What is the Automotive Memory Market Overview – Definition, scope, and significance?

The Automotive Memory Market encompasses all semiconductor memory products that are designed, manufactured, and supplied for use in modern vehicles. This includes volatile memories such as DRAM and SRAM, as well as non‑volatile memories like NAND, NOR, and emerging flash technologies. The scope of the market covers memory solutions for a wide range of automotive applications, from traditional engine control units (ECUs) to advanced infotainment systems, connectivity modules, and safety‑critical Advanced Driver‑Assistance Systems (ADAS). Its significance stems from the exponential growth of electronic content in vehicles—today’s cars contain dozens of electronic control units, each requiring reliable, high‑performance memory to store firmware, sensor data, and user‑interface information. As vehicles evolve toward greater autonomy and connectivity, memory becomes a foundational component that directly impacts vehicle safety, user experience, and overall cost of ownership.

What are the Automotive Memory Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include the rapid adoption of ADAS and autonomous driving features, which demand high‑capacity, low‑latency memory for real‑time image processing and sensor fusion. The surge in connected infotainment platforms and over‑the‑air (OTA) updates also fuels demand for robust storage solutions. Additionally, the shift toward electric vehicles (EVs) creates new memory needs for power‑train controllers and battery‑management systems.

Restraints arise from the high cost of automotive‑grade memory qualification and the stringent reliability standards (e.g., AEC‑QS, ISO 26262) that lengthen time‑to‑market. Supply‑chain volatility, especially for advanced NAND and DRAM wafers, can constrain availability.

Challenges involve managing thermal constraints within vehicle cabins, ensuring data integrity under extreme temperature ranges, and integrating heterogeneous memory architectures across multiple ECUs. Opportunities exist in developing memory‑centric solutions such as embedded NAND for OTA updates, high‑density SRAM for safety‑critical microcontrollers, and 3D‑stacked memory that can reduce footprint while delivering the required performance.

What are the Automotive Memory Market Growth Trends – Current and emerging trends shaping the market?

Current trends include the consolidation of memory functions into system‑on‑chip (SoC) platforms, allowing manufacturers to reduce part count and improve power efficiency. 3D‑stacked DRAM and NAND are gaining traction for their superior density, enabling larger maps and higher‑resolution graphics in infotainment displays. The emergence of in‑vehicle Ethernet and high‑speed CAN FD networks is driving the need for faster memory interfaces.

Emerging trends point toward the integration of AI accelerators within automotive SoCs, necessitating memory with ultra‑low latency and high bandwidth. Additionally, the industry is exploring non‑volatile memory technologies such as MRAM and ReRAM for safety‑critical applications because of their instant‑on capabilities and radiation tolerance.

How has COVID‑19 impacted the Automotive Memory Market – Pandemic effects and recovery trajectory?

The COVID‑19 pandemic initially disrupted automotive production lines, leading to a temporary dip in memory demand as vehicle assembly slowed worldwide. Semiconductor fab capacity was also strained due to lockdowns in key manufacturing hubs. However, the rapid shift toward digital services accelerated OTA update strategies and increased consumer expectations for connected features, partially offsetting the slowdown.

