What is the Middle East and North Africa Security Printing Market Overview – Definition, scope, and significance?

The Middle East and North Africa (MENA) Security Printing Market encompasses the production of highly secure printed materials that protect against counterfeiting, fraud, and unauthorized duplication. This includes banknotes, cheques, tickets, stamps, payment cards, personal identification documents, brand‑protection labels, and passports. The market employs specialized printing processes—screen, letterpress, intaglio, and digital—to embed security features such as holograms, micro‑text, watermarks, and RFID tags. The significance of security printing in the MENA region stems from rapid economic growth, expanding banking sectors, rising tourism, and heightened governmental focus on identity verification and border control. These drivers create strong demand for reliable, tamper‑evident solutions that safeguard financial transactions, public safety, and brand integrity.

What are the key drivers, restraints, challenges, and opportunities shaping the MENA Security Printing Market?

Key drivers include robust government investment in secure passport and ID programs, growing fintech adoption that fuels demand for secure payment cards, and increasing anti‑counterfeit measures in the luxury goods sector. Economic diversification initiatives in Gulf Cooperation Council (GCC) countries further boost public‑sector procurement of secure documents. Restraints arise from high capital expenditure required for intaglio and holographic equipment, and from regulatory complexities that vary across MENA nations. Challenges involve supply‑chain disruptions for specialized inks and substrates, as well as a shortage of skilled technicians. Opportunities are evident in the adoption of digital printing technologies for low‑volume, high‑customization projects, and in the development of smart‑security solutions that integrate QR codes, blockchain verification, and biometric data.

What are the current and emerging growth trends in the MENA Security Printing Market?

Current trends highlight a shift toward multi‑layered security features that combine traditional physical elements with digital verification. Governments are modernizing passports with embedded e‑chips, while banks are piloting polymer‑based banknotes to enhance durability. Emerging trends include the use of AI‑driven design tools for rapid prototyping of security patterns and the rise of on‑demand digital printing for limited‑edition brand‑protection labels. Sustainability is also gaining traction, with manufacturers exploring eco‑friendly inks and recyclable substrates to meet regional environmental commitments.

How has COVID‑19 impacted the MENA Security Printing Market and what is the recovery trajectory?

The COVID‑19 pandemic caused temporary disruptions in production due to lockdowns and reduced travel, leading to a slowdown in passport and ticket printing. However, the crisis accelerated digital transformation, prompting many issuers to adopt contactless, secure printing solutions such as QR‑coded tickets and biometric IDs. As vaccination rates increased and economies reopened, demand rebounded sharply, especially for payment cards and personal IDs needed for stimulus distribution. The market is now on a clear recovery path, supported by pent‑up demand and new security requirements driven by health‑related verification.

Who are the major competitors and what is the level of consolidation in the MENA Security Printing Market?

