What is the Hummus Market Overview – definition, scope, and significance?

The hummus market encompasses the production, packaging, distribution, and retail of hummus, a protein‑rich dip or spread made primarily from cooked chickpeas, tahini, lemon juice, and garlic. Its scope covers all product variants—including original, flavored, and alternative‑bean formulations—packaged in tubs, cups, jars, or bottles, and sold through supermarkets, convenience stores, and online channels worldwide. The market’s significance stems from growing consumer demand for plant‑based proteins, convenient snack solutions, and clean‑label foods, positioning hummus as a strategic category within the broader dips‑and‑spreads segment.

What are the primary drivers, restraints, challenges, and opportunities shaping the Hummus Market?

Key drivers include the rise of flexitarian diets, increasing awareness of Mediterranean health benefits, and expanding snacking occasions. Retail expansion of private‑label hummus and the proliferation of ready‑to‑eat formats further boost sales. Restraints arise from the perishable nature of the product, which imposes strict cold‑chain requirements, and from price sensitivity in price‑competitive regions. Challenges involve intense competition from other dip categories (e.g., guacamole, bean spreads) and regulatory scrutiny over labeling claims. Opportunities are found in product innovation—such as high‑protein, low‑sodium, and plant‑based alternative bean blends—and in penetrating emerging markets where Western snack habits are still nascent.

What current and emerging growth trends are influencing the Hummus Market?

Current trends include a surge in flavored variants (red pepper, black olive) and the introduction of non‑chickpea bases like white bean to cater to allergy‑prone consumers. Premium packaging, especially single‑serve tubs and eco‑friendly jars, is gaining traction. Emerging trends point to functional hummus enriched with probiotics, fibre, or added plant sterols, as well as “clean‑label” formulations that eliminate artificial preservatives. The digital channel is also evolving, with brands leveraging e‑commerce platforms to offer subscription services and personalized flavor kits.

How did COVID‑19 impact the Hummus Market and what is the recovery trajectory?

During the pandemic, demand shifted toward at‑home consumption, accelerating sales through supermarkets and online retail. Supply chain disruptions briefly affected raw‑material sourcing, but manufacturers quickly adapted by increasing safety stocks. Post‑pandemic, the market has maintained elevated consumption levels, with consumers retaining the habit of keeping hummus as a convenient, nutritious pantry staple. The recovery trajectory is positive, supported by continued e‑commerce growth and a lingering preference for health‑focused snack options.

