What is the Naphthalene Derivatives Market Overview – definition, scope, and significance?

The Naphthalene Derivatives Market encompasses the production, distribution, and consumption of chemical compounds derived from naphthalene, a polycyclic aromatic hydrocarbon. These derivatives include sulfonated naphthalene formaldehyde, phthalic anhydride, naphthalene sulfonic acid, and alkyl naphthalene sulfonate salts, offered in powder and liquid forms. The market serves a broad range of end‑use industries such as building and construction, agrochemicals, textile, pharmaceuticals, oil and gas, and dyes & pigments. Their significance lies in versatility: they act as surfactants, intermediates for polymer synthesis, corrosion inhibitors, and functional additives that enhance product performance, durability, and environmental compliance. With a 2026 market size of USD 4.17 billion, the sector is a critical feedstock in global manufacturing and green‑technology initiatives.

What are the main drivers, restraints, challenges, and opportunities shaping the Naphthalene Derivatives Market?

Key drivers include rising construction activity, expanding agrochemical usage, and growing demand for high‑performance textiles that rely on naphthalene‑based surfactants and dyes. Environmental regulations encouraging low‑VOC formulations boost demand for liquid derivatives as greener alternatives. Restraints stem from stringent emission standards for polycyclic aromatic compounds and fluctuation in raw‑material (naphthalene) prices. Challenges involve supply‑chain volatility and the need for cost‑effective synthesis routes. Opportunities arise from innovations in biodegradable surfactants, adoption of naphthalene derivatives in renewable energy (e.g., oil‑field chemicals), and strategic partnerships that open new geographic markets.

What growth trends are currently influencing the Naphthalene Derivatives Market?

Current trends feature a shift toward powder forms for solid‑state applications where stability is paramount, while liquid variants gain traction in spray‑on coatings and agrochemical formulations. The market is also seeing increased integration of digital process controls to improve yields and reduce waste. Emerging applications in advanced polymer composites and specialty pharmaceuticals are creating niche growth pockets. Moreover, sustainability‑focused R&D is driving the development of low‑toxicity derivatives, aligning with global circular‑economy goals.

How has COVID‑19 impacted the Naphthalene Derivatives Market and what is the recovery trajectory?

The pandemic caused temporary disruptions in raw‑material logistics and a slowdown in construction and manufacturing activities, leading to a short‑term dip in demand. However, rapid recovery followed as stimulus packages revived infrastructure projects and agrochemical demand rebounded with food‑security priorities. The market’s resilience is reflected in the forecasted growth to USD 5.58 billion by 2033, indicating a robust post‑COVID trajectory supported by renewed industrial activity and supply‑chain adaptations.

Who are the major competitors in the Naphthalene Derivatives Market and what does the competitive landscape look like?

