What is the Broth Market Overview – definition, scope, and significance?

The broth market comprises ready‑to‑consume and concentrate liquids derived from simmering animal bones, meat, seafood, or vegetables. It includes product categories such as chicken, beef, seafood, and vegetable broths, offered in organic and conventional forms, and distributed through supermarkets, convenience stores, and online channels. The market’s significance lies in its role as a foundational ingredient for culinary applications, a convenient source of nutrition, and a growing segment of the broader soup and beverage industry. With evolving consumer preferences for clean‑label, functional, and ready‑to‑use products, broth has become a strategic growth engine for food manufacturers worldwide.

What are the primary drivers, restraints, challenges, and opportunities in the Broth Market?

Key drivers include rising demand for protein‑rich, low‑fat options, increased awareness of bone broth’s health benefits, and the shift toward at‑home cooking accelerated by convenience trends. Restraints stem from the relatively high price of premium organic broths and supply chain constraints for quality raw materials. Challenges involve stringent food safety regulations, consumer skepticism about labeling claims, and competition from alternative liquid seasonings. Opportunities arise from product innovation (e.g., functional blends with added vitamins or adaptogens), expansion of online retail, and entry into emerging markets where traditional broth consumption is culturally embedded.

What are the current and emerging growth trends shaping the Broth Market?

Current trends feature a surge in “clean‑label” formulations, with consumers favoring organic and minimally processed broths. There is a notable rise in plant‑based broth alternatives that mimic chicken or beef flavor while catering to vegetarians and flexitarians. Emerging trends include fortified broths enriched with collagen, electrolytes, or herbal extracts, and the use of sustainable packaging such as recyclable cartons and glass jars. Additionally, personalized nutrition platforms are prompting brands to offer single‑serve, portion‑controlled packs for on‑the‑go consumption.

How did COVID‑19 impact the Broth Market, and what is the recovery trajectory?

The pandemic created a temporary spike in demand as consumers stocked up on shelf‑stable, easy‑to‑prepare foods, boosting broth sales in both supermarkets and online channels. Supply chain disruptions initially affected raw material availability, but manufacturers adapted by diversifying sourcing. Post‑pandemic, demand has stabilized but remains elevated compared to pre‑COVID levels, driven by continued interest in immune‑supporting foods. The market is on a steady recovery path, with growth projected to accelerate as consumers maintain home‑cooking habits and prioritize health‑focused products.

