What is the EV Transmission Market Overview – definition, scope, and significance?

The EV Transmission Market encompasses the design, manufacturing, and supply of power‑train transmission systems specifically engineered for electric vehicles (EVs). Unlike conventional internal‑combustion engines, EVs use electric motors that require either single‑speed or multi‑speed gearsets to optimize torque delivery, efficiency, and driving dynamics. The market scope covers all drivetrain components, including gearboxes, couplings, and associated control electronics, for both Battery Electric Vehicles (BEV) and Hybrid Electric Vehicles (HEV). Its significance stems from the rapid electrification of the automotive sector, regulatory pressure for lower emissions, and the need for higher performance and range, making transmissions a pivotal element in overall vehicle efficiency and customer acceptance.

What are the main drivers, restraints, challenges, and opportunities shaping the EV Transmission Market?

Key drivers include the global shift toward zero‑emission mobility, supportive government incentives, and the growing demand for higher‑performance EVs that benefit from multi‑speed gearboxes. Technological advances such as lightweight materials and advanced control algorithms further stimulate growth. Restraints involve the higher cost of multi‑speed systems compared with single‑speed units and the added complexity of integration with vehicle electronics. Challenges relate to the need for robust thermal management, stringent reliability standards, and supply‑chain constraints for specialty alloys. Opportunities arise from emerging markets adopting EVs faster than mature regions, the potential for modular transmission platforms across vehicle segments, and the development of integrated power‑train solutions that combine transmission and motor functions.

Which growth trends are currently influencing the EV Transmission Market?

Current trends include a gradual shift from single‑speed to multi‑speed transmissions in high‑performance BEVs to improve acceleration and extend driving range at higher speeds. Another trend is the convergence of transmission and power electronics, enabling more compact and efficient drivetrain packages. OEMs are also exploring standardised transmission architectures to reduce development costs across multiple models. Finally, sustainability considerations are prompting the use of recyclable materials and eco‑friendly manufacturing processes, aligning with broader ESG goals.

How did COVID‑19 affect the EV Transmission Market and what is the recovery trajectory?

The pandemic disrupted supply chains for critical components such as gears and electronic control units, leading to temporary production slowdowns. However, stimulus measures and heightened consumer interest in clean mobility accelerated EV adoption post‑2020. Recovery has been strong, with production volumes rebounding as factories reopened and demand for new EV models surged, positioning the transmission segment for accelerated growth in the medium term.

What does the competitive landscape of the EV Transmission Market look like?

The market is dominated by established automotive suppliers and specialist drivetrain manufacturers. Major players such as ZF Friedrichshafen AG, Continental AG, and BorgWarner Inc. command significant design expertise and global manufacturing footprints. Recent consolidation activity includes strategic acquisitions and joint ventures aimed at expanding capabilities in multi‑speed gearsets and integrated power‑train modules. Competitive differentiation is driven by technology leadership, cost efficiency, and the ability to deliver turnkey solutions to OEMs.

