What is the UAE Ice Cream Market Overview – Definition, scope, and significance?

The UAE Ice Cream Market comprises the production, distribution, and consumption of frozen dessert products within the United Arab Emirates. It covers all categories of ice cream, including impulse, take‑home, and artisanal varieties, and spans distribution channels such as supermarkets and hypermarkets, convenience stores, and specialty stores. The market is significant because it reflects changing consumer lifestyles, growth in disposable income, and a strong demand for premium and innovative frozen treats, making it a key segment of the broader food‑and‑beverage industry in the UAE.

What are the UAE Ice Cream Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising per‑capita income, a youthful population that favors indulgent products, and increasing tourism which boosts demand in hospitality venues. The expanding health‑conscious segment creates opportunities for low‑fat, dairy‑free, and functional ice creams. Restraints stem from high summer temperatures that can affect storage logistics and from stringent halal certification requirements. Major challenges involve supply‑chain volatility for dairy inputs and intense price competition. Opportunities arise from product innovation, such as plant‑based and exotic flavors, and from leveraging e‑commerce channels to reach tech‑savvy consumers.

What are the UAE Ice Cream Market Growth Trends?

Current trends include a surge in artisanal and craft ice cream offerings, reflecting consumer desire for premium experiences. There is a noticeable shift toward smaller, single‑serve impulse packs for on‑the‑go consumption. Brands are experimenting with ethnic and fusion flavors that resonate with the multicultural population. Additionally, sustainability is influencing packaging choices, with a move toward recyclable or biodegradable materials.

How did COVID-19 impact the UAE Ice Cream Market and what is the recovery trajectory?

The pandemic initially disrupted supply chains and reduced footfall in retail locations, leading to a temporary dip in sales. However, heightened home‑consumption and a rebound in tourism helped the market recover quickly. Post‑COVID, there has been a stronger emphasis on hygiene and contactless delivery, accelerating growth in online ordering and home delivery services for ice cream.

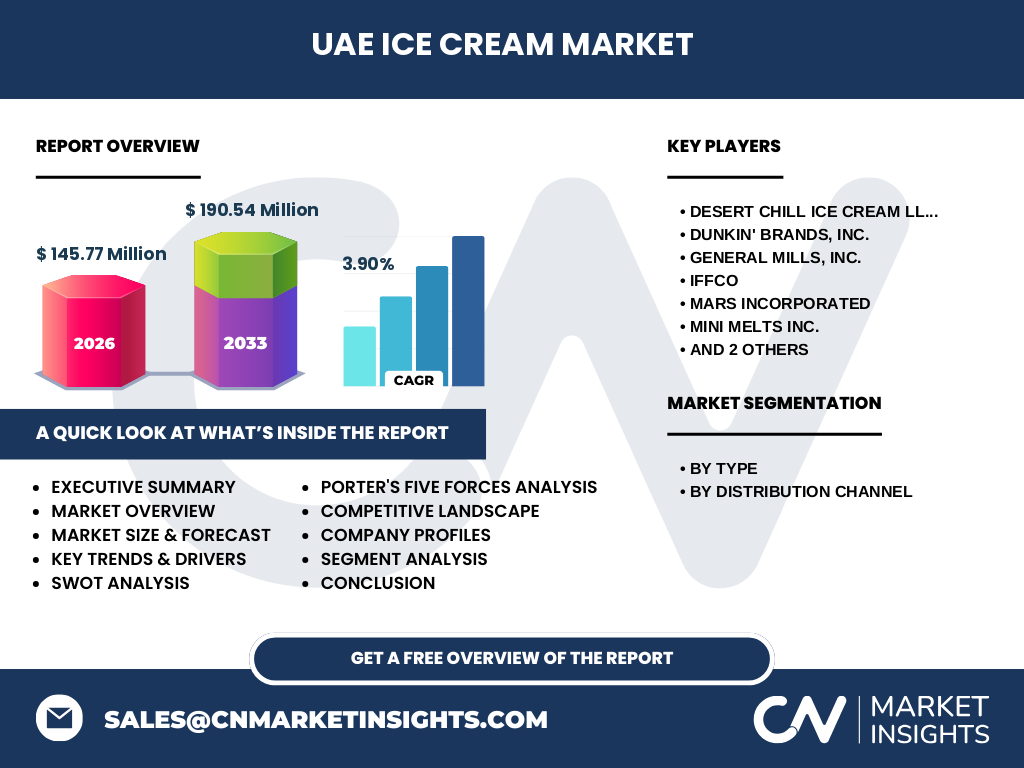

Who are the major competitors in the UAE Ice Cream Market and what is the state of market consolidation?

The competitive landscape features multinational giants such as General Mills, Inc., Nestlé, MARS Incorporated, and Dunkin' Brands, Inc., alongside strong local players like Desert Chill Ice Cream LLC and IFFCO. While the market remains fragmented, there is a gradual consolidation trend as larger firms acquire niche artisanal brands to broaden their portfolio and enhance distribution reach.

What are the key findings in the Executive Summary of the UAE Ice Cream Market?

The market was valued at 145.77 million USD in 2026 and is projected to reach 190.54 million USD by 2033, delivering a CAGR of 3.90 % over the forecast period. Growth is propelled by premiumization, tourism resurgence, and innovative product launches. The distribution channel mix is dominated by supermarkets and hypermarkets, but convenience stores and specialty outlets are gaining share. Local and international players are intensifying competition through new flavors, health‑focused lines, and digital sales strategies.

What is the forecast for the UAE Ice Cream Market for 2025‑2032?