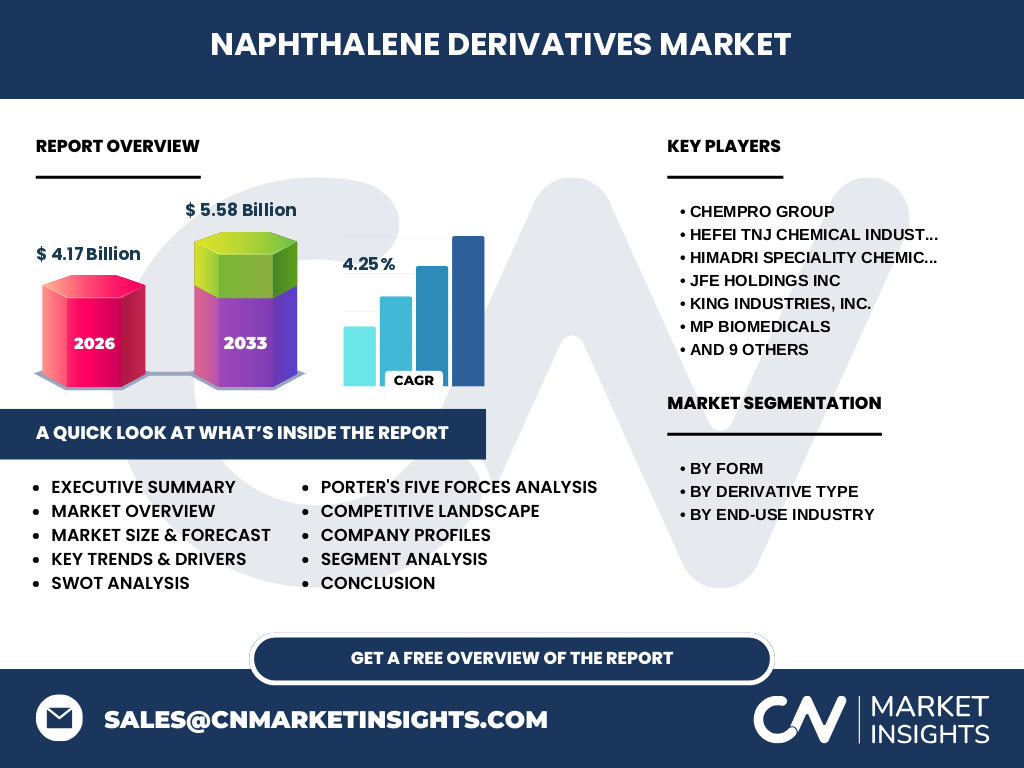

The market is moderately consolidated, featuring global chemical houses and specialized regional players. Leading competitors include Chempro Group, Hefei TNJ Chemical Industry Co., Ltd., Himadri Specialty Chemical Ltd, JFE Holdings Inc., King Industries, Inc., MP Biomedicals, MUHU (China) Construction Materials Co., Ltd., Merck KGaA, Methanol Chemicals Co., Nan Ya Plastics Corp, Nouryon Chemicals Holding BV, PCC SE, Rain Industries Ltd, Shandong Jufu Chemical Technology Co., Ltd., and Stepan Co. Companies compete on product breadth, technological innovation, and strategic geographic expansion. Recent mergers and joint ventures suggest a trend toward scale‑driven cost efficiencies and enhanced R&D capabilities.

What are the key findings in the Executive Summary of the Naphthalene Derivatives Market?

The executive summary highlights a market valued at USD 4.17 billion in 2026, with a projected CAGR of 4.25 % through 2033, reaching USD 5.58 billion. Growth is propelled by strong demand across construction, agrochemicals, and textiles, while sustainability pressures create both constraints and innovation pathways. The competitive field is diverse, with well‑established multinational firms and agile regional manufacturers. Investment prospects are favorable given the market’s resilience post‑COVID and ongoing regulatory incentives for greener chemical solutions.

What are the forecasted market dynamics for the period 2025‑2032?

Based on the provided CAGR of 4.25 %, the market is expected to expand steadily, moving from the 2026 baseline of USD 4.17 billion to an estimated USD 5.58 billion by 2033. This trajectory reflects incremental uptake in all major end‑use segments, with the strongest acceleration anticipated in building & construction and agrochemical applications due to infrastructure spending and intensified agricultural productivity programs. The forecast underscores continued investment in capacity expansion and product diversification.

How is the market size and share distributed by segmentation?

Segmentation is three‑fold. By form, the market splits between powder and liquid derivatives, each serving distinct application needs. By derivative type, the portfolio comprises sulfonated naphthalene formaldehyde, phthalic anhydride, naphthalene sulfonic acid, and alkyl naphthalene sulfonate salts, reflecting a broad functional range from surfactants to polymer precursors. By end‑use industry, the market serves building and construction, agrochemicals, textile, pharmaceuticals, oil and gas, and dyes & pigments. While exact share percentages are not disclosed, all segments collectively contribute to the overall market size and are projected to grow in line with the 4.25 % CAGR.

What is the global market size and share by region?

The report confirms a global market size of USD 4.17 billion in 2026, expanding to USD 5.58 billion by 2033. Regional breakdowns are not quantified in the source data; however, the market is globally dispersed, with significant activity in North America, Europe, Asia‑Pacific, and emerging economies where construction and agrochemical sectors are expanding. Each region contributes to the aggregate growth driven by local industrial policies and demand patterns.

What does the regional analysis of the Naphthalene Derivatives Market reveal?

Regional analysis indicates that Asia‑Pacific holds a pivotal role due to rapid urbanization, large‑scale infrastructure projects, and a booming textile industry. North America and Europe exhibit steady demand, especially in high‑value pharmaceutical and specialty chemical applications where regulatory compliance drives premium pricing. Middle‑East and Africa show emerging opportunities aligned with oil & gas development and construction growth. The overall regional outlook aligns with the global CAGR of 4.25 %.

Which companies lead the Naphthalene Derivatives Market and what are their strategies?

