What is the Whole Slide Imaging Market Overview – definition, scope, and significance?

Whole slide imaging (WSI) refers to the high‑resolution digital capture of entire histopathology glass slides, enabling virtual microscopy, image analysis, and remote consultation. The market encompasses hardware (scanners, cameras), software (image management, AI‑driven analysis), and services (maintenance, cloud hosting) that support hospitals, pharmaceutical firms, laboratories, and academic research institutes. Its significance lies in accelerating diagnostic workflows, enhancing collaborative care, and unlocking data‑intensive research such as digital pathology and precision medicine.

What are the Whole Slide Imaging Market drivers, restraints, challenges, and opportunities?

Key drivers include rising demand for telepathology, increasing clinical trials requiring digital slide archives, and growing adoption of AI‑based diagnostic tools. Restraints stem from high upfront capital costs and regulatory uncertainties surrounding digital diagnostics. Challenges involve integration with legacy laboratory information systems and the need for robust data security. Opportunities arise from expanding applications in immunohistochemistry, cytopathology, and emerging markets where digital infrastructure is being built.

What are the Whole Slide Imaging Market growth trends?

Current trends feature a shift from standalone scanners to integrated hardware‑software platforms that incorporate cloud storage and real‑time analytics. Emerging trends include AI‑enhanced image interpretation, adoption of mobile‑compatible viewers, and the development of service‑oriented models (e.g., subscription‑based image processing). These trends collectively foster faster turnaround times, reduce inter‑observer variability, and create new revenue streams for vendors.

How has COVID‑19 impacted the Whole Slide Imaging Market?

The pandemic accelerated remote pathology workflows as hospitals limited in‑person access to laboratories. Demand for telepathology solutions surged, prompting rapid procurement of scanners and cloud services. Following the acute phase, the market entered a recovery trajectory where institutions continued to invest in digital infrastructure to improve resilience against future disruptions, sustaining the momentum generated during COVID‑19.

What does the Whole Slide Imaging Market competitive landscape look like?

The competitive arena is characterized by a mix of legacy optics manufacturers and specialized digital pathology firms. Major players such as Philips, Leica Biosystems, Hamamatsu, Nikon, Olympus, and 3DHISTECH dominate scanner hardware, while software specialists like Indica Labs, Visiopharm, and Akoya Biosciences lead AI‑driven analysis. Recent years have seen consolidation through strategic acquisitions and partnerships aimed at offering end‑to‑end solutions.

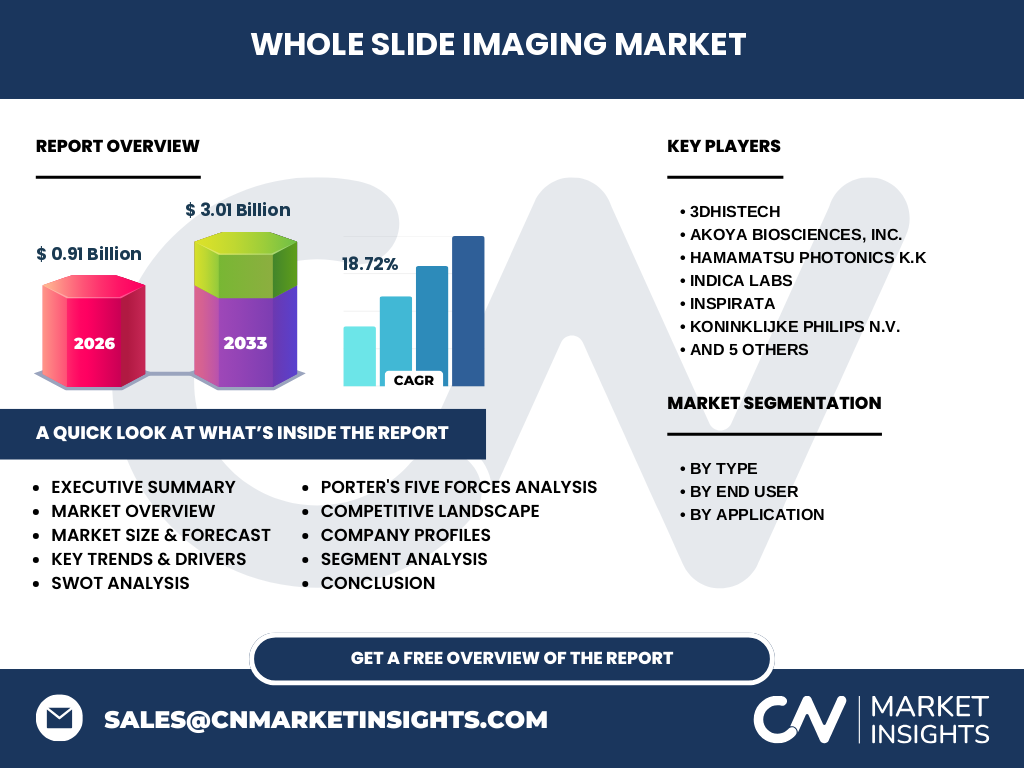

What are the key findings presented in the Executive Summary?

The market is projected to grow from a $0.91 billion valuation in 2026 to $3.01 billion by 2033, reflecting an impressive CAGR of 18.72 %. Hardware remains the largest segment, but software and services are gaining share due to AI integration. Geographic expansion, especially in Asia‑Pacific, and the rise of telepathology are primary growth engines. Competitive intensity is increasing as vendors broaden portfolios to capture end‑user demand.

What is the Whole Slide Imaging Market forecast for 2025‑2032?