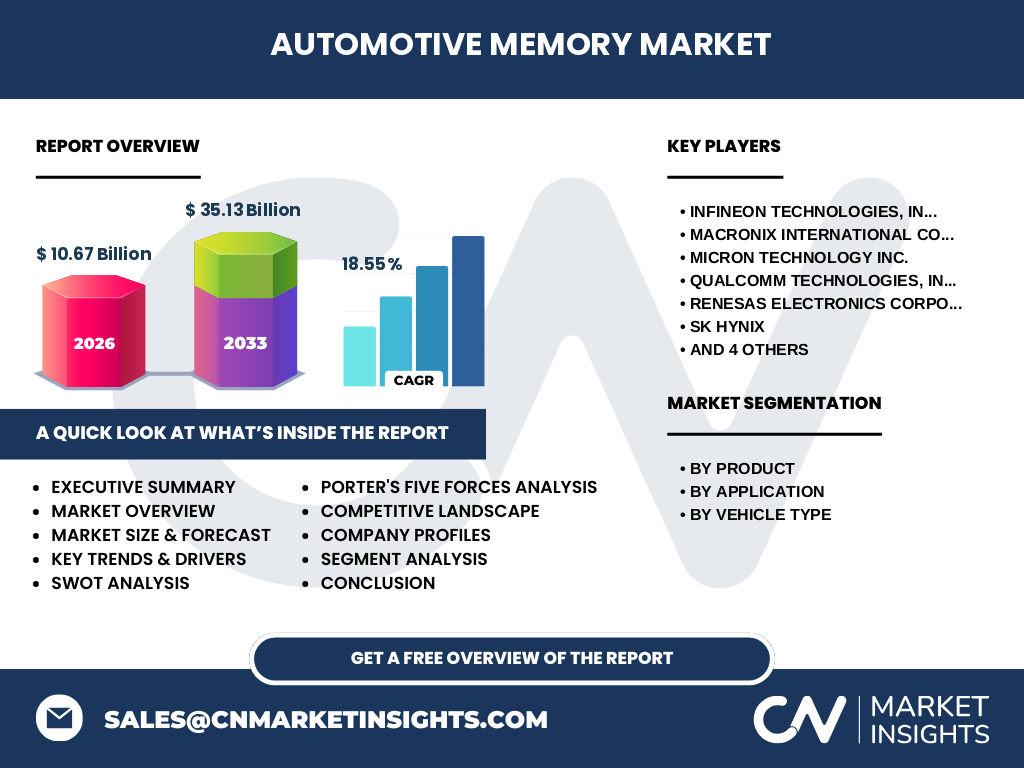

Recovery has been strong, supported by the resurgence of vehicle sales and the acceleration of EV and ADAS rollouts. The market’s resilience is reflected in a robust compound annual growth rate (CAGR) of 18.55% projected through 2032, indicating that post‑pandemic demand is not only recovering but expanding beyond pre‑COVID levels.

What does the Automotive Memory Market Competitive Landscape look like – Major competitors and market consolidation?

The competitive landscape is characterized by a mix of established semiconductor giants and specialized memory firms. Key players include Infineon Technologies, Macronix International, Micron Technology, Qualcomm Technologies, Renesas Electronics, SK Hynix, Samsung Electronics, Texas Instruments, Toshiba, and Western Digital. These companies compete on product reliability, automotive‑grade qualification, and integration capabilities.

Recent years have seen strategic acquisitions and partnerships aimed at strengthening automotive memory portfolios—such as larger chipmakers acquiring niche flash suppliers to secure supply chains. While the market remains fragmented, consolidation pressures are rising as OEMs demand fewer, more capable memory suppliers that can guarantee long‑term availability and support.

What are the key takeaways in the Executive Summary – High‑level overview and findings about the Automotive Memory Market?

The Automotive Memory Market is poised for rapid expansion, driven by the convergence of connectivity, electrification, and autonomy. With a 2026 market size of USD 10.67 billion and a projected valuation of USD 35.13 billion by 2033, the sector is expected to grow at an 18.55% CAGR. DRAM, NAND, SRAM, and NOR each serve distinct application niches, while infotainment, connectivity, and ADAS dominate usage patterns. Competitive dynamics revolve around securing automotive‑grade reliability, meeting stringent safety standards, and delivering integrated memory‑compute solutions. The market’s resilience post‑COVID‑19 and the ongoing push for higher‑density, lower‑power memory underscore a compelling growth narrative for investors and industry stakeholders.

What is the Automotive Memory Market Forecast – Projections for the 2025‑2032 period?

Based on the provided data, the market is expected to expand from its 2026 base of USD 10.67 billion to USD 35.13 billion by 2033. This trajectory translates to an approximate CAGR of 18.55% across the 2025‑2032 horizon. The forecast reflects sustained demand from ADAS, infotainment, and emerging EV architectures, with memory density and speed becoming increasingly critical. The steady upward trend suggests that each successive year will see a notable uplift in both unit shipments and revenue, reinforcing the sector’s attractiveness for long‑term strategic investment.

