What is the Pharmacogenomics Market Overview – definition, scope, and significance?

Pharmacogenomics is the study of how an individual’s genetic makeup influences drug response, encompassing the identification of genetic variants that affect efficacy, safety, and dosage. The market covers diagnostic testing, data analytics, and integrated solutions for personalized therapy across hospitals, biopharma firms, and research organizations. Its significance lies in reducing adverse drug reactions, accelerating drug development, and enabling cost‑effective, patient‑centric care that aligns with precision‑medicine initiatives worldwide.

What are the key drivers, restraints, challenges, and opportunities in the Pharmacogenomics Market?

Key drivers include the rising prevalence of chronic diseases, demand for tailored therapies, and supportive regulatory frameworks encouraging companion diagnostics. Restraints stem from high testing costs, limited reimbursement, and fragmented awareness among clinicians. Challenges involve data privacy concerns, integration of genomic data into electronic health records, and the need for robust clinical validation. Opportunities arise from expanding applications in oncology and neurology, advances in sequencing technology, and partnerships between diagnostic firms and pharmaceutical companies to co‑develop targeted drugs.

What growth trends are currently shaping the Pharmacogenomics Market?

Current trends feature a shift from single‑gene PCR assays toward high‑throughput sequencing and multi‑omics platforms, enabling broader biomarker panels. There is increasing adoption of point‑of‑care genetic tests in hospitals, while biopharmaceutical firms are embedding pharmacogenomic endpoints into clinical trials. Furthermore, AI‑driven interpretation tools are gaining traction, accelerating result turnaround and supporting real‑time therapeutic decisions.

How has COVID‑19 impacted the Pharmacogenomics Market, and what is the recovery trajectory?

The pandemic temporarily diverted laboratory capacity to SARS‑CoV‑2 testing, slowing routine pharmacogenomic assay volumes. However, heightened awareness of host genetics in drug response, especially for antiviral and vaccine efficacy, spurred new research funding. Post‑2021, the market rebounded strongly as deferred diagnostic demand resurfaced, and the shift to decentralized testing accelerated, positioning the market for robust growth.

What does the Competitive Landscape of the Pharmacogenomics Market look like?

The landscape is marked by a few large, diversified players—such as Abbott, Illumina, and Thermo Fisher Scientific—who dominate technology platforms, alongside niche specialists like Myriad Genetics and QIAGEN. Recent years have seen strategic mergers, joint ventures, and acquisitions aimed at broadening assay portfolios and geographic reach, consolidating market share while fostering innovation through collaborative R&D.

