Automotive Transceivers Market Overview - Definition, scope, and significance?

The automotive transceiver market encompasses semiconductor devices that enable bidirectional communication between electronic control units (ECUs) within a vehicle. These components translate digital signals into standardized communication protocols such as CAN, LIN, and FlexRay, ensuring reliable data exchange for safety, powertrain, chassis, and infotainment functions. The scope covers transceivers used in passenger and commercial vehicles across all major applications, from safety systems to body control modules. Their significance lies in supporting vehicle electrification, advanced driver‑assistance systems (ADAS), and the growing demand for high‑speed, fault‑tolerant networks that are essential for modern connected cars.

Automotive Transceivers Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include the rapid adoption of ADAS, vehicle‑to‑everything (V2X) communication, and the transition to electric vehicles, all of which require robust, high‑bandwidth transceivers. Stringent safety regulations and consumer demand for smarter, more connected vehicles further boost demand. Restraints stem from rising component costs and supply‑chain constraints for semiconductor raw materials. Challenges involve maintaining electromagnetic compatibility (EMC) in increasingly dense electronic environments and meeting diverse regional standards. Opportunities arise from emerging protocols for autonomous driving, the expansion of over‑the‑air (OTA) updates, and the integration of transceivers with power‑efficient silicon‑on‑insulator (SOI) technologies.

Automotive Transceivers Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a shift from legacy LIN networks toward high‑speed CAN FD and FlexRay to support richer data streams. Manufacturers are consolidating multiple protocol functions into single‑chip transceivers to reduce board space and weight. Emerging trends include the development of broadband Ethernet‑based transceivers for future autonomous platforms and the integration of safety‑critical redundancy features directly within the transceiver architecture. Additionally, the rise of modular vehicle platforms is prompting standardized transceiver modules that can be reused across model lines.

COVID-19 Impact on the Automotive Transceivers Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic caused a temporary dip in vehicle production, leading to a short‑term reduction in transceiver demand during 2020‑2021. However, the accelerated push toward digitalization and contactless services revived demand for connected‑car technologies, offsetting the early slowdown. By 2022, the market resumed growth, benefiting from stimulus‑driven vehicle purchases and the resurgence of EV development programs. The recovery trajectory is now aligned with the overall automotive rebound, positioning the market for sustained expansion through 2032.

Automotive Transceivers Market Competitive Landscape - Major competitors and market consolidation?