Based on the disclosed CAGR of 3.90 %, the market is expected to maintain steady expansion through 2025‑2032, moving from the 2026 baseline of 145.77 million USD toward the 2033 forecast of 190.54 million USD. This trajectory signals robust demand across all ice‑cream types and reinforces the sector’s attractiveness for investment and new product development.

How is the UAE Ice Cream Market sized and shared by segmentation?

By type, the market is divided into impulse ice cream, take‑home ice cream, and artisanal ice cream. Impulse packs dominate the on‑the‑go segment, take‑home products capture family‑size consumption, and artisanal offerings appeal to premium consumers. By distribution channel, supermarkets and hypermarkets hold the largest share due to extensive shelf space, while convenience stores serve quick‑purchase needs and specialty stores cater to niche, high‑margin products.

What is the global UAE Ice Cream Market size and share by region?

The UAE constitutes a key regional hub within the Middle East for ice‑cream consumption, benefiting from high expatriate density and tourism inflows. While specific regional share figures are not disclosed, the UAE’s market size of 145.77 million USD (2026) positions it as a leading contributor to the broader Middle‑East ice‑cream landscape.

What does the regional analysis of the UAE Ice Cream Market reveal?

Within the UAE, major emirates such as Dubai and Abu Dhabi drive the majority of sales, supported by affluent consumer bases and dense retail networks. Smaller emirates contribute growth through rising tourism and expanding retail formats. The analysis shows that premium and artisanal segments are particularly strong in cosmopolitan areas, whereas impulse products perform well in high‑traffic convenience locations.

What are the leading company profiles in the UAE Ice Cream Market?

Desert Chill Ice Cream LLC is a home‑grown brand known for locally‑tailored flavors and halal compliance. Dunkin' Brands, Inc. leverages its coffee‑shop footprint to cross‑sell frozen treats. General Mills, Inc. and MARS Incorporated bring global brand recognition and extensive distribution. IFFCO focuses on dairy‑based innovation, while MINI Melts Inc. targets the impulse segment with bite‑size packs. Nestlé offers a broad portfolio ranging from classic to premium lines, reinforcing its market presence.

How does Porter’s Five Forces assess the UAE Ice Cream Market?

Threat of new entrants is moderate due to high brand loyalty and the need for halal certification. Bargaining power of suppliers is moderate, as dairy inputs are essential but can be sourced locally or imported. Bargaining power of buyers is high, given abundant choices and price sensitivity. Threat of substitutes is low to moderate, with alternatives like frozen yogurt and gelato gaining niche appeal. Industry rivalry is intense, driven by numerous global and local players competing on price, flavor innovation, and distribution.

What is the SWOT Analysis of the UAE Ice Cream Market?

Strengths: Strong consumer purchasing power, diversified product range, and robust tourism support. Weaknesses: Dependence on temperature‑sensitive logistics and high competition compressing margins. Opportunities: Expansion of health‑focused and plant‑based lines, digital sales channels, and premium artisanal offerings. Threats: Supply‑chain disruptions for dairy, regulatory changes, and potential economic slowdown affecting discretionary spending.

What does the UAE Ice Cream Market value chain look like?

The value chain starts with raw‑material procurement (milk, cream, sugar, stabilizers), followed by formulation and processing in manufacturing facilities. Next is packaging— increasingly focused on sustainability— and distribution through wholesalers to retail outlets across supermarkets, convenience stores, and specialty shops. End‑customers purchase the product, and feedback loops inform R&D for new flavors and formats.

What key investment insights can be drawn for the UAE Ice Cream Market?

Investors should consider growth in premium and artisanal segments, which command higher margins. Expanding into e‑commerce and direct‑to‑consumer delivery can capture the digitally engaged demographic. Partnerships with local dairy producers can mitigate raw‑material risks, while adopting eco‑friendly packaging can differentiate brands. The projected CAGR of 3.90 % underscores a stable return environment.

What is the conclusion for the UAE Ice Cream Market?

The UAE Ice Cream Market is on a clear upward trajectory, supported by affluent consumers, tourism recovery, and a shift toward premium, health‑conscious products. The market’s modest CAGR and solid base of both global and local players create a competitive yet opportunity‑rich landscape. Companies that innovate in flavor, sustainability, and digital distribution are poised to capture the most share.

How was the research methodology conducted for this report?

The study combined primary interviews with industry experts, retailers, and consumer panels, alongside secondary data collection from company reports, trade publications, and government statistics. Trend analysis, forecasting models, and competitive benchmarking were applied to derive the market size, growth rates, and segment insights.

What is the scope of the research?

The research covers the UAE ice‑cream market from 2026 baseline through 2033 forecast, encompassing product type, distribution channel, and key player analysis. Geographic focus is limited to the United Arab Emirates, with regional context provided for the Middle East. The study excludes unrelated frozen dessert categories such as frozen yogurts.

Who are the key companies and what recent developments have they announced?

Desert Chill Ice Cream LLC recently launched a line of halal‑certified artisanal flavors targeting upscale dining venues. Dunkin' Brands, Inc. expanded its menu to include seasonal ice‑cream beverages in its UAE stores. General Mills, Inc. introduced a low‑sugar, high‑protein ice‑cream range. IFFCO announced a joint venture with a local dairy farm to secure stable milk supply. MARS Incorporated rolled out a limited‑edition chocolate‑coated ice‑cream bar in partnership with a regional retailer. MINI Melts Inc. increased its impulse‑pack distribution in convenience stores, and Nestlé launched a recyclable packaging program across its UAE product portfolio.