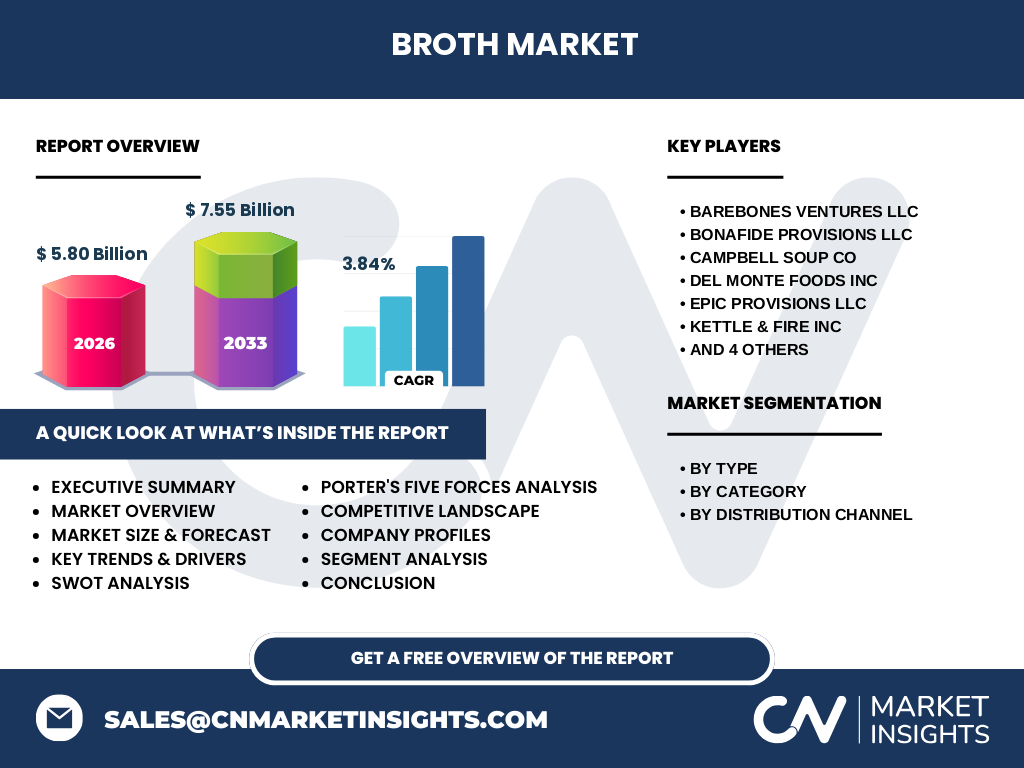

Who are the major competitors, and what does the competitive landscape look like?

The broth market is moderately consolidated, featuring a mix of large multinational food companies and niche specialty producers. Key players include Campbell Soup Co, Del Monte Foods Inc, Kettle & Fire Inc, The Hain Celestial Group Inc, and emerging brands such as Barebones Ventures LLC, Bonafide Provisions LLC, Epic Provisions LLC, Look’s Gourmet Food Company Inc, The Manischewits Co, and Zoup Specialty Products LLC. Competition centers on product differentiation, organic certification, flavor authenticity, and distribution reach. Recent strategic moves involve partnerships with online retailers, expansion of organic lines, and acquisition of smaller specialty brands to broaden portfolios.

What are the high‑level findings in the Executive Summary?

The broth market is valued at USD 5.80 billion in 2026 and is forecast to reach USD 7.55 billion by 2033, reflecting a CAGR of 3.84 %. Growth is propelled by health‑centric consumer trends, expanding online sales, and product innovation across organic and functional segments. While price sensitivity and regulatory compliance pose challenges, opportunities in fortified formulations and sustainable packaging are poised to drive further expansion. The market remains attractive for investors seeking exposure to the fast‑growing ready‑to‑eat and functional foods categories.

What are the market forecasts for 2025‑2032?

Based on the provided CAGR of 3.84 %, the broth market is expected to continue its upward trajectory throughout the 2025‑2032 horizon. By 2032, the market size is projected to approximate USD 7.2 billion, maintaining a steady growth pace that outpaces many traditional soup categories. This sustained expansion is underpinned by continued demand for organic and functional broths, as well as the widening reach of e‑commerce platforms that simplify consumer access.

How is the Broth Market sized and shared by segmentation?

Segmentation by type shows four primary product families: chicken broth, beef broth, seafood broth, and vegetable broth. By category, the market splits into organic and conventional offerings, with organic broths capturing a premium niche due to higher consumer willingness to pay for clean‑label attributes. Distribution channels are divided among supermarkets and hypermarkets, convenience stores, and online retail, the latter experiencing the fastest growth rate as digital grocery adoption accelerates.

What is the global market size and share by region?

While specific regional dollar values are not disclosed, the global broth market’s USD 5.80 billion valuation reflects strong participation across North America, Europe, and Asia‑Pacific. These regions collectively dominate consumption due to established culinary traditions that incorporate broth, robust retail infrastructures, and high disposable incomes that support premium organic products.

What does the regional analysis reveal about market performance?

North America leads in organic broth adoption, driven by health‑conscious consumers and extensive distribution networks. Europe follows closely, with a growing emphasis on sustainable sourcing and regulatory standards that favor clean‑label products. The Asia‑Pacific region presents the most significant growth potential, as traditional broth consumption aligns with modern convenience formats, and rising middle‑class incomes spur demand for premium packaged options. Latin America and the Middle East are emerging markets where local flavors and increased retail penetration are beginning to shape broth sales.

What are the profiles of leading companies in the Broth Market?