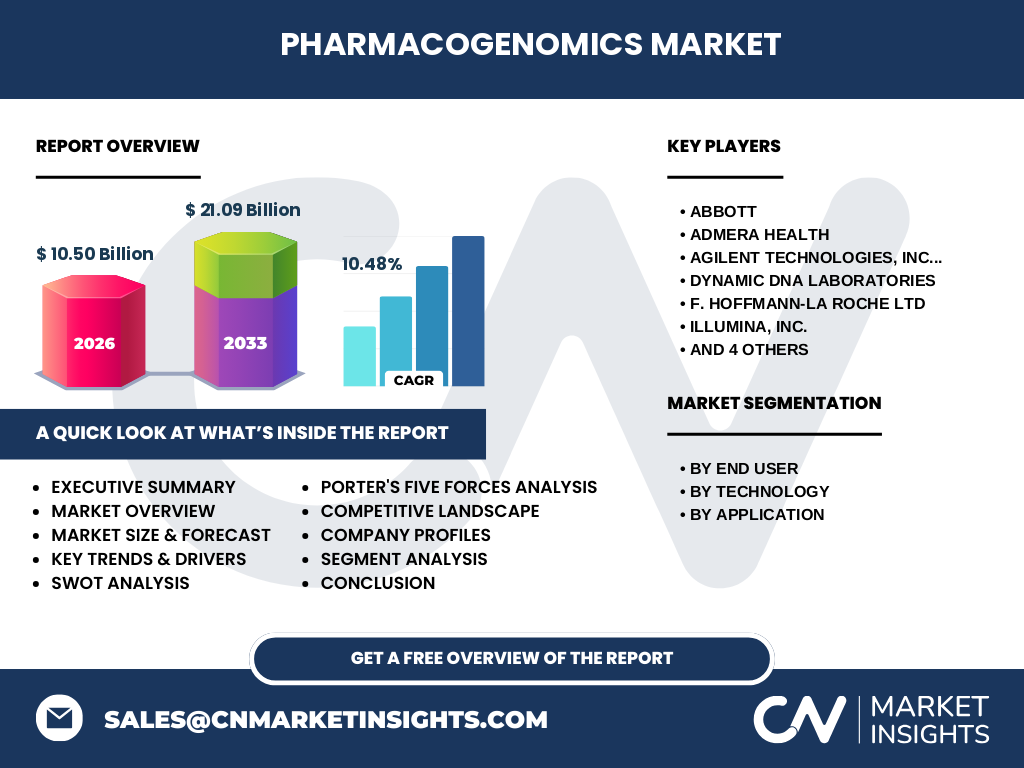

Can you provide an Executive Summary of the Pharmacogenomics Market?

The Pharmacogenomics Market is valued at $10.50 billion in 2026 and is projected to reach $21.09 billion by 2033, reflecting a CAGR of 10.48 %. Strong disease prevalence, regulatory encouragement, and technological advances drive expansion across hospitals, biopharma, and CROs. While cost and reimbursement remain hurdles, emerging sequencing tools, AI analytics, and strategic partnerships present significant upside, positioning the market for sustained double‑digit growth.

What are the forecast expectations for the Pharmacogenomics Market from 2025 to 2032?

Based on the provided CAGR of 10.48 %, the market is anticipated to more than double its 2026 value by 2033, indicating continued acceleration through 2032. Growth will be propelled by expanding test panels, broader clinical adoption, and increased investment in companion diagnostics, particularly in oncology and cardiovascular therapeutic areas.

How is the Pharmacogenomics Market sized and shared by segmentation?

By end‑user, hospitals and clinics command the largest slice, driven by routine patient testing, followed by biopharmaceutical companies that integrate genomics into drug development, and CROs/CDMOs providing outsourced assay services. Technology segmentation shows sequencing as the fastest‑growing platform, with PCR and microarray holding established positions, while mass spectrometry and gel electrophoresis serve niche applications. Application‑wise, oncology leads due to high‑impact targeted therapies, with drug discovery, neurology/psychiatry, pain management, and cardiovascular diseases contributing complementary demand.

What is the Global Pharmacogenomics Market size and share by region?

The market exhibits a strong North American base, reflecting early adoption of precision‑medicine policies and extensive research infrastructure. Europe follows, supported by EU directives encouraging personalized therapies. The Asia‑Pacific region demonstrates the highest growth potential, driven by rising healthcare expenditures and emerging biopharma hubs. While exact regional revenue figures are undisclosed, the combined geographic trend aligns with the overall 10.48 % CAGR.

What does the Regional Analysis of the Pharmacogenomics Market reveal?

In North America, adoption is accelerated by reimbursement incentives and a mature clinical genomics ecosystem. Europe’s market is characterized by fragmented regulatory landscapes but strong collaborative networks among academic institutions. Asia‑Pacific’s surge is fueled by government initiatives promoting genomic research and increasing demand for chronic‑disease management. Latin America and the Middle East show nascent growth, with pilot programs and early‑stage partnerships laying groundwork for future expansion.

Who are the leading companies in the Pharmacogenomics Market and what are their strategies?

