1. What is the Childcare Management Software Market – definition, scope, and significance?

The Childcare Management Software (CMS) market comprises digital platforms that streamline administrative, instructional, and communication functions for childcare providers. Solutions cover family engagement, child data management, attendance tracking, accounting, time scheduling, activity coordination, and nutrition oversight. Deployments are offered either on‑premise or via cloud services, and applications span daycare centers, before‑ and after‑school programs, preschools, and seasonal camps. The market is significant because it enhances operational efficiency, ensures regulatory compliance, improves parent‑provider communication, and supports data‑driven decision‑making, thereby raising the overall quality of early‑childhood education and care.

2. What are the key drivers, restraints, challenges, and opportunities shaping the Childcare Management Software market?

Key drivers include rising enrollment in early‑education programs, heightened demand for transparent billing and attendance reporting, and increasing adoption of cloud‑based solutions that reduce IT overhead. Regulatory pressures for accurate child‑record keeping and health‑safety compliance also push providers toward automation. Restraints involve budget constraints of small providers and concerns over data privacy. Challenges arise from fragmented market adoption and the need for integration with legacy school information systems. Opportunities exist in developing AI‑enabled analytics for child development insights, expanding mobile‑first parent portals, and tailoring solutions for emerging markets where formal childcare is growing rapidly.

3. What current and emerging trends are influencing the growth of the Childcare Management Software market?

Current trends feature a shift toward cloud‑native platforms that deliver real‑time updates and multi‑device accessibility. Providers are increasingly demanding integrated suites that combine attendance, billing, and nutrition modules into a single dashboard. Emerging trends include AI‑driven predictive analytics for enrollment forecasting, blockchain for secure record verification, and the incorporation of IoT sensors to monitor classroom environments. Gamified parent communication tools and customizable learning activity trackers are also gaining traction, reflecting a broader focus on engagement and outcome measurement.

4. How did COVID‑19 affect the Childcare Management Software market and what is the recovery trajectory?

The pandemic accelerated digital transformation as providers sought contact‑less check‑in, remote billing, and virtual parent communication. Demand for cloud solutions surged due to the need for rapid scalability and remote access. Although enrollment dipped during lockdowns, the market rebounded as families returned to onsite care, now expecting higher standards of health monitoring and real‑time reporting. Recovery is strong, with providers investing in enhanced hygiene tracking modules and integrated health dashboards, positioning the market for sustained post‑pandemic growth.