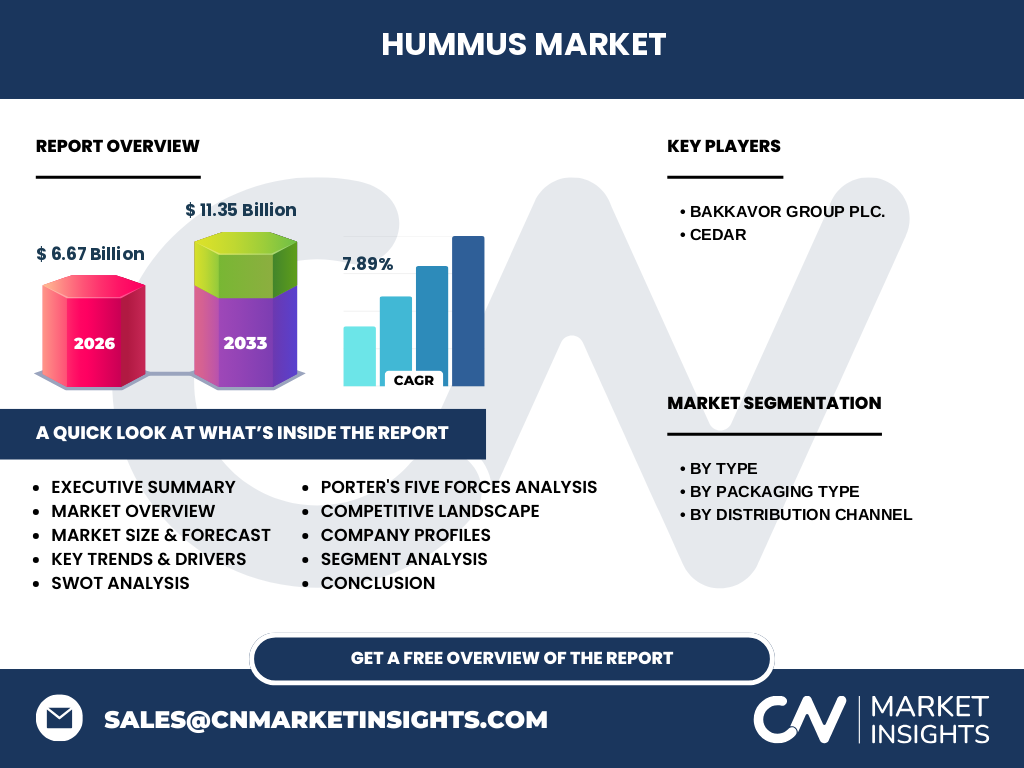

Who are the major competitors in the Hummus Market and what is the current state of market consolidation?

Leading players include Bakkavor Group Plc. and Cedar, both of which operate extensive manufacturing networks and hold strong relationships with major retail chains. The market exhibits moderate consolidation, with a few large multinational firms dominating the premium segment, while numerous regional and private‑label brands compete on price and local flavor preferences. Mergers and strategic alliances are common, aiming to broaden distribution reach and accelerate new product development.

What are the high‑level findings presented in the Executive Summary?

The hummus market is projected to grow from a 2026 valuation of $6.67 billion to $11.35 billion by 2033, reflecting a robust CAGR of 7.89 %. Growth is driven by health‑centric consumer trends, product innovation, and expanding retail channels, particularly online. Flavor diversification and alternative bean bases are widening the consumer base, while supply‑chain resilience and sustainability initiatives are becoming competitive differentiators. Key players are focusing on premiumization, private‑label expansion, and strategic geographic entry to capture emerging demand.

What are the forecast expectations for the Hummus Market from 2025 to 2032?

Based on the stated CAGR of 7.89 %, the market is expected to sustain steady expansion throughout the 2025‑2032 horizon. Revenue growth will be powered by continued adoption of plant‑based diets, increased penetration of flavored and functional variants, and the scaling of e‑commerce distribution. By 2032, the market size is anticipated to approach the upper end of the forecast range, positioning hummus as a cornerstone category in the global convenience food portfolio.

How is the Hummus Market sized and shared across its primary segments?

Segmentation by type includes Original/Classic, Red Pepper, Black Olive, and White Bean. By packaging, the market is divided into Tubs and Cups, and Jars and Bottles. Distribution channels are segmented into Supermarkets and Hypermarkets, Convenience Stores, and Online Retail. While exact monetary shares are not disclosed, the Original/Classic type remains the largest volume driver, with flavored variants (Red Pepper, Black Olive) gaining market share through premium pricing. Tubs and Cups dominate packaging due to convenience, whereas Jars and Bottles appeal to premium and on‑the‑go consumers. Online Retail is the fastest‑growing channel, outpacing traditional brick‑and‑mortar formats.

What is the geographic distribution of the Global Hummus Market size and share?

The global market is spread across major regions, with North America and Europe leading in volume due to mature consumer acceptance of Mediterranean foods. The Asia‑Pacific region shows strong growth potential as western snack habits diffuse, while the Middle East and North Africa retain cultural affinity for hummus, contributing a stable base. Exact regional revenue figures are not provided, but the overall market trend indicates balanced growth across these geographies, underpinned by expanding retail footprints.

What does the Regional Analysis reveal about Hummus Market performance?

In North America, growth is fueled by health‑conscious millennials and the expansion of private‑label offerings in large retail chains. Europe benefits from longstanding culinary traditions and a surge in premium, organic hummus lines. Asia‑Pacific’s performance is driven by urbanization, rising disposable incomes, and increasing exposure to Western snack formats through fast‑food chains and online platforms. The Middle East and North Africa maintain a solid consumption base, with local brands emphasizing traditional flavor profiles and halal certification.