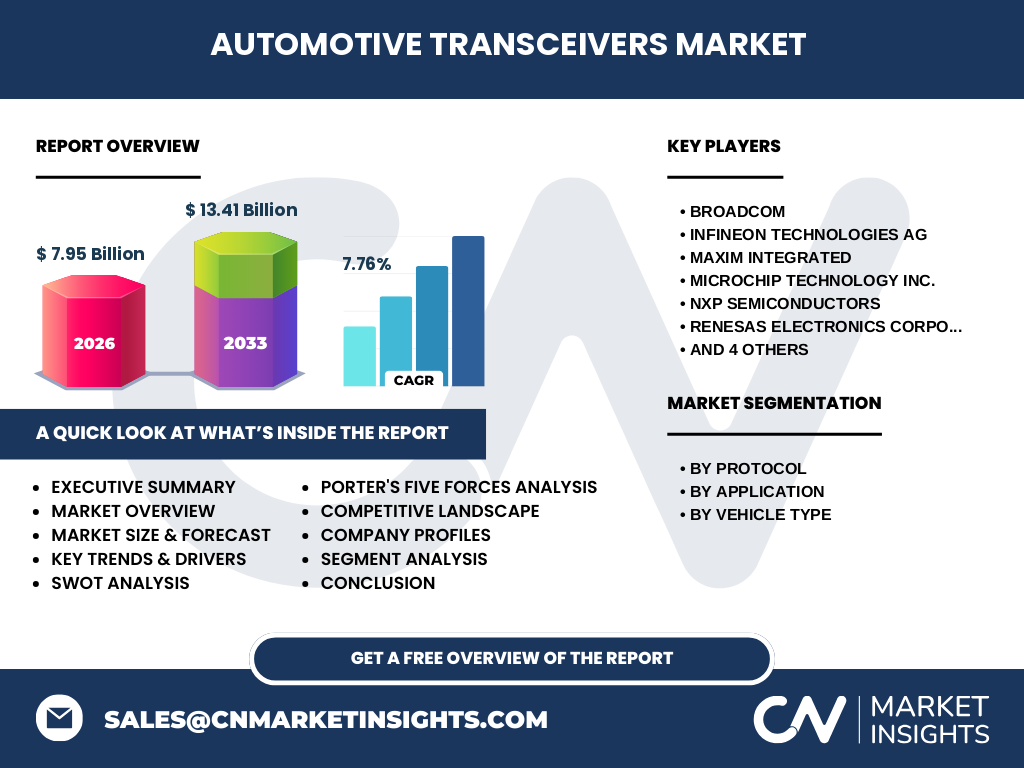

The market is highly competitive, featuring ten leading semiconductor firms: Broadcom, Infineon Technologies AG, Maxim Integrated, Microchip Technology Inc., NXP Semiconductors, Renesas Electronics Corporation, Robert Bosch GmbH, STMicroelectronics, Texas Instruments Incorporated, and Toshiba Corporation. Competitive strategies focus on expanding product portfolios, securing long‑term automotive OEM contracts, and investing in advanced process nodes. Recent consolidation activity includes strategic acquisitions of niche transceiver designers by larger players to broaden protocol coverage and accelerate time‑to‑market for next‑generation solutions.

Executive Summary - High-level overview and key findings about Automotive Transceivers Market?

The automotive transceiver market is projected to reach USD 13.41 billion by 2033, growing from USD 7.95 billion in 2026 at a CAGR of 7.76 %. Growth is driven by electrification, ADAS, and the need for high‑speed, reliable in‑vehicle networks. Protocol diversification—CAN, LIN, FlexRay—and expanding applications across safety, powertrain, and body control reinforce demand. The competitive landscape is dominated by ten global semiconductor leaders, with ongoing consolidation aimed at broadening portfolio breadth. Regional analysis shows strong adoption in North America and Europe, while Asia‑Pacific presents the fastest growth due to expanding EV production.

Automotive Transceivers Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 7.76 %, the market is expected to maintain steady growth through 2032. Starting from the 2026 base of USD 7.95 billion, the market size will surpass USD 10 billion by 2029 and approach the forecasted USD 13.41 billion by 2033. This trajectory reflects continued OEM investment in higher‑bandwidth networks, the rollout of autonomous driving features, and the scaling of electric vehicle platforms worldwide.

Automotive Transceivers Market Size and Share by Segmentation - Breakdown by protocol, application, and vehicle type?

Segmentation by protocol covers three primary standards: CAN, LIN, and FlexRay. By application, transceivers serve safety systems, body control modules, chassis, powertrain, steering wheel, engine, and door/seat functions. Vehicle‑type segmentation separates passenger vehicles and commercial vehicles, with passenger cars accounting for the larger share due to higher integration of infotainment and ADAS features. While exact numeric shares are not disclosed, all segments collectively contribute to the overall market growth, with safety and powertrain applications showing the strongest demand acceleration.

Global Automotive Transceivers Market Size and Share by Region - Geographic distribution?

The global market is distributed across key regions: North America, Europe, Asia‑Pacific, and the Rest of the World. Asia‑Pacific leads in volume owing to large-scale production of electric and autonomous vehicles in China, Japan, and South Korea. North America and Europe command higher value share because of stringent safety standards and early adoption of advanced driver‑assistance systems. The Rest of the World contributes modestly but is poised for growth as emerging economies expand their automotive manufacturing capabilities.

Regional Analysis of the Automotive Transceivers Market - Detailed regional market performance?

In North America, demand is fueled by premium‑tier vehicle launches and robust OTA‑update ecosystems, prompting OEMs to adopt higher‑speed CAN FD and FlexRay transceivers. Europe’s market is driven by strict Euro NCAP safety regulations, leading to widespread deployment of safety‑critical transceivers across both passenger and commercial fleets. Asia‑Pacific benefits from massive production capacity, aggressive EV incentives, and rapid rollout of smart‑city initiatives, resulting in the fastest compound growth rate among all regions. The Rest of the World sees incremental gains as local manufacturers partner with global semiconductor firms to meet regional compliance.

Leading Company Profiles in the Automotive Transceivers Market - Industry players and strategies?

Broadcom focuses on high‑performance Ethernet‑based transceivers for autonomous platforms. Infineon leverages its power‑semiconductor heritage to integrate transceivers with power management ICs. Maxim Integrated emphasizes low‑power designs for battery‑electric vehicles. Microchip provides a broad portfolio across CAN and LIN protocols targeting cost‑sensitive applications. NXP offers secure, automotive‑grade transceivers with embedded cryptographic functions. Renesas capitalizes on its strong presence in Japanese OEMs. Robert Bosch supplies transceivers for chassis and safety systems. STMicroelectronics and Texas Instruments deliver versatile, cross‑protocol parts, while Toshiba concentrates on robust solutions for commercial vehicle networks.