Based on the provided CAGR of 18.72 %, the market is expected to maintain robust expansion throughout the forecast horizon. By 2032, the market size is anticipated to exceed $2.5 billion, driven by continual adoption in hospitals, pharmaceutical research, and academic institutions. The accelerating pace of digital transformation and regulatory acceptance of digital diagnostics will support this upward trajectory.

How is the Whole Slide Imaging Market sized and shared by segmentation?

The market is segmented by type (hardware, software, service), by end‑user (hospital, pharmaceutical and biopharmaceutical companies, laboratories, academic research institutes), and by application (telepathology, cytopathology, immunohistochemistry, hematopathology). While exact monetary shares are not disclosed, hardware traditionally commands the largest portion, with software and services capturing growing fractions as AI and cloud‑based offerings mature. Among end‑users, hospitals lead adoption, followed by pharmaceutical companies leveraging digital slides for drug development.

What is the global Whole Slide Imaging Market size and share by region?

The global market reached $0.91 billion in 2026. Although specific regional values are not enumerated, the market is broadly distributed across North America, Europe, Asia‑Pacific, and Rest of World. North America currently holds a strong position due to early technology adoption, while Asia‑Pacific is emerging as a high‑growth region driven by expanding healthcare infrastructure and governmental support for digital health initiatives.

What does the regional analysis of the Whole Slide Imaging Market reveal?

North America leads in terms of adoption speed, supported by robust research institutions and favorable reimbursement policies. Europe follows with strong academic research networks and regulatory frameworks encouraging digital pathology. Asia‑Pacific demonstrates the highest growth potential, propelled by rapid hospital modernization and increasing clinical trial activity. The Rest of World lags in adoption but presents niche opportunities where telepathology can bridge geographic gaps.

Which companies lead the Whole Slide Imaging Market and what are their strategies?

Key leaders include 3DHISTECH, Akoya Biosciences, Hamamatsu Photonics, Indica Labs, Inspirata, Philips, Leica Biosystems, Mikroscan Technologies, Nikon, Olympus, and Visiopharm. Strategies focus on portfolio diversification—combining scanners with AI analytics—strategic partnerships with cloud providers, and expanding service models. Companies are also investing in ergonomic scanner designs and interoperable software platforms to enhance user experience and broaden market reach.

How does Porter’s Five Forces analysis apply to the Whole Slide Imaging Market?

Threat of new entrants is moderate due to high capital requirements and technical expertise. Bargaining power of suppliers is low because components are sourced from multiple optical and electronic vendors. Bargaining power of buyers is increasing as hospitals and labs demand integrated solutions and cost‑effective licensing. Threat of substitutes remains low; traditional microscopy cannot match digital workflow benefits. Industry rivalry is high, driven by rapid innovation and overlapping product portfolios.

What are the SWOT analysis insights for the Whole Slide Imaging Market?

Strengths: Technological advantage, data‑driven diagnostics, and strong growth momentum. Weaknesses: High initial investment and fragmented standards. Opportunities: AI‑enabled analysis, expansion in emerging economies, and telepathology services. Threats: Regulatory delays, data privacy concerns, and potential market saturation in mature regions.

What does the Whole Slide Imaging Market value chain look like?

The value chain begins with research and development of scanner optics and image‑processing algorithms, followed by component procurement and manufacturing. Next is system integration, where hardware and software are bundled. Distribution occurs through direct sales, distributors, and OEM partnerships. Post‑sale services—maintenance, calibration, cloud storage, and analytics support—complete the chain, creating recurring revenue streams for vendors.

What key investment insights can be drawn from the Whole Slide Imaging Market?

Investors should prioritize companies that offer end‑to‑end platforms combining hardware, AI software, and service contracts, as these generate diversified cash flows. Funding opportunities exist in emerging regions where digital pathology infrastructure is nascent. Partnerships with cloud and AI firms can accelerate product development and market penetration. Monitoring regulatory approvals for AI‑based diagnostics will be critical for assessing risk.

What are the main conclusions of the Whole Slide Imaging Market report?

The Whole Slide Imaging Market is on a rapid growth trajectory, propelled by a CAGR of 18.72 % and an expected three‑fold increase in value by 2033. Hardware remains foundational, but software and services are becoming decisive growth levers. Geographic expansion, especially across Asia‑Pacific, and the rise of AI‑driven applications position the market for sustained expansion. Competitive dynamics favor firms that can deliver integrated, scalable solutions.

How was the research methodology designed for this Whole Slide Imaging Market study?

The study combined primary interviews with industry experts, technology vendors, and key end‑users, alongside secondary data from scientific publications, corporate filings, and market databases. Quantitative forecasts employed compound annual growth rate (CAGR) calculations based on the provided 2026 market size ($0.91 billion) and 2027‑2033 projection ($3.01 billion). Qualitative analysis addressed trends, competitive forces, and strategic insights.

What is the scope of the Whole Slide Imaging Market research?

The scope encompasses a global assessment of Whole Slide Imaging across hardware, software, and services, segmented by end‑user and application. It includes market size, growth forecasts (2025‑2032), competitive landscape, regional performance, and strategic analyses such as Porter’s Five Forces, SWOT, and value‑chain mapping. The research does not extend to detailed financial statements of individual companies or granular regional revenue breakdowns beyond the data provided.

Which key companies and recent developments are highlighted in the Whole Slide Imaging Market?

Prominent players include 3DHISTECH, Akoya Biosciences, Hamamatsu Photonics, Indica Labs, Inspirata, Philips, Leica Biosystems, Mikroscan Technologies, Nikon, Olympus, and Visiopharm. Recent developments feature product launches of AI‑enhanced analysis platforms, strategic partnerships with cloud service providers, and acquisitions aimed at consolidating hardware and software capabilities. Several firms announced expanded service agreements and cloud‑based image repositories to support telepathology and remote diagnostics.