What is the Mammography Systems Market Overview – Definition, scope, and significance?

The Mammography Systems Market comprises devices and related services used for early detection of breast cancer through imaging techniques. It spans analog and digital platforms, including full‑field digital mammography (FFDM) and breast tomosynthesis (3D) systems, as well as supporting technologies such as screen‑film, 2D, and 3D imaging. The market serves hospitals, ambulatory surgical centers, and diagnostic imaging centers worldwide. Early diagnosis of breast cancer significantly improves treatment outcomes and reduces mortality, making mammography a critical component of public health programs and a cornerstone of women's preventive health care.

What are the Mammography Systems Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising breast cancer awareness, government screening initiatives, and the transition from analog to digital and 3D technologies, which offer higher diagnostic accuracy. Aging populations and increasing disposable income in emerging economies further boost demand. Restraints stem from high capital costs of digital and tomosynthesis equipment and reimbursement uncertainties in some regions. Challenges involve regulatory compliance, the need for skilled radiologists, and integration with health‑IT systems. Opportunities arise from the expanding use of AI‑driven analytics, portable digital units for remote areas, and growing demand for low‑dose imaging solutions.

What are the Mammography Systems Market Growth Trends – Current and emerging trends shaping the market?

Current trends show rapid adoption of breast tomosynthesis, which now accounts for a growing share of new installations due to its superior lesion detection. Vendors are integrating AI algorithms for automated breast density assessment and cancer risk stratification. Emerging trends include the development of compact, clinic‑based digital units and the use of cloud‑based image storage to enable tele‑radiology. Sustainability considerations are prompting manufacturers to offer energy‑efficient models and recyclable components.

How has COVID‑19 impacted the Mammography Systems Market – Pandemic effects and recovery trajectory?

The COVID‑19 pandemic caused a temporary decline in screening volumes as elective procedures were postponed and patients avoided non‑essential visits. Supply‑chain disruptions delayed equipment deliveries, impacting short‑term sales. Recovery began in late 2021 as health systems reinstated screening programs and patients returned for routine exams. The market now experiences a rebound effect, with pent‑up demand driving higher installation rates for digital and tomosynthesis systems, supporting a strong post‑pandemic growth trajectory.

What does the Mammography Systems Market Competitive Landscape look like – Major competitors and market consolidation?