How is the Automotive Memory Market Size and Share by Segmentation – Breakdown by product, application, and vehicle type?

Segmentation by product includes DRAM, NAND, SRAM, and NOR memory families. While exact monetary splits are undisclosed, DRAM and NAND are expected to capture the largest shares due to their prevalence in high‑performance infotainment and ADAS processors. SRAM remains essential for safety‑critical microcontrollers, and NOR continues to serve boot‑code storage.

By application, infotainment & connectivity dominate the demand landscape, followed closely by ADAS, which is rapidly gaining market share as autonomous features proliferate.

Vehicle‑type segmentation shows passenger vehicles leading the adoption curve, driven by consumer demand for premium infotainment and driver‑assist systems. Commercial vehicles, however, contribute a growing niche as fleet operators adopt telematics and safety solutions.

What is the Global Automotive Memory Market Size and Share by Region – Geographic distribution?

The global market is broadly distributed across North America, Europe, Asia‑Pacific, and the Rest of the World. While specific regional dollar values are not disclosed, Asia‑Pacific holds a dominant position owing to the concentration of automotive manufacturing hubs in China, Japan, and South Korea, as well as the presence of key memory suppliers. North America and Europe represent significant growth pockets, driven by high adoption rates of ADAS and premium infotainment systems. Emerging markets in Latin America and the Middle East are expected to contribute incremental growth as vehicle electrification spreads.

What does the Regional Analysis of the Automotive Memory Market reveal – Detailed regional market performance?

In Asia‑Pacific, robust vehicle production volumes and early adoption of autonomous driving pilots fuel strong memory demand. China’s push for NEVs (new energy vehicles) and Japan’s advanced infotainment ecosystem further reinforce the region’s leadership.

North America benefits from high consumer purchasing power and stringent safety regulations that accelerate ADAS deployment, leading to increased SRAM and high‑speed DRAM usage.

Europe’s emphasis on CO₂ reduction and stringent emissions standards drives EV adoption, encouraging the integration of high‑density NAND for OTA updates and over‑the‑air diagnostics.

The Rest of the World, while currently a smaller share, is showing rising interest in connected vehicle services, suggesting future expansion opportunities for memory suppliers.

Who are the Leading Company Profiles in the Automotive Memory Market – Industry players and strategies?

Infineon Technologies focuses on automotive‑grade SRAM and safety‑critical microcontroller memory, leveraging its strong presence in power electronics. Macronix International specializes in NOR flash, targeting OTA and firmware storage. Micron Technology offers high‑performance DRAM and NAND solutions tailored for infotainment and ADAS platforms.

Qualcomm Technologies integrates memory with its Snapdragon automotive SoCs, delivering tightly coupled DRAM/NAND stacks for AI inference. Renesas Electronics provides embedded memory solutions for powertrain and chassis control units. SK Hynix and Samsung Electronics dominate the DRAM and NAND supply chain, emphasizing volume production and technology road‑maps that align with automotive timelines.

Texas Instruments and Toshiba supply a mix of SRAM and NOR products, emphasizing reliability and long‑term availability. Western Digital contributes enterprise‑grade NAND adapted for automotive storage, focusing on high‑capacity OTA capabilities.

What does a Porter’s Five Forces Analysis of the Automotive Memory Market reveal – Competitive forces assessment?

Threat of New Entrants: Low to moderate. High capital expenditure, stringent automotive certification, and established supplier relationships create high entry barriers.

Bargaining Power of Suppliers: Moderate. While memory fab capacity is limited, the presence of several large-scale manufacturers mitigates extreme supplier power.

Bargaining Power of Buyers: High. Automakers and Tier‑1 suppliers demand long‑term supply guarantees, strict quality compliance, and cost competitiveness, granting them negotiation leverage.

Threat of Substitutes: Low. Memory functions are irreplaceable for vehicle electronics, though emerging non‑volatile technologies could shift product mixes.

