovate in integrated 5G solutions despite regulatory constraints. Infineon Technologies and Xilinx, Inc. concentrate on power‑efficient RF front‑ends and programmable logic for industrial and automotive applications. International Business Machines Corporation collaborates on AI‑enabled edge compute modules that embed 5G connectivity.

12. Porter's Five Forces Analysis of the North America 5G Chipset Market - Competitive forces assessment?

Threat of New Entrants: Moderate to high. While high capital intensity and IP barriers deter newcomers, fabless startups backed by venture funding can enter niche segments (e.g., low‑power IoT). Bargaining Power of Suppliers: High, due to limited sources for advanced silicon wafers and specialized RF components. Bargaining Power of Buyers: Growing, as OEMs and carriers consolidate purchases and demand multi‑band, cost‑effective solutions. Threat of Substitutes: Low, because alternative wireless technologies (e.g., Wi‑Fi 6) cannot fully replace 5G’s latency and coverage capabilities for many verticals. Industry Rivalry: Intense, with multiple global players competing on performance, power efficiency, and integration levels, driving rapid innovation cycles.

13. SWOT Analysis of the North America 5G Chipset Market - Strengths, weaknesses, opportunities, threats?

Strengths: Strong R&D ecosystem, access to leading fabs, and high adoption rates for 5G devices. Weaknesses: Dependence on a limited number of advanced foundries, which can create supply bottlenecks. Opportunities: Expansion into edge‑computing platforms, O‑RAN solutions, and vertical‑specific chipsets for automotive, healthcare, and public safety. Threats: Geopolitical tensions affecting supply chains (e.g., restrictions on Huawei), rapid technology obsolescence, and escalating competition from Asian manufacturers.

14. North America 5G Chipset Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with design and IP licensing (IP cores, RF libraries) performed by fabless companies, followed by foundry manufacturing (TSMC, GlobalFoundries) that fabricate the silicon wafers. Next is assembly, test, and packaging (ASE, Amkor) delivering ready‑to‑integrate dies. System integration occurs as OEMs embed chipsets into devices or network gear, complemented by software and firmware development for protocol stacks and AI inference. Finally, distribution channels deliver the finished products to carriers, device manufacturers, and enterprise integrators, with after‑sales support and firmware updates sustaining the ecosystem.

15. Key Investment Insights in the North America 5G Chipset Market - Strategic investment recommendations?

Investors should prioritize companies with diversified product portfolios spanning sub‑6 GHz and mmWave bands, and those that have secured long‑term supply agreements with leading foundries. Firms advancing O‑RAN compatible chipsets and programmable silicon (e.g., FPGA‑based solutions) offer attractive upside as carriers shift toward open architectures. Additionally, targeting players that have established strong automotive and industrial partnerships can capture high‑margin, growth‑driven revenue streams. Monitoring regulatory developments and supply‑chain resiliency will be essential for risk mitigation.

16. North America 5G Chipset Market Conclusion - Summary and key takeaways?

The North America 5G chipset market is on a steep growth trajectory, underpinned by a 46.51% CAGR and a projected market size of $35.67 billion for the 2027‑2033 period. Multi‑band, AI‑enabled SoCs dominate product development, while end‑users across automotive, healthcare, and industrial automation drive diversified demand. Competitive intensity, supply‑chain constraints, and geopolitical factors present challenges, yet opportunities in O‑RAN, edge computing, and vertical‑specific solutions create a compelling landscape for investors and innovators alike.

17. Research Methodology - How this research was conducted?

The study employed a mixed‑method approach combining primary interviews with industry executives, carrier planners, and component manufacturers, alongside secondary data extraction from financial reports, regulatory filings, and reputable market databases. Quantitative forecasts were derived using time‑series modeling anchored to the provided 2026 market size ($2.46 billion) and CAGR (46.51%). Qualitative analysis incorporated Porter’s Five Forces, SWOT, and value‑chain mapping to contextualize competitive dynamics.

18. Research Scope - Coverage and limitations?

The scope covers the entirety of North America, focusing on chipset segments for devices, CPE, and network infrastructure, and on end‑users listed in the segmentation table. Frequency bands examined include sub‑6 GHz, 26‑39 GHz, and >39 GHz. While the research leverages the most recent market data, it does not extend to post‑2033 forecasts or to regions outside North America. Proprietary data from individual companies that are not publicly disclosed were not incorporated.

19. Key Companies and Recent Developments in the North America 5G Chipset Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Qualcomm unveiled its Snapdragon X70 5G modem, supporting up to 10 Gbps peak download and integrated AI processing. Broadcom announced a new RF front‑end module optimized for sub‑6 GHz carrier aggregation, targeting enterprise routers. MediaTek launched a mid‑range 5G SoC featuring on‑chip NPU for AI‑enhanced camera functions. Samsung introduced a mmWave transceiver with 30% higher efficiency for small‑cell deployments. Nokia and Ericsson each secured multi‑year contracts with major U.S. carriers to supply O‑RAN‑compatible baseband chipsets. Huawei continued R&D on integrated 5G modules for private‑network solutions despite regulatory constraints. Infineon released a power‑optimized automotive 5G chipset for V2X communication, and Xilinx announced a new programmable SoC aimed at industrial automation that incorporates native 5G connectivity. IBM partnered with Qualcomm to embed quantum‑inspired algorithms within edge AI chipsets, positioning the combined offering for real‑time analytics in healthcare and manufacturing.