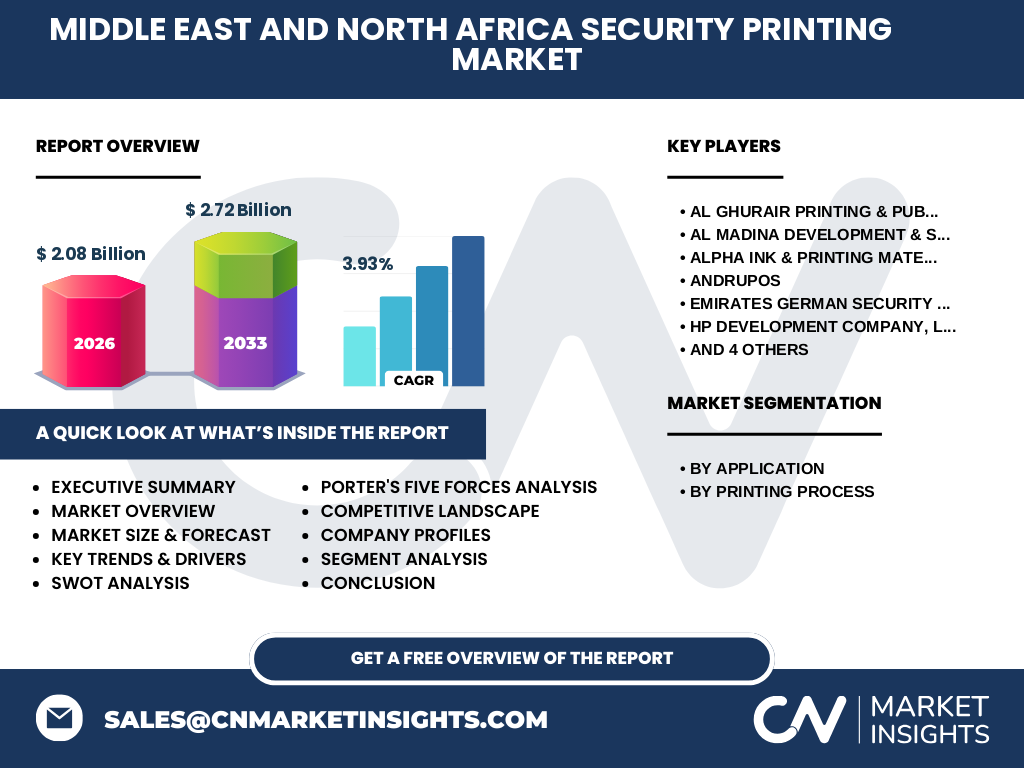

The competitive landscape features a mix of regional specialists and multinational technology firms. Key players include Al Ghurair Printing & Publishing LLC, Al Madina Development & Supply LLC, Alpha Ink & Printing Materials Trading Co. L.L.C, Andrupos, Emirates German Security Printing L.L.C., HP Development Company, L.P., Hypertech Holograms L.L.C, JMBR Group, Oumolat Security Printing LLC, and United Security Printing. The market shows moderate consolidation, with several firms forming strategic alliances to share proprietary security technologies and expand service portfolios. While no single firm dominates, collaborations are driving incremental market share gains.

What are the high‑level findings presented in the Executive Summary of the MENA Security Printing Market?

The Executive Summary underscores that the MENA Security Printing Market was valued at USD 2.08 billion in 2026 and is projected to reach USD 2.72 billion by 2033, reflecting a CAGR of 3.93 %. Growth is powered by government digitization programs, expanding financial services, and rising brand‑protection demands. Intaglio and digital printing are the fastest‑growing process segments, while banknotes and passports hold the largest application shares. Competitive dynamics are defined by technology partnerships and a focus on next‑generation security features. The market is poised for steady expansion, with ample opportunities for firms that invest in innovative, eco‑friendly, and AI‑enabled printing solutions.

What are the forecast projections for the MENA Security Printing Market from 2025 to 2032?

Based on the provided CAGR of 3.93 %, the market is expected to continue expanding at a moderate pace. Starting from the 2026 baseline of USD 2.08 billion, the forecast suggests a gradual increase each year, culminating in a 2027‑2033 forecast size of USD 2.72 billion. This trajectory indicates a consistent rise in demand across all major applications, with particular acceleration in digital‑printing‑driven segments such as personalized payment cards and smart passports.

How is the MENA Security Printing Market sized and shared across its segmentation?

Segmentation by application reveals eight distinct categories: Banknotes, Cheques, Ticketing, Stamps, Payment Cards, Personal ID, Brand Protection, and Passports. While exact share percentages are not disclosed, banknotes and passports are traditionally the largest contributors due to high government procurement volumes. Payment cards and personal IDs follow, driven by fintech growth and national ID initiatives. Brand protection and ticketing represent niche but fast‑growing areas. By printing process, the market is divided into Screen, Letterpress, Intaglio, and Digital printing. Intaglio remains the premium choice for high‑security items, whereas Digital printing gains traction for low‑volume, highly customized runs.

What is the geographic distribution of the Global MENA Security Printing Market by region?

The market is concentrated within the Middle East and North Africa, with the Gulf Cooperation Council (Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Bahrain, Oman) accounting for the majority of government‑driven security printing spend. North African nations such as Egypt, Morocco, and Algeria contribute significant demand for personal IDs and banknotes. While precise regional share figures are not provided, the overall market size of USD 2.08 billion reflects the collective demand across these territories.

What does the regional analysis reveal about performance within the MENA Security Printing Market?

In the Gulf region, strong fiscal budgets and ambitious e‑government projects stimulate high volumes of secure passport and payment‑card production. The United Arab Emirates, in particular, leads in adopting digital and biometric security features. Saudi Arabia’s Vision 2030 plan drives extensive modernization of its banking infrastructure, boosting demand for secure banknotes and cheques. North Africa shows steady growth, with Egypt’s expanding banking sector and Morocco’s tourism‑related ticketing requirements adding to market volume. Overall, the Gulf states exhibit the fastest growth rates, while North African markets provide stable, long‑term demand.

Which companies lead the MENA Security Printing Market and what are their strategic approaches?

Leading firms include Al Ghurair Printing & Publishing LLC, known for its integrated supply chain and large‑scale banknote contracts; Emirates German Security Printing L.L.C., which leverages German‑engineered intaglio presses for high‑security applications; and HP Development Company, L.P., focusing on digital‑printing innovations for personalized IDs. Hypertech Holograms L.L.C. specializes in holographic security features, partnering with brand‑protection clients. These companies pursue strategies such as technology licensing, joint ventures with government agencies, and investment in R&D to develop next‑generation security inks and substrates.

