What is the Malaria Diagnostics Market Overview – definition, scope, and significance?

The Malaria Diagnostics Market encompasses all products, technologies, and services used to detect Plasmodium infections in humans. It includes microscopy, rapid diagnostic tests (RDTs), and molecular diagnostic platforms supplied to hospitals, clinics, and diagnostic centers worldwide. The market’s significance lies in its role of enabling timely treatment, reducing malaria‑related mortality, and supporting public‑health surveillance programs, especially in endemic regions where accurate diagnosis is critical for disease control and elimination efforts.

What are the key drivers, restraints, challenges, and opportunities shaping the Malaria Diagnostics Market?

Key drivers include rising incidence of malaria in low‑income regions, increased government spending on disease‑control programs, and growing demand for point‑of‑care RDTs. Restraints stem from limited healthcare infrastructure and low purchasing power in endemic countries. Challenges involve the need for high‑sensitivity molecular tests and supply‑chain disruptions. Opportunities arise from innovations in multiplex testing, integration of digital health solutions, and expanding private‑sector partnerships that can accelerate market penetration.

What growth trends are currently influencing the Malaria Diagnostics Market?

Current trends feature a shift toward rapid diagnostic tests due to their ease of use and short turnaround time, while molecular diagnostics gain traction for confirming low‑parasite‑density infections. Manufacturers are also investing in portable microscopy devices that combine high resolution with field usability. Additionally, there is an emerging emphasis on combining malaria testing with other febrile illness panels, supporting broader infectious‑disease diagnostics.

How has COVID‑19 impacted the Malaria Diagnostics Market, and what is the recovery trajectory?

The COVID‑19 pandemic diverted resources and disrupted supply chains, temporarily slowing malaria testing activities and delaying new product launches. However, heightened awareness of infectious‑disease diagnostics and increased funding for health‑system resilience have accelerated post‑pandemic recovery. Market participants are now leveraging lessons learned to improve rapid test distribution networks, positioning the market for renewed growth.

Who are the major competitors in the Malaria Diagnostics Market and what is the state of market consolidation?

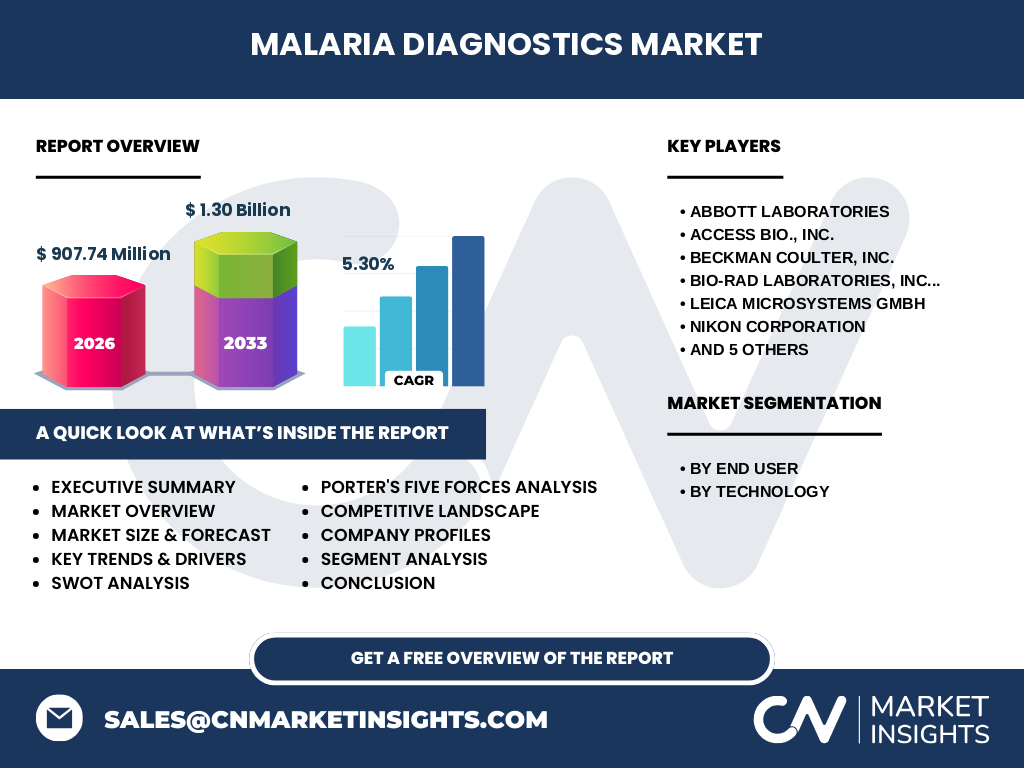

Key competitors include Abbott Laboratories, Access Bio., Inc., Beckman Coulter, Inc., Bio‑Rad Laboratories, Inc., Leica Microsystems GmbH, Nikon Corporation, Olympus Corporation, Premier Medical Corporation Pvt. Ltd., Siemens Healthineers, Sysmex Partec GmbH, and bioM√©rieux. The market remains moderately fragmented, with leading firms focusing on product diversification and strategic alliances rather than large‑scale mergers, resulting in a competitive yet collaborative landscape.

What are the high‑level insights presented in the Executive Summary?

The Executive Summary highlights a market valued at US 907.74 million in 2026, projected to reach US 1.30 billion by 2033, reflecting a 5.30 % CAGR. Growth is driven by expanding public‑health initiatives, rising adoption of rapid and molecular diagnostics, and increasing investment in underserved regions. Competitive dynamics are shaped by innovation and partnerships, while challenges such as infrastructure gaps persist. The outlook is positive, with significant upside from technology integration.