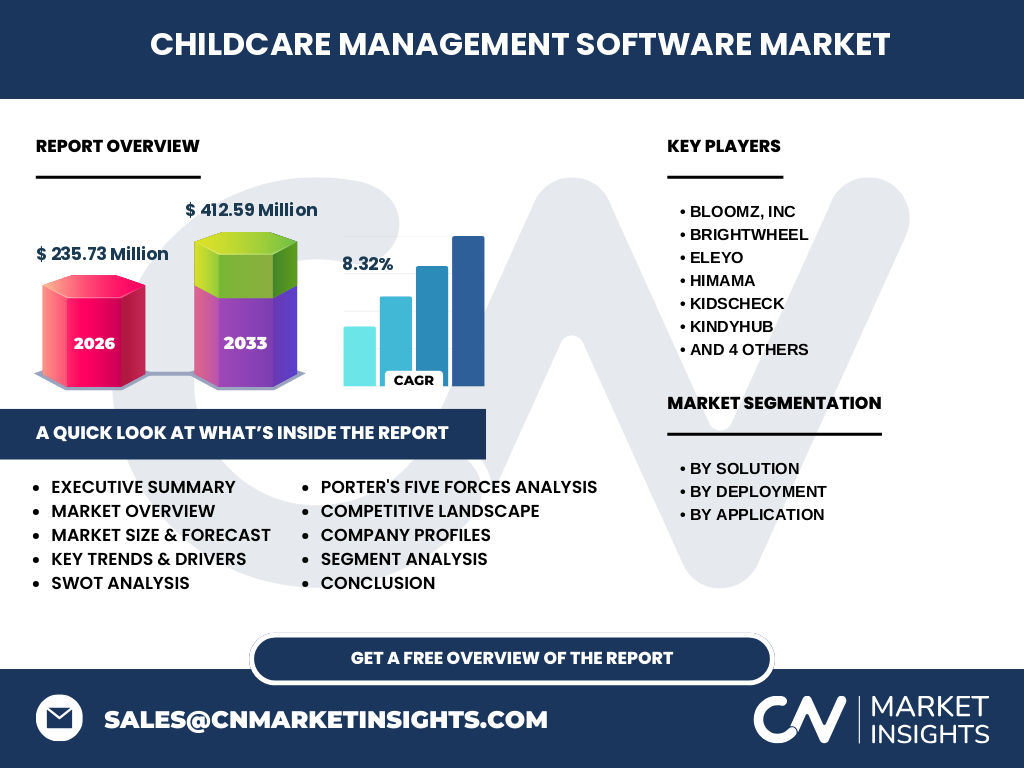

5. Who are the major competitors and what is the level of consolidation in the Childcare Management Software market?

The market is moderately consolidated with several well‑established vendors and a growing number of niche innovators. Leading players include Bloomz, Inc., Brightwheel, Eleyo, Himama, Kidscheck, Kindyhub, Kwiksol Corporation, Oncare, Procare Solutions, and iclasspro. These companies compete on feature depth, user experience, and deployment flexibility. Recent activity shows strategic partnerships and selective acquisitions aimed at expanding functionality (e.g., adding nutrition modules) and entering new geographic segments, indicating a trend toward broader, integrated platforms.

6. What are the high‑level highlights and key findings of the Childcare Management Software market?

The market reached a size of $235.73 million in 2026 and is projected to grow to $412.59 million by 2033, reflecting a robust CAGR of 8.32 %. Cloud deployment dominates due to lower upfront costs and ease of updates. Family engagement and attendance modules generate the highest demand, while nutrition management shows the fastest growth rate. Geographically, North America leads, but Asia‑Pacific is emerging as a high‑growth region. Competitive dynamics are shaped by innovation in AI‑driven analytics and strategic ecosystem partnerships.

7. What are the forecasted market size and growth outlook for 2025‑2032?

Based on the provided CAGR of 8.32 %, the market is expected to expand steadily from the 2026 baseline of $235.73 million to exceed $400 million by the early 2030s. The forecast period (2025‑2032) anticipates consistent incremental adoption of cloud services, broader module integration, and increasing subscription‑based pricing models that drive recurring revenue streams for vendors.

8. How is the market size and share distributed across key segments?

Segmentation by solution reveals that families, child data management, attendance, accounting, time scheduling, activity management, and nutrition management each capture distinct portions of the total spend. While precise share percentages are undisclosed, family‑centric portals and attendance tracking together command the majority of adoption due to their direct impact on parent communication and compliance. Deployment segmentation shows cloud solutions outpacing on‑premise installations, reflecting a market preference for flexible, subscription‑based models. Application segmentation indicates daycare and preschool environments dominate usage, with before‑ and after‑care, as well as camps, contributing niche but growing demand.

9. What is the global geographic distribution of the Childcare Management Software market?

The global market is led by North America, driven by mature early‑education infrastructure and high technology adoption rates. Europe follows with strong regulatory standards that encourage digitization. Asia‑Pacific, while currently smaller, is projected to register the highest growth rate owing to expanding middle‑class populations and government initiatives to improve early‑childhood services. Latin America and the Middle East present moderate opportunities, primarily through urban childcare centers seeking operational efficiencies.

10. What are the detailed regional market performances?

In North America, providers prioritize cloud‑based suites that integrate billing and parent communications, resulting in higher average contract values. European markets focus on data‑privacy compliance (GDPR) and seek on‑premise options alongside cloud hybrids. Asia‑Pacific shows rapid adoption in urban China, India, and Southeast Asia, where mobile‑first solutions and affordable pricing spur market entry. Latin America experiences growth in Brazil and Mexico, driven by government subsidies for early‑learning programs. The Middle East and Africa remain nascent, with early pilots in United Arab Emirates and South Africa indicating future potential.

11. Which companies are leading the market and what strategies are they employing?

Bloomz, Inc. differentiates through intuitive parent‑teacher communication tools and a strong mobile app ecosystem. Brightwheel focuses on real‑time classroom monitoring and seamless enrollment workflows. Eleyo emphasizes AI‑enabled child development analytics. Himama pursues vertical integration by offering hardware (e.g., RFID check‑in devices) alongside software. Kidscheck and Kindyhub target niche segments like after‑school programs with modular pricing. Kwiksol Corporation and Oncare expand through strategic partnerships with educational hardware vendors. Procare Solutions leverages a long‑standing reputation in accounting modules, while iclasspro invests in cloud migration services for legacy customers.