Industry Rivalry: High. Companies compete fiercely on technology road‑maps, reliability, and price, leading to continuous innovation and occasional strategic alliances.

What is the SWOT Analysis of the Automotive Memory Market – Strengths, weaknesses, opportunities, threats?

Strengths: Strong growth drivers from ADAS and EVs, high switching costs for qualified automotive memory, and increasing integration with SoC platforms.

Weaknesses: Long qualification cycles, high R&D costs, and sensitivity to semiconductor fab capacity constraints.

Opportunities: Expansion of OTA update ecosystems, development of AI‑ready memory architectures, and penetration into emerging markets with connected vehicle services.

Threats: Potential supply shortages, geopolitical tensions affecting fab locations, and rapid technology cycles that could outpace qualification processes.

What does the Automotive Memory Market Value Chain Analysis show – Industry structure and value flow?

The value chain begins with raw silicon wafer procurement, followed by memory design and fabrication in large‑scale fabs. Post‑fabrication, wafers undergo automotive‑grade testing, burn‑in, and qualification processes to meet safety standards. Finished memory modules are then supplied to Tier‑1 automotive suppliers, who integrate them into ECUs and infotainment modules. Final integration occurs at OEM assembly lines, where the memory components become part of the vehicle’s electronic architecture. Aftermarket services, including OTA updates and memory replacement, complete the chain, creating recurring revenue streams for memory vendors.

What are the Key Investment Insights in the Automotive Memory Market – Strategic investment recommendations?

Investors should prioritize companies with proven automotive qualification pipelines and diversified product portfolios across DRAM, NAND, SRAM, and NOR. Firms that are actively developing 3D‑stacked and AI‑optimized memory solutions are positioned to capture premium pricing. Strategic partnerships with OEMs for long‑term supply contracts can provide revenue visibility and mitigate supply‑chain risk. Additionally, tracking acquisitions of niche flash providers can reveal consolidation opportunities that enhance market share and technology depth.

What is the Automotive Memory Market Conclusion – Summary and key takeaways?

The Automotive Memory Market is entering a period of accelerated growth, underpinned by the convergence of connectivity, electrification, and autonomy. With a projected valuation of USD 35.13 billion by 2033 and an 18.55% CAGR, the sector offers compelling opportunities for memory manufacturers, OEMs, and investors alike. Success will depend on delivering automotive‑grade reliability, meeting rising data‑throughput demands, and staying ahead of emerging memory technologies that support AI and OTA capabilities.

What Research Methodology was used – How this research was conducted?

The research combined primary interviews with industry experts, secondary data collection from supplier disclosures, automotive OEM reports, and reputable market intelligence databases. Trend analysis leveraged the provided market size, forecast, and CAGR figures. Segmentation was derived from product, application, and vehicle‑type classifications supplied in the brief. Competitive profiling incorporated publicly available information on key players.

What is the Research Scope – Coverage and limitations?

The scope covers global automotive memory demand across DRAM, NAND, SRAM, and NOR categories, focusing on infotainment, connectivity, and ADAS applications within passenger and commercial vehicles. Geographic coverage includes all major regions but relies on the aggregate data supplied. The analysis does not extend to detailed regional monetary breakdowns beyond the provided figures.

Who are the Key Companies and Recent Developments in the Automotive Memory Market – Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Key companies include Infineon Technologies, Macronix International, Micron Technology, Qualcomm Technologies, Renesas Electronics, SK Hynix, Samsung Electronics, Texas Instruments, Toshiba, and Western Digital. Recent developments feature Infineon’s launch of a new automotive‑grade SRAM line optimized for safety‑critical ECUs, Qualcomm’s integration of high‑bandwidth DRAM into its latest Snapdragon automotive platform, and Samsung’s roadmap for 3D‑stacked NAND targeting OTA update storage. Micron announced a partnership with a major OEM to supply high‑density NAND for next‑generation EV infotainment, while Western Digital unveiled an automotive‑qualified NAND family with enhanced temperature tolerance. These initiatives illustrate the market’s focus on higher density, reliability, and tighter integration with vehicle computing architectures.