What is the Tortilla Market Overview – definition, scope, and significance?

The tortilla market encompasses the production, distribution, and consumption of flatbreads primarily made from wheat or corn, as well as derived products such as tortilla chips, taco shells, and wraps. Its scope covers both traditional foodservice channels (restaurants, cafeterias) and retail channels (supermarkets, convenience stores, online platforms). Tortillas are a staple in many cuisines, particularly in North, Central, and South American diets, and their growing popularity in health‑focused and convenience‑driven meals underscores their strategic importance in the global packaged foods sector. The market’s significance is reflected in a 2026 valuation of $35.92 billion, indicating robust consumer demand and a strong platform for product innovation.

What are the Tortilla Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising demand for convenient, ready‑to‑eat meals, the expansion of Mexican‑inspired cuisine worldwide, and increasing consumer interest in gluten‑free and high‑protein alternatives. The organic segment is gaining traction as health‑conscious shoppers seek cleaner labels. Restraints stem from price sensitivity in emerging markets and fluctuating raw‑material costs for wheat and corn. Challenges involve supply‑chain disruptions, especially for corn, and the need to meet diverse regulatory standards across regions. Opportunities arise from product diversification (e.g., fortified wraps), digital sales channels, and the ability to capture premium pricing through organic and clean‑label positioning.

What are the current Tortilla Market Growth Trends?

Growth trends are defined by a shift toward premiumization, with consumers favoring organic and non‑GMO varieties. The snack‑segment—particularly tortilla chips and tostada chips—continues to outpace traditional wraps due to snacking culture and innovative flavors. Plant‑based ingredient blends are emerging, offering higher fiber and protein content. Additionally, e‑commerce penetration is accelerating, as online retail becomes a key distribution channel for both bulk and single‑serve packaging.

How has COVID‑19 impacted the Tortilla Market and what is the recovery trajectory?

The pandemic initially disrupted supply chains for corn and wheat, but also spurred home cooking and stock‑piling of pantry staples, boosting tortilla sales in retail outlets. With lockdowns easing, the market transitioned from a retail‑centric surge to a balanced mix of foodservice revival and continued online growth. The recovery trajectory is positive, with demand stabilizing and expanding as consumers maintain the convenience habits formed during the pandemic.

Who are the main competitors in the Tortilla Market and how is the competitive landscape evolving?