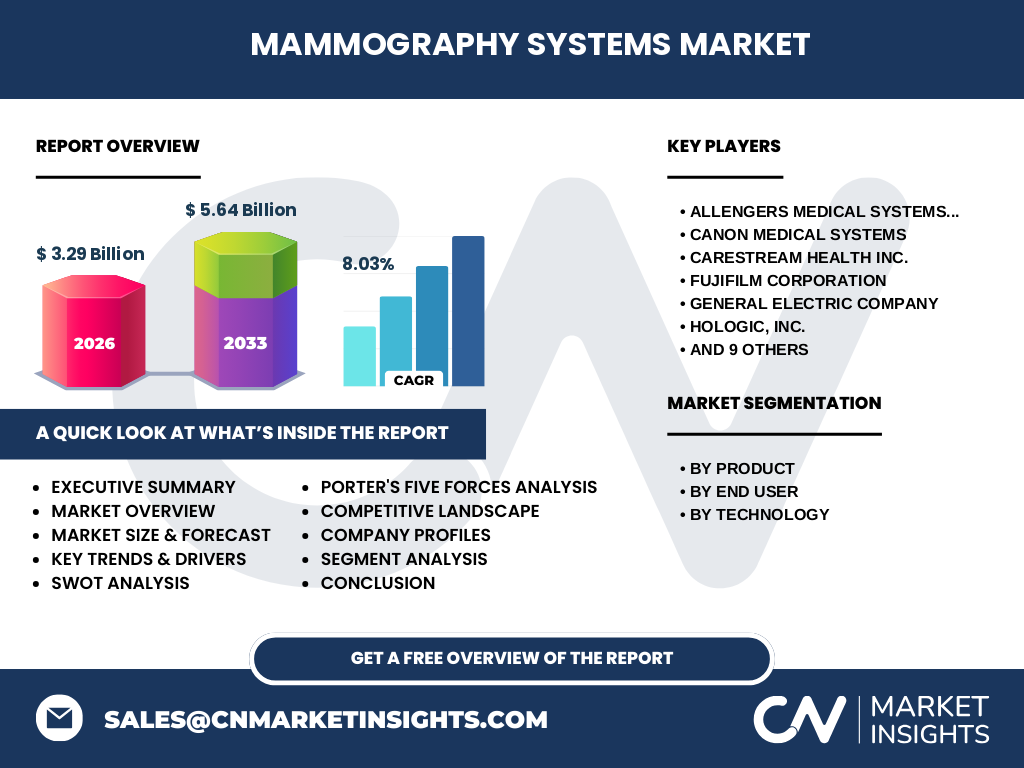

The market is moderately consolidated, led by global imaging giants and specialized manufacturers. Major players include Canon Medical Systems, Fujifilm Corporation, General Electric Company, Hologic, Inc., Konica Minolta, Koninklijke Philips N.V., Siemens Healthineers AG, and a range of niche firms such as Allengers Medical Systems Limited and PLANMED OY. Recent years have seen strategic alliances, joint ventures, and selective acquisitions aimed at expanding product portfolios, especially in AI‑enabled imaging and 3D technologies.

What are the key findings in the Executive Summary?

The Mammography Systems Market is valued at $3.29 billion in 2026 and is projected to reach $5.64 billion by 2033, growing at a CAGR of 8.03 %. Digital transformation, especially the shift to 3D tomosynthesis, is the primary growth engine. Regional demand is strongest in North America and Europe, while Asia‑Pacific shows the fastest growth potential due to expanding screening programs. Competitive dynamics are driven by technology innovation, AI integration, and value‑based pricing strategies.

What is the Mammography Systems Market Forecast – Projections for 2025‑2032 period?

Based on the provided CAGR of 8.03 %, the market is expected to expand steadily from its 2026 base of $3.29 billion to approximately $5.64 billion by 2033. This growth reflects continued migration to digital and tomosynthesis platforms, increased hospital and ambulatory center adoption, and ongoing government initiatives promoting breast cancer screening.

What is the Mammography Systems Market Size and Share by Segmentation?

By product, analog systems remain a legacy segment, while Full Field Digital Mammography (FFDM) holds the largest share due to its established clinical acceptance. Breast tomosynthesis is the fastest‑growing segment, driven by superior diagnostic performance. By end‑user, hospitals dominate installations because of higher patient volumes and reimbursement structures, whereas ambulatory surgical centers are gaining traction for convenience‑focused services. Technologically, the market is split among screen‑film, 2D, and 3D mammography, with 3D (tomosynthesis) showing the steepest growth curve.

What is the Global Mammography Systems Market Size and Share by Region – Geographic distribution?

North America and Europe together account for the majority of current market revenue, reflecting mature screening programs and high healthcare expenditures. The Asia‑Pacific region, while contributing a smaller share today, is expected to register the highest compound annual growth rate, driven by expanding middle‑class populations, rising cancer awareness, and government‑backed screening initiatives. Latin America and the Middle‑East & Africa represent emerging opportunities with growing investment in diagnostic infrastructure.

What does the Regional Analysis of the Mammography Systems Market reveal – Detailed regional market performance?

In the United States, digital and tomosynthesis replacements of aging analog fleets drive sales, supported by strong reimbursement policies. Europe shows steady demand, particularly in Germany, the UK, and France, where national screening programs mandate regular mammography. In China and India, government cancer control plans are accelerating procurement of cost‑effective digital units. Japan and South Korea exhibit high adoption of advanced 3D systems, while Brazil and Mexico are emerging markets with increasing private‑sector investment.

Who are the Leading Company Profiles in the Mammography Systems Market – Industry players and strategies?