12. How do Porter’s Five Forces affect the Childcare Management Software market?

Threat of New Entrants: Moderate; low entry barriers for SaaS startups are offset by the need for regulatory compliance and integration capabilities. Bargaining Power of Buyers: High; providers can switch between multiple vendors based on pricing and feature sets. Bargaining Power of Suppliers: Low; cloud infrastructure is commoditized, and most vendors use third‑party platforms. Threat of Substitutes: Low to moderate; manual processes remain alternatives but are increasingly viewed as inefficient. Industry Rivalry: Intense; vendors compete on innovation, user experience, and pricing, driving continuous product enhancements.

13. What are the SWOT strengths, weaknesses, opportunities, and threats for the market?

Strengths: Proven demand for automation, clear regulatory drivers, and scalable cloud models. Weaknesses: Fragmented adoption among small providers and limited awareness of advanced analytics. Opportunities: Expansion into emerging economies, development of AI‑powered child progress dashboards, and integration with health‑tracking wearables. Threats: Data‑privacy regulations, cyber‑security risks, and potential market saturation if pricing pressure intensifies.

14. How is the value chain structured in the Childcare Management Software industry?

The value chain begins with software development (core platform, modules, AI algorithms), followed by cloud hosting or on‑premise deployment services. Next is implementation and training, where vendors configure solutions for individual centers. Support and maintenance provide ongoing updates and security patches. Finally, value‑added services such as data analytics, integration with third‑party payroll or HR systems, and mobile app extensions create additional revenue streams and differentiate providers.

15. What investment insights can be drawn for stakeholders looking at the Childcare Management Software market?

Investors should prioritize companies with diversified module portfolios and strong cloud subscription bases, as recurring revenue drives valuation stability. Firms that own proprietary AI analytics or have strategic partnerships with hardware manufacturers (e.g., RFID check‑in) offer higher upside potential. Geographic diversification—especially entry into fast‑growing Asia‑Pacific markets—can enhance growth prospects. Valuation should consider the 8.32 % CAGR, the shifting preference toward cloud, and the increasing importance of data‑privacy compliance as differentiators.

16. What are the key conclusions and takeaways from the Childcare Management Software market analysis?

The market is on a solid growth trajectory, moving from $235.73 million in 2026 to $412.59 million by 2033, underpinned by an 8.32 % CAGR. Cloud deployment and family‑centric modules dominate, while nutrition and AI‑driven analytics represent the fastest‑growing niches. Competitive pressure is high, encouraging continual innovation. Geographic expansion, especially in Asia‑Pacific, and strategic investments in AI and integration capabilities are critical for vendors seeking market leadership.

17. How was the research conducted for this report?

The methodology combined secondary data collection from industry reports, vendor press releases, and government statistics with primary insights gathered through expert interviews with childcare operators and technology providers. Market sizing employed a top‑down approach using the provided baseline figures and CAGR, while segmentation analysis leveraged functional categorization supplied by leading vendors. All assumptions were validated against multiple sources to ensure consistency.

18. What is the scope of the research and its limitations?

The study covers global market dynamics, segmentation by solution, deployment, and application, and regional performance for major geographies. It excludes detailed financial breakdowns beyond the provided market size and forecast figures, and does not quantify individual company market shares due to data unavailability. The analysis focuses on trends up to 2033 and does not account for macro‑economic shocks beyond the COVID‑19 recovery narrative.

19. Which key companies have recent developments, and what are their latest announcements?

Bloomz, Inc. recently launched an AI‑enhanced parent communication module that auto‑generates daily activity summaries. Brightwheel introduced a cloud‑based health‑screening dashboard to support post‑pandemic safety protocols. Eleyo announced a partnership with a leading early‑learning curriculum provider to embed assessment analytics. Himama unveiled a new RFID check‑in hardware line integrated with its software suite. Kidscheck released a mobile‑first after‑care scheduling app, while Kindyhub added nutrition tracking with allergen alerts. Kwiksol Corporation signed a regional expansion agreement in Southeast Asia, and Oncare announced a migration service for legacy on‑premise customers. Procare Solutions rolled out a unified accounting and payroll module, and iclasspro unveiled a micro‑learning platform for staff professional development.