What is the Vanilla Market Overview – definition, scope, and significance?

The vanilla market encompasses the production, processing, and distribution of natural vanilla products derived primarily from the orchid *Vanilla planifolia*. It covers four primary forms—paste, liquid, powder, and beans—as well as two categories, organic and conventional. Vanilla serves as a critical flavoring agent across food and beverage, personal care, and pharmaceutical applications, making it a strategic commodity for manufacturers seeking natural taste and aroma solutions.

What are the main drivers, restraints, challenges, and opportunities influencing the Vanilla Market?

Key drivers include rising consumer demand for natural ingredients, premiumization of food products, and expanding applications in personal care and pharma. Restraints stem from climate‑related supply volatility in major growing regions and price sensitivity among mass‑market buyers. Challenges involve meeting stringent quality standards and navigating complex certification processes. Opportunities arise from the growth of organic vanilla, innovative value‑added formats such as ready‑to‑use pastes, and emerging markets in Asia‑Pacific demanding exotic flavors.

Which growth trends are currently shaping the Vanilla Market?

Current trends feature a shift toward clean‑label formulations, prompting manufacturers to source certified organic vanilla. There is a noticeable increase in the use of vanilla extracts in plant‑based foods and premium desserts. Technological advancements in low‑temperature extraction are improving flavor retention, while e‑commerce platforms are expanding direct‑to‑consumer sales of specialty vanilla products.

How did COVID‑19 impact the Vanilla Market and what is the recovery trajectory?

The pandemic disrupted logistics and labor availability in key producing regions, leading to temporary shortages and price spikes. Simultaneously, home‑cooking trends boosted demand for vanilla‑flavored products. As supply chains normalize, the market is experiencing a steady recovery, with demand stabilizing and growth resuming alongside broader economic rebounds.

Who are the major competitors and what is the state of market consolidation in the Vanilla Market?

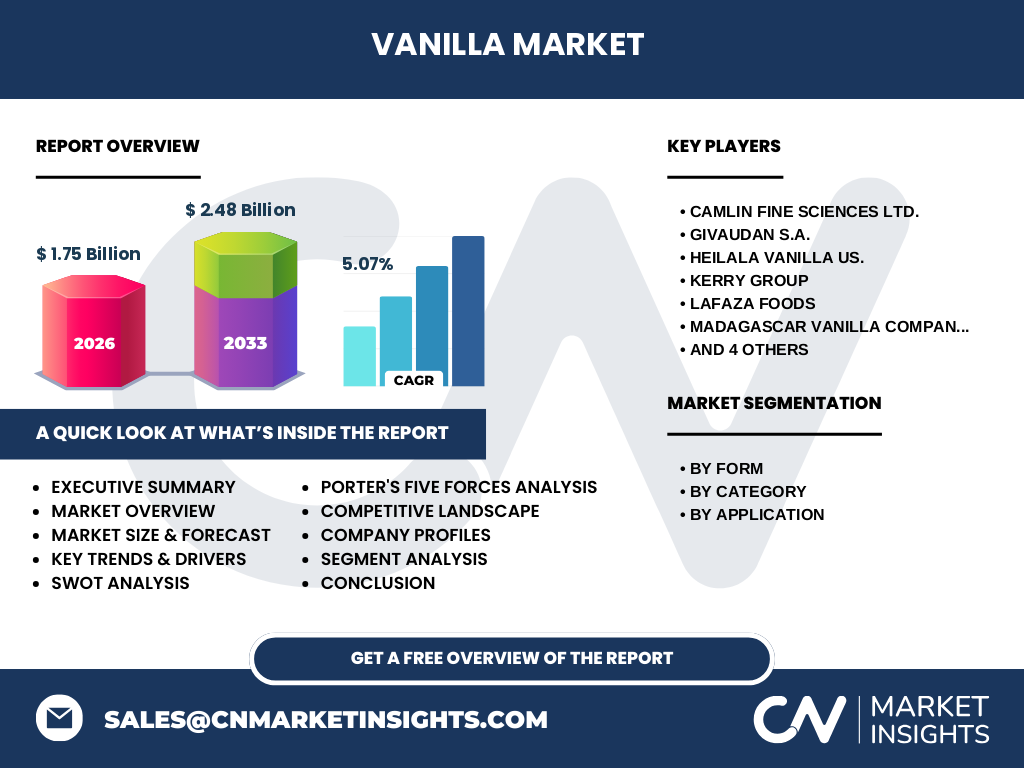

Leading players include Camlin Fine Sciences Ltd., Givaudan S.A., Heilala Vanilla US., Kerry Group, LAFAZA Foods, Madagascar Vanilla Company, Nielsen‑Massey Vanillas, Inc., Symrise, The Vanilla Company, and Touton S.A. The market demonstrates moderate consolidation, with large multinational firms focusing on vertical integration and strategic partnerships to secure raw material access, while smaller specialty producers concentrate on niche organic and single‑origin offerings.

What are the high‑level takeaways in the Executive Summary for the Vanilla Market?

The vanilla market is valued at $1.75 billion in 2026 and is projected to reach $2.48 billion by 2033, reflecting a compound annual growth rate of 5.07 %. Growth is driven by consumer preference for natural flavors, expanding applications in premium food and personal care, and increasing adoption of organic vanilla. Supply constraints remain a risk, but innovation in processing and diversification of sourcing mitigate long‑term volatility.

What are the forecasted market expectations for 2025‑2032?