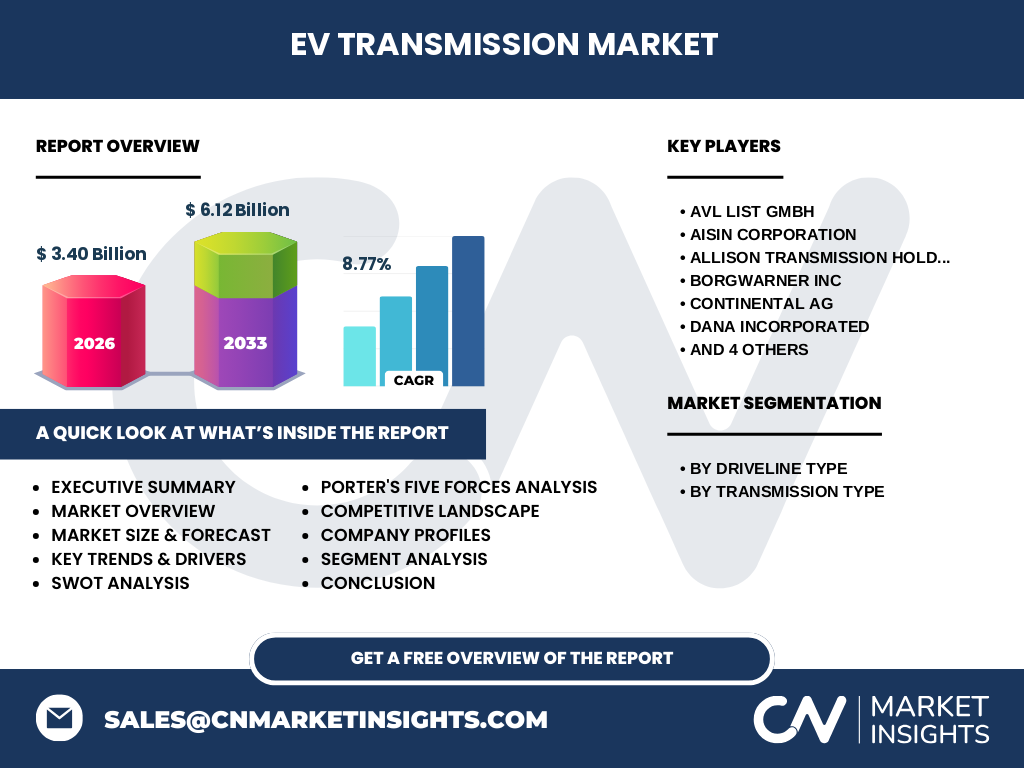

Can you provide an executive summary of the key findings about the EV Transmission Market?

The EV Transmission Market is projected to expand from a 2026 value of $3.40 billion to $6.12 billion by 2033, reflecting a robust CAGR of 8.77 %. Growth is propelled by the shift toward electrified mobility, the emergence of multi‑speed transmissions for performance‑oriented BEVs, and increasing demand in hybrid vehicles. While cost and integration complexity remain hurdles, opportunities abound in modular designs, emerging market uptake, and the convergence of transmission and power electronics. Leading suppliers are consolidating to broaden their technology portfolios, positioning the market for sustained expansion.

What are the forecast expectations for the EV Transmission Market from 2025 to 2032?

Based on the provided CAGR of 8.77 %, the market is expected to maintain steady growth throughout the forecast horizon. By 2032, the market size is anticipated to approach the upper end of the projected $6.12 billion figure for 2033, indicating a continuously expanding demand for both single‑speed and multi‑speed transmission solutions across BEV and HEV platforms.

How is the EV Transmission Market sized and shared by segment?

The market is segmented by driveline type into Battery Electric Vehicles and Hybrid Electric Vehicles, and by transmission type into Single Speed and Multi‑Speed. While exact monetary shares are not disclosed, the BEV segment is expected to dominate due to higher unit sales of pure‑electric models, whereas the HEV segment sustains demand for specialized multi‑speed gearsets that balance electric and combustion power. Single‑speed transmissions currently hold a larger share because of their simplicity and lower cost, but the multi‑speed segment is gaining traction in performance‑focused vehicles.

What is the geographic distribution of the global EV Transmission Market?

The market exhibits a worldwide footprint, with major activity in North America, Europe, and Asia‑Pacific. These regions host the largest OEM bases and have aggressive EV adoption policies, driving demand for advanced transmission technologies. Emerging economies in Latin America and the Middle East are beginning to contribute to market growth as local manufacturers launch new EV models.

What are the key regional performance insights for the EV Transmission Market?

In North America, strong regulatory support and high consumer purchasing power stimulate rapid deployment of BEVs, fostering demand for both single‑speed and emerging multi‑speed solutions. Europe’s stringent CO₂ targets accelerate the rollout of HEVs and BEVs, prompting OEMs to adopt advanced transmission architectures. Asia‑Pacific leads in production volume, with China’s aggressive EV rollout and Japan’s hybrid expertise driving diversified transmission needs. Regional investments in R&D centers further enhance local capabilities.

Which companies lead the EV Transmission market and what are their strategic approaches?

The leading companies include AVL List GmbH, Aisin Corporation, Allison Transmission Holdings Inc., BorgWarner Inc., Continental AG, Dana Incorporated, Eaton Corporation plc, Porsche AG, Schaeffler Technologies AG & Co. KG, and ZF Friedrichshafen AG. Their strategies focus on expanding multi‑speed product portfolios, investing in digital control systems, forming alliances with EV manufacturers, and leveraging proprietary materials to reduce weight and improve efficiency. Many are also pursuing joint development projects to integrate transmission functions directly with electric motors.