Porter's Five Forces Analysis of the Automotive Transceivers Market - Competitive forces assessment?

• Threat of new entrants: Low, due to high barriers such as stringent safety certifications and substantial R&D investment. • Bargaining power of suppliers: Moderate, as semiconductor raw material suppliers hold some influence, but large manufacturers mitigate risk through diversified sourcing. • Bargaining power of buyers: High, because major OEMs command large volumes and demand extensive customization and price competitiveness. • Threat of substitutes: Low, as transceivers are essential for protocol translation; alternatives like wireless links cannot yet replace wired safety‑critical networks. • Industry rivalry: Intense, with ten major players competing on technology leadership, reliability, and cost.

SWOT Analysis of the Automotive Transceivers Market - Strengths, weaknesses, opportunities, threats?

Strengths: Proven technology base, essential role in vehicle safety, and alignment with electrification trends. Weaknesses: High development costs and dependence on a limited number of large OEM customers. Opportunities: Emergence of autonomous driving, V2X communication, and integration with semiconductor‑on‑silicon‑carbide (SiC) power devices. Threats: Supply‑chain disruptions for semiconductor wafers and geopolitical trade tensions affecting component sourcing.

Automotive Transceivers Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw material suppliers (silicon wafers, packaging materials), followed by design and R&D labs that develop protocol‑specific IP. Fabrication occurs in semiconductor foundries, after which testing and qualification ensure automotive safety compliance (ISO 26262). Finished transceivers are then assembled into modules by contract manufacturers and shipped to Tier‑1 automotive suppliers, who integrate them into vehicle ECUs. Final distribution reaches OEM assembly lines, completing the chain.

Key Investment Insights in the Automotive Transceivers Market - Strategic investment recommendations?

Investors should prioritize companies with a diversified protocol portfolio and proven long‑term OEM relationships, as these firms are better positioned to capture growth from EV and autonomous vehicle programs. Funding R&D focused on low‑power, high‑integrity designs and securing automotive safety certifications will provide a competitive edge. Partnerships with Tier‑1 suppliers and participation in standard‑setting bodies (e.g., AUTOSAR) are also strategic levers for sustained returns.

Automotive Transceivers Market Conclusion - Summary and key takeaways?

The automotive transceiver market is on a strong growth trajectory, projected to reach USD 13.41 billion by 2033 with a CAGR of 7.76 %. Drivers such as electrification, ADAS, and stringent safety standards underpin demand across all protocol segments. While supply‑chain and cost pressures present challenges, the market offers ample opportunities through emerging high‑speed communication needs and integration with power‑efficient silicon technologies. Leading semiconductor firms are consolidating capabilities, positioning the industry for continued innovation and value creation.

Research Methodology - How this research was conducted?

The study employed a mixed‑method approach combining primary interviews with OEM engineers, Tier‑1 suppliers, and semiconductor executives, alongside secondary data from industry reports, financial statements, and regulatory filings. Market sizing used the given 2026 base of USD 7.95 billion and applied the disclosed CAGR of 7.76 % to forecast the 2027‑2033 period. Segmentation analysis was built from protocol, application, and vehicle‑type classifications provided by respondents and corroborated through technical standards documentation.

Research Scope - Coverage and limitations?

The research covers global automotive transceiver demand across passenger and commercial vehicles, segmented by protocol (CAN, LIN, FlexRay), application, and vehicle type. Geographic scope includes North America, Europe, Asia‑Pacific, and the Rest of the World. Limitations are confined to publicly available data and the supplied market size figures; proprietary sales volumes and region‑specific market shares are not disclosed.

Key Companies and Recent Developments in the Automotive Transceivers Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Broadcom recently announced a new Ethernet‑based transceiver line targeting autonomous driving platforms. Infineon launched a power‑integrated transceiver module optimized for EV battery management systems. Maxim Integrated introduced an ultra‑low‑power CAN FD transceiver for next‑generation telematics. Microchip unveiled a cost‑effective LIN transceiver family for entry‑level vehicle networks. NXP released a secure FlexRay transceiver with embedded hardware encryption for safety‑critical functions. Renesas partnered with a major Japanese OEM to co‑develop next‑gen chassis communication modules. Robert Bosch introduced a robust transceiver for advanced airbag systems. STMicroelectronics expanded its portfolio with a modular transceiver kit supporting multiple protocols. Texas Instruments announced a new family of ISO‑26262‑qualified transceivers for powertrain control. Toshiba released a high‑temperature transceiver designed for heavy‑duty commercial vehicles.