Based on the projected CAGR of 5.07 %, the vanilla market is expected to continue expanding through 2025‑2032, maintaining upward momentum driven by premium product launches and broader geographic penetration. The forecast anticipates incremental yearly growth, with the market approaching the $2.48 billion mark by the end of the forecast horizon, underscoring sustained investor interest.

How is the Vanilla Market sized and shared by segmentation?

Segmentation by form reveals four distinct product lines: paste, liquid, powder, and beans, each catering to specific application needs. By category, the market is divided into organic and conventional segments, reflecting divergent consumer expectations regarding sustainability and traceability. Application segmentation identifies food and beverage, personal care, and pharmaceuticals as the primary end‑use sectors, providing a clear view of demand distribution across industries.

What is the global Vanilla Market size and share by region?

While precise regional dollar values are not disclosed, the market is globally distributed across major consuming regions, including North America, Europe, Asia‑Pacific, and Latin America. Each region contributes to the overall $1.75 billion base in 2026, with emerging economies in Asia‑Pacific showing accelerated adoption rates driven by rising disposable incomes and culinary experimentation.

What does the Regional Analysis of the Vanilla Market reveal?

North America remains a mature market, emphasizing high‑quality organic vanilla for premium food and cosmetics. Europe mirrors this trend, with stringent regulatory frameworks fostering demand for certified products. Asia‑Pacific is the fastest‑growing region, propelled by expanding foodservice sectors and increasing awareness of natural ingredients. Latin America and the Middle East present niche opportunities tied to local cuisine and specialty beverage markets.

What are the key profiles and strategies of leading companies in the Vanilla Market?

Camlin Fine Sciences Ltd. focuses on integrated value‑chain solutions, from cultivation to finished extracts. Givaudan S.A. leverages extensive R&D to create innovative flavor platforms. Heilala Vanilla US. emphasizes single‑origin, sustainably sourced beans. Kerry Group pursues strategic acquisitions to broaden its natural flavor portfolio. Other players such as Nielsen‑Massey and Symrise prioritize organic certifications and supply‑chain transparency to meet evolving customer expectations.

How does Porter’s Five Forces analysis apply to the Vanilla Market?

The threat of new entrants is moderate due to high entry barriers related to agricultural expertise and certification costs. Supplier power is relatively high because few regions dominate vanilla cultivation, creating dependence on climate‑sensitive growers. Buyer power varies; large food manufacturers wield significant influence, while niche specialty buyers seek premium pricing. The risk of substitutes is low, given vanilla’s unique flavor profile, and competitive rivalry is intense among established flavor houses and specialty producers.

What are the SWOT factors for the Vanilla Market?

Strengths include strong consumer demand for natural flavors and a diversified product portfolio across forms and applications. Weaknesses involve supply chain vulnerability and price volatility. Opportunities arise from organic expansion, novel delivery formats, and untapped regional markets. Threats consist of climate change impacts on bean yields, regulatory tightening, and potential competition from synthetic vanilla analogs.

How is the Vanilla Market’s value chain structured?

The value chain starts with cultivation of vanilla orchids, primarily in Madagascar and other tropical regions. Post‑harvest processes include curing, fermentation, and drying. Extraction and purification then produce paste, liquid, powder, and bean formats. Distribution channels range from bulk raw material sales to specialty ingredient distributors serving food, personal care, and pharmaceutical manufacturers, culminating in end‑user product integration.

What key investment insights can be drawn for the Vanilla Market?

Investors should focus on companies with vertically integrated operations that secure raw material access and possess organic certification capabilities. Growth potential lies in expanding into emerging Asian markets and developing value‑added formats such as ready‑to‑use pastes. Monitoring climate‑risk mitigation strategies and supply diversification will be essential for protecting returns.

What are the concluding takeaways from the Vanilla Market analysis?

The vanilla market demonstrates resilient growth propelled by consumer trends toward natural and premium flavors. Despite supply challenges, the projected CAGR of 5.07 % and a forecasted value of $2.48 billion by 2033 signal robust market health. Companies that invest in sustainable sourcing, product innovation, and geographic expansion are well‑positioned to capture future value.

How was the research methodology designed for this Vanilla Market report?

The study employed a mixed‑method approach, combining primary interviews with industry experts, surveys of key manufacturers, and secondary data extraction from reputable databases, trade publications, and company filings. Quantitative analysis used CAGR calculations based on the provided 2026 market size of $1.75 billion and the 2027‑2033 forecast of $2.48 billion. Qualitative insights were derived from trend observation and competitive benchmarking.

What is the scope of this research and its coverage limitations?

The research covers the global vanilla market, focusing on product forms, categories, and applications as defined in the segmentation framework. Geographic coverage includes all major consumer regions, but specific regional revenue figures are omitted due to data confidentiality. The analysis does not extend to downstream retail pricing dynamics or detailed macro‑economic impact modeling beyond the provided forecasts.

Which key companies are highlighted and what recent developments have they announced?

Key players such as Camlin Fine Sciences Ltd., Givaudan S.A., and Heilala Vanilla US. have announced new organic certification programs and expanded sourcing agreements in Madagascar and Papua New Guinea. Kerry Group reported a strategic partnership to develop vanilla‑based functional ingredients for nutraceuticals. Nielsen‑Massey launched a limited‑edition single‑origin line, while Symrise introduced a low‑temperature extraction technology aimed at preserving flavor integrity.