Key players such as Hologic, Inc. focus on 3D tomosynthesis and AI‑enabled workflow solutions. Siemens Healthineers AG leverages its broad imaging portfolio to cross‑sell mammography units alongside MRI and ultrasound. Philips prioritizes integration with its health‑IT platform for seamless data exchange. Canon and Fujifilm emphasize high‑resolution digital detectors and low‑dose technologies. Smaller firms like Allengers Medical Systems Limited and PLANMED OY differentiate through cost‑competitive analog and hybrid digital offerings for price‑sensitive markets.

What are the results of the Porter’s Five Forces Analysis of the Mammography Systems Market?

Threat of new entrants: Moderate – high capital requirements and regulatory barriers limit newcomers. Bargaining power of suppliers: Low to moderate – component suppliers are diversified, though specialized detector manufacturers hold some leverage. Bargaining power of buyers: High – hospitals and health systems negotiate pricing, especially for bulk purchases. Threat of substitutes: Low – alternative imaging modalities cannot replace mammography for primary breast cancer screening. Rivalry among existing competitors: Strong – firms compete on technology innovation, price, service contracts, and AI capabilities.

What does the SWOT Analysis of the Mammography Systems Market show?

Strengths: Proven clinical efficacy, strong regulatory support, and growing demand for early detection. Weaknesses: High upfront cost, dependence on reimbursement policies, and need for skilled operators. Opportunities: Expansion into emerging markets, AI‑driven diagnostic tools, and low‑dose 3D technologies. Threats: Economic downturns affecting capital spending, potential regulatory changes, and competition from alternative screening methods.

What is the Mammography Systems Market Value Chain Analysis?

The value chain begins with raw material suppliers (e.g., detector crystals, electronics), proceeds to component manufacturers (detector panels, X‑ray tubes), then to system integrators that assemble analog, digital, and tomosynthesis units. Afterward, distributors and service providers deliver equipment to hospitals and ambulatory centers, offering installation, training, and maintenance. Finally, end‑users generate imaging data that feed into health‑IT systems, creating feedback loops for product improvement and AI algorithm training.

What are the Key Investment Insights in the Mammography Systems Market?

Investors should target companies with robust digital and 3D pipelines, as these segments command higher growth rates. Partnerships with AI and health‑IT firms enhance product differentiation and recurring revenue streams. Geographic diversification—particularly into Asia‑Pacific—offers upside potential. Monitoring regulatory developments around low‑dose imaging and AI‑assisted diagnostics can uncover early‑stage investment opportunities.

What is the Mammography Systems Market Conclusion – Summary and key takeaways?

The Mammography Systems Market is on an upward trajectory, driven by technology upgrades, heightened cancer awareness, and favorable policy environments. With a projected CAGR of 8.03 % and a market size reaching $5.64 billion by 2033, digital and tomosynthesis solutions dominate growth. Competitive advantage will hinge on AI integration, cost‑effective product lines, and strategic geographic expansion.

What Research Methodology was used for this study?

The research employed a mixed‑method approach, combining primary interviews with industry executives, surveys of radiology departments, and secondary data analysis from company reports, regulatory filings, and reputable industry databases. Market sizing used a top‑down analysis anchored on the provided 2026 market value of $3.29 billion and applied the disclosed CAGR of 8.03 % for forward projections.

What is the Research Scope – Coverage and limitations?

The scope covers global mammography equipment, focusing on product types (analog, FFDM, tomosynthesis), end‑users (hospitals, ambulatory surgical centers), and underlying technologies (screen‑film, 2D, 3D). It excludes consumables, ancillary services, and non‑imaging breast health products. Geographic coverage includes all major regions, though granular country‑level financial data were not disclosed.

Who are the Key Companies and Recent Developments in the Mammography Systems Market?

Leading firms such as Hologic, Siemens Healthineers, Philips, Canon, and Fujifilm have announced new 3D tomosynthesis platforms with integrated AI for automated lesion detection. GE Healthcare introduced a low‑dose digital detector aimed at reducing patient radiation exposure. Smaller players like Allengers Medical Systems Limited launched affordable hybrid digital‑analog units targeting emerging markets. Collaborative agreements between AI startups and established manufacturers are accelerating the rollout of decision‑support tools across the product portfolio.