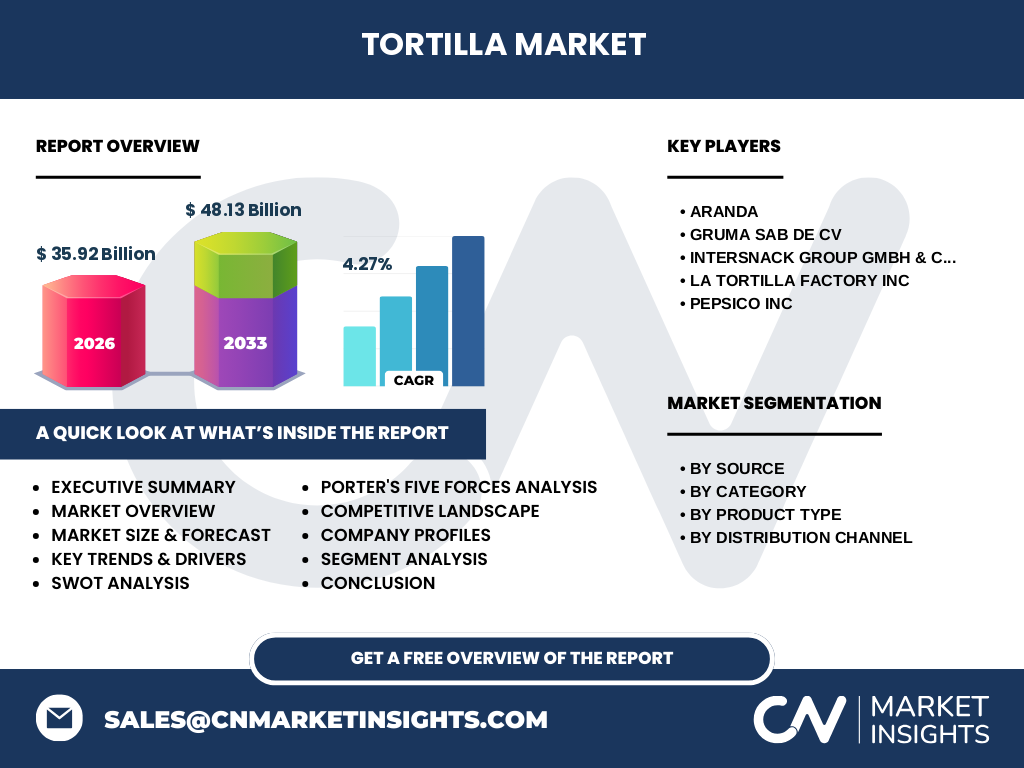

Major players include Aranda, GRUMA SAB de CV, Intersnack Group GmbH & Co KG, La Tortilla Factory Inc, and PepsiCo Inc. These firms compete across multiple segments—source (wheat vs. corn), category (organic vs. conventional), and product type. Consolidation is modest but noticeable, as larger companies acquire niche organic brands to broaden portfolios. Strategic alliances with retail giants and investment in automation are common tactics to improve cost efficiency and expand distribution reach.

What are the key findings in the Executive Summary of the Tortilla Market?

The tortilla market is valued at $35.92 billion in 2026 and is projected to reach $48.13 billion by 2033, reflecting a CAGR of 4.27%. Growth is driven by expanding snack consumption, premium organic offerings, and digital sales channels. While raw‑material price volatility presents a risk, companies are mitigating this through vertical integration and diversified sourcing. The market remains fragmented with several global leaders, yet opportunities for new entrants exist in niche categories such as gluten‑free and functional tortillas.

What are the Tortilla Market Forecasts for 2025‑2032?

Based on the provided CAGR of 4.27%, the market is expected to steadily climb from its 2026 base of $35.92 billion to approximately $48.13 billion by the end of 2033. This trajectory suggests that by 2025 the market will be just under $36 billion, with incremental growth each subsequent year. The forecast underscores a consistent demand environment, supported by expanding snack lines and ongoing health‑driven product innovation.

How is the Tortilla Market Size and Share distributed by segmentation?

Segmentation by source splits the market between wheat and corn tortillas, each serving distinct culinary uses and consumer preferences. By category, organic tortillas command a growing premium niche, while conventional products retain the majority share due to price competitiveness. Product‑type segmentation highlights tortilla chips/tostada chips as the largest share, followed by taco shells and tortilla wraps. Distribution channels are led by supermarkets and hypermarkets, with convenience stores and online retail gaining momentum, especially for single‑serve formats.

What is the Global Tortilla Market Size and Share by Region?

The market exhibits a broad geographic footprint, with North America holding the largest share due to entrenched Mexican cuisine and strong retail infrastructure. Latin America follows closely, reflecting traditional consumption patterns and rapid urbanization. Europe and Asia‑Pacific are emerging regions where tortilla‑based products are introduced through fusion concepts and snack diversification. The regional split aligns with the global valuation of $35.92 billion in 2026.

What does the Regional Analysis of the Tortilla Market reveal?

In North America, growth is propelled by premium organic offerings and high‑volume snack sales. Latin America benefits from cultural affinity and expanding modern retail, though price sensitivity remains a factor. Europe shows steady adoption driven by health‑focused consumers and the rise of Mediterranean‑style wraps. The Asia‑Pacific market, while still nascent, presents upside potential as international food trends introduce tortillas to new consumer bases, supported by online retail growth.

Which companies lead the Tortilla Market and what are their strategic approaches?