What are the forecast expectations for the Malaria Diagnostics Market from 2025 to 2032?

Based on the provided CAGR of 5.30 %, the market is expected to expand consistently through 2032, surpassing the US 1.30 billion mark by 2033. This steady growth reflects continued demand for accurate, rapid testing solutions, ongoing governmental and NGO funding, and the rollout of next‑generation molecular platforms that address low‑parasite‑density cases.

How is the Malaria Diagnostics Market sized and shared by segmentation?

Segmentation by end‑user shows hospitals and clinics as a primary channel, complemented by diagnostic centers that cater to high‑volume testing. By technology, microscopy remains a foundational method, rapid diagnostic tests dominate point‑of‑care settings, and molecular diagnostic tests are gaining market share due to superior sensitivity. Each segment contributes to the overall market value, with RDTs and molecular platforms driving the fastest growth.

What is the global geographic distribution of the Malaria Diagnostics Market?

The market is globally dispersed, with the highest concentration in malaria‑endemic regions of Africa, South‑East Asia, and parts of Latin America. Developed economies contribute through the supply of advanced microscopy and molecular equipment, while emerging markets are the primary consumers of rapid diagnostic tests, reflecting differing healthcare infrastructure and disease burden.

What does the regional analysis reveal about market performance?

Region‑specific analysis shows Africa leading in volume due to the highest disease prevalence, supported by extensive donor‑funded testing programs. Asia‑Pacific follows, driven by rapid urbanization and increased private‑sector healthcare spending. Europe and North America, though less affected by malaria, influence the market through R&D activities, production of high‑tech diagnostic instruments, and export of testing kits to endemic regions.

Which companies lead the Malaria Diagnostics Market and what are their strategic approaches?

Leading firms such as Abbott Laboratories and Siemens Healthineers focus on integrated diagnostics platforms and global distribution networks. Access Bio., Inc. and bioM√©rieux prioritize affordable rapid test kits tailored for low‑resource settings. Companies like Leica Microsystems and Nikon concentrate on high‑resolution microscopy solutions for reference laboratories. Strategic moves include product portfolio expansion, collaborations with NGOs, and localized manufacturing.

How does Porter’s Five Forces framework apply to the Malaria Diagnostics Market?

Threat of new entrants is moderate due to high regulatory barriers and capital requirements. Bargaining power of buyers is strong in low‑income markets where price sensitivity is high. Bargaining power of suppliers is limited, as raw material sources are abundant. Threat of substitutes is low, given the specialized nature of malaria testing. Industry rivalry is intense, driven by innovation, price competition, and the pursuit of government contracts.

What are the SWOT strengths, weaknesses, opportunities, and threats for the Malaria Diagnostics Market?

Strengths: Established demand, proven technologies, and strong public‑health backing. Weaknesses: Dependence on external funding, limited infrastructure in endemic zones. Opportunities: Emerging molecular platforms, digital health integration, and expansion into multi‑disease testing. Threats: Supply‑chain disruptions, emergence of drug‑resistant malaria strains, and competition from alternative disease‑control strategies.

What does the value chain of the Malaria Diagnostics Market look like?

The value chain begins with raw material suppliers (reagents, consumables), followed by R&D and manufacturing of diagnostic kits and instruments. Distribution channels include importers, wholesalers, and direct sales to hospitals, clinics, and diagnostic centers. End‑users perform the testing, generating data that feed back into public‑health surveillance systems, influencing policy and further investment.

What key investment insights can be drawn from the Malaria Diagnostics Market?

Investors should focus on companies delivering affordable rapid tests with scalable production, as these address the largest unmet need. Funding opportunities also exist in molecular diagnostics firms that can provide high‑sensitivity solutions for low‑parasite‑density cases. Strategic partnerships with governments and NGOs can de‑risk market entry, while digital health platforms that aggregate testing data present ancillary revenue streams.

What conclusions can be drawn about the Malaria Diagnostics Market?

The market exhibits robust growth, underpinned by a clear public‑health imperative and supportive funding environment. While infrastructure constraints remain, advances in rapid and molecular testing are expanding access. Competitive dynamics favor innovators who combine affordability with accuracy, and the projected CAGR of 5.30 % signals a healthy trajectory toward 2033.

How was the research for this report conducted?

The methodology combined primary interviews with industry experts, secondary data review from reputable databases, and analysis of published financial statements of key players. Trend extrapolation employed the specified CAGR, while segmental breakdowns were derived from product‑type and end‑user classifications provided by market respondents.

What is the scope of this research?

The study covers global market size, forecasts, segmentation by technology and end‑user, regional performance, and competitive dynamics. It excludes detailed financial ratios, proprietary pricing models, and country‑level macroeconomic projections, focusing instead on the overarching market structure and growth outlook.

Which key companies have recent developments in the Malaria Diagnostics Market?

Recent announcements include Abbott Laboratories launching a new high‑throughput malaria antigen assay, Access Bio., Inc. introducing an ultra‑low‑cost RDT for rural clinics, and Siemens Healthineers expanding its molecular platform portfolio with malaria‑specific cartridges. Bio‑Rad Laboratories announced a partnership with regional health ministries to supply microscopy kits, while bioM√©rieux released a next‑generation rapid test with improved sensitivity, reflecting ongoing innovation across the sector.