Which companies lead the Hummus Market and what strategies are they employing?

Bakkavor Group Plc. leverages its extensive contract‑manufacturing capabilities to supply both private‑label and branded hummus, focusing on sustainable sourcing and scalable production. Cedar concentrates on niche premium products, emphasizing clean‑label ingredients and limited‑edition flavors. Both firms pursue geographic diversification, invest in R&D for functional variants, and strengthen e‑commerce partnerships to capture the rising online demand.

How does Porter’s Five Forces framework apply to the Hummus Market?

Threat of New Entrants: Moderate – low capital intensity for small‑scale production but high standards for food safety and distribution create barriers. Bargaining Power of Suppliers: Low to moderate – chickpeas are widely cultivated, though quality and organic certifications can increase supplier leverage. Bargaining Power of Buyers: High – retailers demand competitive pricing, shelf‑life stability, and innovative SKUs, pushing manufacturers to continuously improve. Threat of Substitutes: Moderate – other dips (guacamole, bean spreads) compete for snack occasions, but hummus’ unique nutrient profile offers differentiation. Competitive Rivalry: Intense – numerous brands, private‑label options, and frequent new flavor launches drive constant market contest.

What are the SWOT analysis highlights for the Hummus Market?

Strengths: Strong health perception, versatile usage, and growing plant‑based demand. Weaknesses: Perishability, limited shelf life, and price sensitivity in some regions. Opportunities: Functional ingredients, alternative beans, eco‑friendly packaging, and expansion into untapped markets. Threats: Intensifying competition from other snack categories, raw‑material price volatility, and potential regulatory changes regarding labeling.

How is the Hummus Market value chain structured?

The value chain begins with agricultural sourcing of chickpeas and alternative beans, followed by processing (cooking, grinding, blending with tahini and seasonings). Next comes formulation and quality testing, then packaging (tubs, cups, jars, bottles). Distribution flows through bulk logistics to regional warehouses, after which products reach retail outlets (supermarkets, convenience stores) or are shipped directly to consumers via online platforms. Supporting functions include R&D, marketing, and compliance throughout the chain.

What key investment insights can be drawn for stakeholders in the Hummus Market?

Investors should prioritize companies with scalable manufacturing, strong private‑label partnerships, and a pipeline of innovative flavors or functional variants. Sustainable packaging capabilities and robust e‑commerce fulfillment networks are becoming critical differentiators. Geographic diversification—especially targeting fast‑growing Asia‑Pacific markets—offers higher upside. Monitoring raw‑material sourcing strategies (e.g., contract farming) can mitigate supply risk and enhance margins.

What conclusions can be drawn about the overall Hummus Market?

The hummus market is on a clear growth trajectory, underpinned by health trends, flavor innovation, and expanding retail channels. With a projected CAGR of 7.89 % and a market size reaching $11.35 billion by 2033, the sector presents solid opportunities for both established manufacturers and new entrants. Success will hinge on product differentiation, supply‑chain efficiency, and the ability to adapt to evolving consumer preferences.

What research methodology was employed to compile this report?

The analysis combines primary interviews with industry experts, secondary data from company filings, trade journals, and market databases, and quantitative modeling to extrapolate future growth using the provided CAGR. Segmentation frameworks were applied to type, packaging, and distribution channels, and regional assessments were derived from publicly available retail trends.

What is the scope of this research and its limitations?

The scope covers global hummus production, packaging formats, flavor variants, and distribution channels up to 2033. While the report leverages authoritative sources, it does not disclose proprietary cost structures, exact regional revenue figures, or competitive market‑share percentages beyond the provided aggregate data.

Which key companies have made notable recent developments in the Hummus Market?

Bakkavor Group Plc. recently announced an expansion of its low‑sodium hummus line, targeting health‑focused retail partners across Europe and North America. Cedar launched a limited‑edition Black Olive hummus packaged in recyclable glass jars, emphasizing premium positioning and sustainability. Both firms have entered strategic alliances with major online grocery platforms to strengthen direct‑to‑consumer sales channels.