How does Porter’s Five Forces analysis apply to the EV Transmission Market?

• Threat of new entrants is moderate; high capital requirements and technical expertise create barriers, yet emerging startups with innovative designs could challenge incumbents.

• Bargaining power of suppliers is moderate, as specialized gear and electronic components have limited sources, but large manufacturers can negotiate volume discounts.

• Bargaining power of buyers (OEMs) is high because they demand cost‑effective, high‑performance solutions and can switch suppliers if criteria are not met.

• Threat of substitutes is low; alternative drivetrain concepts such as direct‑drive or in‑wheel motors still rely on some form of transmission technology.

• Industry rivalry is intense, with numerous established players competing on technology, price, and delivery reliability.

What are the SWOT factors influencing the EV Transmission Market?

Strengths: Established technical expertise, growing demand from EVs, and strong OEM relationships.

Weaknesses: High development costs for multi‑speed systems and dependence on complex supply chains.

Opportunities: Expansion into emerging markets, modular transmission platforms, and integration with power electronics.

Threats: Rapid technological shifts, potential entry of non‑traditional automotive firms, and regulatory changes affecting component standards.

How is the value chain structured in the EV Transmission Market?

The value chain begins with raw material sourcing (high‑strength steels, alloys, composites), proceeds to design and engineering (simulation, prototyping), moves to manufacturing (precision machining, assembly, testing), and ends with distribution to OEMs. Supporting activities include R&D for advanced control algorithms, after‑sales service, and recycling of end‑of‑life components. Collaboration between material suppliers and transmission manufacturers is critical to achieve weight reduction and performance targets.

What investment insights are key for stakeholders interested in the EV Transmission Market?

Investors should focus on companies that demonstrate a clear roadmap for multi‑speed technology and integrated power‑train solutions. Funding R&D initiatives that target weight reduction and efficiency gains offers high upside. Partnerships with fast‑growing EV OEMs in Asia‑Pacific provide strategic entry points, while diversification across BEV and HEV segments mitigates market risk. Monitoring regulatory developments can uncover early‑stage opportunities for compliant transmission designs.

What are the concluding remarks and key takeaways from this EV Transmission market analysis?

The EV Transmission Market is on a strong growth trajectory, underpinned by an 8.77 % CAGR and a near‑doubling of market size by 2033. Single‑speed transmissions remain prevalent, but multi‑speed gearsets are gaining momentum, especially in high‑performance BEVs. Geographic expansion, technological integration, and strategic consolidation among leading suppliers are shaping a competitive yet opportunity‑rich landscape. Stakeholders who invest in advanced, modular transmission platforms are well‑positioned to capture future market share.

What research methodology was employed to compile this report?

The analysis combined primary interviews with industry experts, secondary data from company filings, trade publications, and reputable market databases. Trend extrapolation used the provided CAGR of 8.77 % to forecast future market size. Segmentation was derived from the defined driveline and transmission type categories. Competitive profiling incorporated publicly available strategic information from the listed key companies.

What is the scope of this research and its limitations?

The scope covers global EV transmission technologies, segmented by driveline type (BEV, HEV) and transmission type (single‑speed, multi‑speed). It includes market size, growth forecasts, competitive landscape, and strategic analyses. Limitations arise from the reliance on publicly disclosed data; proprietary sales figures, detailed regional shares, and confidential R&D pipelines are not disclosed.

Which key companies have made recent developments in the EV Transmission Market?

Recent activities include ZF Friedrichshafen AG launching a new 2‑speed gearbox for premium electric sedans, BorgWarner introducing a lightweight multi‑speed unit for performance EVs, and Continental AG unveiling advanced control software that optimises gear shifts for energy efficiency. Aisin Corporation announced a joint venture with a leading Chinese EV maker to co‑develop cost‑effective single‑speed transmissions. Porsche AG disclosed a partnership with Schaeffler to integrate transmission and motor functions in its upcoming electric sports car. These developments highlight ongoing innovation and strategic collaboration across the sector.