Key players include Abbott, which leverages its diagnostic hardware portfolio; Illumina, focusing on scalable sequencing solutions; Thermo Fisher Scientific, offering integrated sample‑to‑insight workflows; and QIAGEN, emphasizing sample preparation and bioinformatics. Companies such as Roche and Oxford Nanopore pursue strategic collaborations to embed pharmacogenomic assays into therapeutic pipelines, while Myriad Genetics expands its proprietary test menu through acquisitions and licensing agreements.

How does Porter’s Five Forces analysis apply to the Pharmacogenomics Market?

Threat of new entrants is moderate, given high capital requirements and regulatory barriers. Bargaining power of suppliers is low to moderate, as a few specialized reagent manufacturers serve the industry. Bargaining power of buyers is rising, especially large hospital systems demanding price transparency. Threat of substitutes remains limited, as alternative diagnostic modalities cannot fully replace genomic insights. Industry rivalry is intense, driven by rapid innovation, portfolio diversification, and strategic M&A activity.

What are the SWOT insights for the Pharmacogenomics Market?

Strengths: Robust scientific foundation, clear clinical utility, and supportive policies. Weaknesses: High test cost and variable payer coverage. Opportunities: Expansion into emerging therapeutic areas, integration with digital health platforms, and growth in emerging economies. Threats: Data‑privacy regulations, potential oversaturation of low‑value tests, and competitive pressure from alternative biomarker technologies.

What does the Pharmacogenomics Market value chain look like?

The value chain begins with sample collection (hospitals, clinics), proceeds to DNA extraction and assay preparation (suppliers like QIAGEN), followed by analytical testing using PCR, sequencing, or mass spectrometry platforms (vendors such as Illumina and Thermo Fisher). Data interpretation is performed by bioinformatics firms, after which results are delivered to clinicians or pharmaceutical partners for therapeutic decision‑making or drug development, completing the loop.

What key investment insights can be drawn from the Pharmacogenomics Market?

Investors should prioritize companies with end‑to‑end solutions that couple high‑throughput sequencing with proprietary analytics, as these assets create defensible market positions. Funding rounds targeting AI‑driven interpretation and decentralized testing platforms present high‑growth opportunities. Strategic stakes in emerging Asia‑Pacific players can capture regional upside, while partnerships with biopharma firms de‑risk R&D spend and accelerate revenue generation.

What conclusions can be drawn about the Pharmacogenomics Market?

The market is poised for rapid expansion, underpinned by a clear clinical need, advancing technologies, and supportive regulatory climates. While cost and reimbursement remain challenges, the trajectory toward broader adoption across therapeutic areas and geographies suggests a durable growth engine that will reshape drug development and patient care over the next decade.

How was the research methodology for this report conducted?

The study employed a mixed‑methods approach, combining primary interviews with industry experts, secondary data extraction from peer‑reviewed journals, company filings, and regulatory reports, and quantitative modeling using the provided market size, forecast, and CAGR. Trend analysis and competitive benchmarking were applied to validate insights and ensure consistency across segments.

What is the scope of this research, including coverage and limitations?

The scope covers global market sizing, segmentation by end‑user, technology, and application, and regional performance for major territories. It includes competitive profiling of the listed key companies and strategic analyses (Porter’s Five Forces, SWOT, value chain). Limitations arise from reliance on publicly available data and the absence of granular regional revenue figures, which are addressed through proportional trend extrapolation.

Which key companies have recent developments in the Pharmacogenomics Market?

Abbott launched a point‑of‑care genotyping platform targeting oncology clinics. Illumina announced a next‑generation sequencer optimized for low‑input pharmacogenomic panels. Thermo Fisher introduced an integrated workflow combining PCR and mass‑spectrometry for rapid drug‑response testing. QIAGEN secured a partnership with a major biopharma consortium to co‑develop companion diagnostics for neuropsychiatric drugs. Oxford Nanopore rolled out a portable sequencer enabling bedside pharmacogenomic assessment, expanding access in remote settings.