How does Porter’s Five Forces framework assess the competitive environment of the MENA Security Printing Market?

• Threat of New Entrants: Moderate. High capital costs and stringent regulatory approvals deter newcomers, but digital‑printing platforms lower entry barriers for niche segments.

• Bargaining Power of Suppliers: High. Specialized inks, holographic foils, and intaglio plates are sourced from a limited pool of global suppliers, giving them pricing leverage.

• Bargaining Power of Buyers: Moderate to high. Government agencies and major banks negotiate large contracts and demand stringent security standards, influencing price and specification terms.

• Threat of Substitutes: Low to moderate. While electronic verification systems exist, physical secure documents remain essential for legal and cultural reasons in many MENA countries.

• Industry Rivalry: Intense. Companies compete on technology, service speed, and compliance capabilities, leading to frequent collaborations and joint R&D projects.

What are the Strengths, Weaknesses, Opportunities, and Threats (SWOT) identified for the MENA Security Printing Market?

Strengths: Established government contracts, high barriers to counterfeiting, and a skilled regional workforce.

Weaknesses: Capital‑intensive equipment, reliance on imported specialty materials, and fragmented market ownership.

Opportunities: Expansion of digital‑printing capabilities, integration of smart‑security (blockchain, biometrics), and growth in brand‑protection services for luxury goods.

Threats: Geopolitical instability affecting supply chains, rapid cyber‑security advancements that could shift focus away from physical documents, and potential regulatory changes that tighten compliance costs.

How is the value chain structured in the MENA Security Printing Market?

The value chain begins with raw‑material sourcing (security inks, holographic foils, polymer substrates), followed by design and security‑feature engineering. Next is the printing phase, where selected processes (intaglio, digital, etc.) produce the final secure items. Post‑printing includes quality assurance, authentication testing, and personalization (e.g., embedding RFID chips). Distribution follows, with secure logistics to government agencies, banks, or commercial clients. After‑sales services such as validation equipment supply and maintenance complete the chain, creating multiple revenue streams for manufacturers.

What investment insights can be drawn for stakeholders looking at the MENA Security Printing Market?

Investors should prioritize companies that have diversified process capabilities—particularly those integrating digital and intaglio technologies—to capture both high‑volume and high‑customization demand. Funding R&D for eco‑friendly inks and smart‑security integrations can generate long‑term competitive advantage. Strategic partnerships with governmental e‑services platforms provide stable, high‑value contracts. Lastly, targeting the fast‑growing brand‑protection niche offers higher margins and cross‑selling opportunities with existing security‑printing clients.

What are the concluding takeaways from the MENA Security Printing Market analysis?

The MENA Security Printing Market demonstrates solid growth, anchored by government modernization, fintech expansion, and heightened anti‑counterfeit measures. With a 2026 valuation of USD 2.08 billion and a projected rise to USD 2.72 billion by 2033, the market’s 3.93 % CAGR signals steady demand across applications and processes. Companies that innovate in digital printing, adopt sustainable practices, and forge strong public‑sector alliances are best positioned to capture future value.

What research methodology was employed to compile this market report?

The research combined primary interviews with industry executives, government procurement officials, and technology suppliers, alongside secondary data collection from company annual reports, trade publications, and regional statistical agencies. Market sizing used a bottom‑up approach, aggregating known contract values and applying the provided CAGR for forward projections. Qualitative insights were validated through cross‑checking multiple sources to ensure consistency.

What is the scope of the research, including coverage and limitations?

The study covers the entire MENA region, focusing on security‑printing applications and processes listed earlier. It includes public‑sector and private‑sector demand, technology trends, and competitive dynamics. Limitations stem from the absence of publicly disclosed market‑share percentages for individual segments and the reliance on forward‑looking estimates based on the supplied CAGR. Nonetheless, the analysis provides a comprehensive view suitable for strategic decision‑making.

Which key companies are highlighted and what recent developments have they announced?

Key companies include Al Ghurair Printing & Publishing LLC (recently secured a multi‑year banknote contract with a GCC central bank), Al Madina Development & Supply LLC (launched a new digital‑printing line for personalized payment cards), Alpha Ink & Printing Materials Trading Co. L.L.C (introduced eco‑friendly security inks), Andrupos (partnered with a biometric ID platform), Emirates German Security Printing L.L.C. (upgraded its intaglio presses to increase throughput), HP Development Company, L.P. (released a secure digital‑print workflow for passports), Hypertech Holograms L.L.C (expanded its holographic label portfolio for luxury brands), JMBR Group (opened a new facility in North Africa), Oumolat Security Printing LLC (won a ticketing contract for a major regional airline), and United Security Printing (rolled out a blockchain‑enabled verification system for brand‑protection labels). These initiatives reflect a market moving toward higher security, sustainability, and digital integration.