GRUMA SAB de CV leverages its extensive corn supply chain to dominate the corn tortilla segment and invests heavily in sustainable farming practices. Aranda focuses on wheat‑based products and has expanded its snack portfolio through acquisitions. Intersnack Group emphasizes branded tortilla chips, utilizing strong marketing campaigns. La Tortilla Factory Inc differentiates via organic and gluten‑free product lines, targeting health‑conscious shoppers. PepsiCo Inc integrates tortilla snacks into its broader Frito‑Lay portfolio, benefiting from cross‑category synergies and global distribution networks.

How does Porter’s Five Forces analysis apply to the Tortilla Market?

Threat of new entrants is moderate; brand loyalty and economies of scale pose barriers, yet niche organic entrants can gain footholds. Bargaining power of suppliers is moderate to high, especially for corn, where weather‑related volatility can affect pricing. Bargaining power of buyers is significant in retail, as large chains demand volume discounts and shelf‑space concessions. Threat of substitutes includes alternative snack bases (pita, rice cakes), but tortillas retain a unique texture and flavor profile. Industry rivalry is intense, driven by product innovation, marketing spend, and price competition among the leading firms.

What are the SWOT elements of the Tortilla Market?

Strengths: Established consumer base, versatile product applications, and strong growth in snack formats.

Weaknesses: Dependence on commodity raw materials and limited differentiation in conventional segments.

Opportunities: Expansion of organic, gluten‑free, and functional tortillas; digital sales acceleration; geographic diversification.

Threats: Raw‑material price spikes, supply‑chain disruptions, and competitive pressure from alternative snack categories.

What does the Tortilla Market Value Chain look like?

The value chain begins with agricultural sourcing of wheat and corn, followed by milling, dough preparation, and forming. Production stages include baking or frying (for chips), seasoning, and packaging. Distribution flows through bulk shipments to distributors, then to supermarkets, hypermarkets, convenience stores, and increasingly, direct‑to‑consumer online platforms. Ancillary services such as quality assurance, branding, and logistics optimization add value throughout the chain.

What key investment insights can be drawn for the Tortilla Market?

Investors should target companies with strong vertical integration and diversified product portfolios, as these mitigate raw‑material risk and capture premium pricing. Brands that have successfully entered the organic and functional segments are positioned for higher margin growth. Additionally, firms expanding their e‑commerce capabilities are likely to benefit from continued channel shift. Strategic partnerships with retail giants and investment in sustainable sourcing can enhance long‑term profitability.

What conclusions can be drawn from the Tortilla Market analysis?

The tortilla market is on a clear growth path, underpinned by a solid CAGR of 4.27% and a projected market size of $48.13 billion by 2033. Consumer trends toward convenience, health, and snacking drive product innovation, while supply‑chain resilience and organic differentiation provide competitive advantages. Companies that adapt to digital channels and expand premium offerings will likely capture the greatest share of future value.

How was the research methodology designed for this Tortilla Market report?

The study employed a mixed‑method approach, combining primary interviews with industry executives, surveys of retail and foodservice buyers, and secondary data analysis from company filings, trade associations, and market databases. Trend extrapolation used the disclosed CAGR of 4.27% to model forward projections. Segmentation analysis leveraged the defined categories (source, category, product type, channel) to ensure comprehensive coverage.

What is the scope of the research and its limitations?

The scope covers global market sizing, segmentation, regional performance, competitive profiling, and strategic analysis for the period 2025‑2033. Data is confined to the figures provided (2026 market size, forecast, CAGR, and segment definitions). While the report offers qualitative insights, it does not include granular country‑level revenue breakdowns or proprietary financial ratios beyond the stated numbers.

Which key companies and recent developments are shaping the Tortilla Market?

GRUMA SAB de CV announced the launch of a sustainable corn‑sourcing program aimed at reducing carbon footprint. Aranda recent acquisition of a boutique organic tortilla brand expands its premium portfolio. Intersnack Group introduced a new line of low‑sodium tortilla chips targeting health‑conscious snackers. La Tortilla Factory Inc unveiled gluten‑free tortilla wraps in partnership with a major supermarket chain. PepsiCo Inc integrated its new tortilla chip flavor into globally recognized snack assortments, leveraging its extensive distribution network.