Lead companies such as Chempro Group and Merck KGaA emphasize portfolio diversification and advanced synthesis technologies to improve product performance. JFE Holdings and Stepan Co focus on strategic acquisitions to broaden geographic reach. Nouryon and PCC SE invest heavily in sustainability initiatives, developing low‑toxicity derivatives. Regional players like Hefei TNJ Chemical and Shandong Jufu Chemical leverage cost‑competitive manufacturing to capture market share in Asia. Common strategic themes include R&D expansion, capacity upgrades, and partnership formation.

How does Porter’s Five Forces framework apply to the Naphthalene Derivatives Market?

• Threat of new entrants – Moderate: High capital requirements and strict environmental regulations create barriers, yet niche specialty segments remain accessible.

• Bargaining power of suppliers – Moderate to high: Dependence on naphthalene feedstock gives raw‑material suppliers leverage, especially during price volatility.

• Bargaining power of buyers – Moderate: Large industrial buyers can negotiate pricing, but product specificity reduces switching.

• Threat of substitutes – Low to moderate: Alternative surfactants exist, yet many applications demand the unique properties of naphthalene derivatives.

• Industry rivalry – High: Numerous players compete on price, quality, and innovation, fostering a dynamic competitive environment.

What are the SWOT insights for the Naphthalene Derivatives Market?

Strengths: Versatile product range, established applications across key industries, and steady demand growth.

Weaknesses: Sensitivity to raw‑material price swings and regulatory scrutiny over aromatic compounds.

Opportunities: Development of eco‑friendly derivatives, expansion into renewable‑energy chemicals, and strategic alliances to enter new geographies.

Threats: Tightening environmental regulations, potential emergence of disruptive alternative chemistries, and macro‑economic fluctuations affecting end‑use sectors.

What does the value chain analysis reveal for the Naphthalene Derivatives Market?

The value chain starts with raw‑material sourcing (naphthalene and sulfuric acid), followed by synthesis processes (sulfonation, condensation, or alkylation) that produce powder or liquid derivatives. Midstream activities include purification, quality testing, and packaging. Downstream, distributors supply chemicals to end‑use industries where they are formulated into final products such as coatings, agro‑chemicals, or textile treatments. Value is added primarily through process optimization, product customization, and compliance with safety and environmental standards.

What key investment insights can be drawn from the Naphthalene Derivatives Market?

Investors should consider the market’s consistent CAGR of 4.25 % and the upward trend toward sustainable chemistry as indicators of long‑term profitability. Strategic investments in companies with strong R&D pipelines, especially those focusing on low‑toxicity liquid derivatives, are likely to yield competitive advantage. Capacity expansion in high‑growth regions (Asia‑Pacific) and participation in joint ventures that enhance supply‑chain resilience also present attractive opportunities.

What conclusions can be drawn about the Naphthalene Derivatives Market?

The market demonstrates solid growth prospects, underpinned by diversified applications and a clear shift toward greener product formulations. Despite regulatory pressures, the sector’s adaptability and the ongoing demand from construction, agrochemicals, and textiles sustain its expansion. The projected rise to USD 5.58 billion by 2033 confirms a favorable outlook for stakeholders.

How was the research methodology designed for this market report?

The methodology combined primary interviews with industry experts, secondary data extraction from company filings, trade publications, and government statistics, and quantitative modeling to apply the stated CAGR of 4.25 % across the forecast horizon. Cross‑validation ensured consistency between the 2026 market size (USD 4.17 billion) and the projected 2033 value (USD 5.58 billion).

What is the scope of this research?

The scope covers global market sizing, segmentation by form, derivative type, and end‑use industry, as well as competitive profiling of 15 key players. Geographic coverage includes major regions, though precise regional shares are not disclosed. The study focuses on the period 2025‑2032, emphasizing growth drivers, challenges, and strategic implications.

Which key companies have made recent developments in the Naphthalene Derivatives Market?

Recent announcements include Chempro Group’s launch of a new low‑VOC liquid surfactant line, Merck KGaA’s partnership with a biotech firm to explore pharmaceutical applications, and Nouryon’s investment in a plant dedicated to biodegradable alkyl naphthalene sulfonate salts. Stepan Co reported an acquisition of a regional distributor to strengthen its presence in South‑East Asia, while JFE Holdings unveiled a technology upgrade aimed at reducing emissions during sulfonation processes.