Campbell Soup Co leverages its extensive distribution and brand equity to offer a broad range of conventional broths. Kettle & Fire Inc specializes in premium organic bone broths with functional claims. The Hain Celestial Group Inc focuses on natural and organic product lines, targeting health‑focused shoppers. Smaller innovators such as Barebones Ventures LLC and Epic Provisions LLC differentiate through specialty flavors and sustainable packaging. These companies employ strategies ranging from product line extensions to strategic alliances with online platforms to capture market share.

How does Porter’s Five Forces framework assess the Broth Market?

Threat of New Entrants: Moderate – low capital requirements for niche brands, but scale and distribution pose barriers. Bargaining Power of Suppliers: Moderate – reliance on high‑quality meat, seafood, and organic vegetables can give suppliers leverage. Bargaining Power of Buyers: High – retailers and end‑consumers demand competitive pricing and quality, driving brands to innovate. Threat of Substitutes: Moderate – alternative flavor bases like bouillon cubes and plant‑based sauces compete, yet broth’s functional image sustains demand. Industry Rivalry: Intense – numerous players vie for shelf space, differentiation, and shelf‑stable innovation.

What are the SWOT findings for the Broth Market?

Strengths: Strong health narrative, versatile culinary use, growing premium segment. Weaknesses: Higher cost of organic ingredients, limited awareness of functional benefits among some consumer groups. Opportunities: Development of fortified and plant‑based broths, expansion into emerging markets, leveraging e‑commerce growth. Threats: Price pressure from conventional soups, supply chain volatility for animal‑based raw materials, potential regulatory scrutiny of health claims.

How is the Broth Market value chain structured?

The value chain begins with raw material sourcing (livestock, seafood, vegetables), followed by processing (simmering, concentration, sterilization). Next comes formulation, where flavors and functional ingredients are added. Packaging and labeling then create the final product, which is distributed through wholesale channels to supermarkets, convenience stores, and direct‑to‑consumer online platforms. Post‑sale services include consumer feedback loops that inform product refinement and new line development.

What key investment insights emerge for potential investors?

Investors should focus on companies with diversified portfolios across organic and conventional segments, strong e‑commerce capabilities, and proven track records of product innovation. Brands that secure sustainable sourcing and transparent labeling are better positioned for long‑term growth. Strategic investments in emerging market entrants or joint ventures that enhance distribution reach can yield outsized returns as the market expands beyond mature regions.

What are the main conclusions drawn from the research?

The broth market is on a solid growth trajectory, underpinned by health‑oriented consumer trends and expanding digital distribution. While price sensitivity and regulatory considerations present challenges, the sector offers considerable upside through product innovation, geographic expansion, and sustainability initiatives. Stakeholders that align with these dynamics are likely to capture a meaningful share of the projected USD 7.55 billion market by 2033.

What methodology was used to compile this research?

The study combined primary interviews with industry experts, secondary analysis of company reports, trade publications, and market databases. Quantitative data were cross‑validated against publicly available financial statements and forecast models applying the stated CAGR of 3.84 %. Qualitative insights were derived from trend monitoring, consumer surveys, and supply chain assessments.

What is the scope of this research?

The report covers global broth products segmented by type, category, and distribution channel, focusing on the period 2026‑2033. It includes competitive analysis, regional performance, and strategic recommendations. The scope excludes detailed pricing studies and proprietary formulation specifics, concentrating instead on market size, growth drivers, and strategic outlook.

Which key companies and recent developments are highlighted in the Broth Market?

Major players such as Campbell Soup Co and Kettle & Fire Inc have launched new organic, low‑sodium lines in 2022‑2023. The Hain Celestial Group Inc announced a partnership with a leading online grocer to accelerate direct‑to‑consumer sales. Smaller innovators like Barebones Ventures LLC introduced a line of bone broth infused with adaptogenic herbs, while Epic Provisions LLC expanded its distribution to convenience stores across the Midwest. These developments illustrate the market’s dynamic nature and the emphasis on innovation, sustainability, and channel diversification.