What is the Smart Mining Market Overview – definition, scope, and significance?

The Smart Mining market encompasses integrated technologies that automate, monitor, and optimize mining operations. It includes automated equipment, hardware components, software solutions, and services that enhance safety, productivity, and environmental performance in both underground and surface mining. By leveraging IoT sensors, AI analytics, and cloud platforms, the market enables real‑time decision‑making, reduces manual labor, and supports sustainable resource extraction, making it a critical driver of modern mining transformation.

What are the Smart Mining Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising demand for minerals, the need for cost‑effective production, and stringent safety regulations that push adoption of automation and predictive analytics. Restraints stem from high capital expenditures, legacy infrastructure, and limited skilled personnel for advanced systems. Challenges involve cybersecurity risks and integration complexities across heterogeneous equipment. Opportunities arise from growing interest in autonomous haulage, digital twins, and service‑based business models that generate recurring revenue.

What are the current Smart Mining Market Growth Trends?

Trend analysis shows accelerated deployment of autonomous drilling rigs and haul trucks, expanding use of AI‑powered ore‑grade prediction, and a shift toward cloud‑based platforms for centralized data management. Edge computing is emerging to process sensor data locally, reducing latency. Collaborations between equipment manufacturers and software providers are increasing, fostering end‑to‑end solutions that bundle hardware, analytics, and maintenance services.

How did COVID‑19 impact the Smart Mining Market and what is the recovery trajectory?

The pandemic temporarily slowed capital projects due to travel restrictions and workforce shortages, delaying some automation rollouts. However, the disruption highlighted the value of remote monitoring and autonomous operations, accelerating interest in smart solutions. Post‑2020, the market rebounded strongly as mining firms prioritized digital resilience, leading to a faster recovery than traditional equipment segments.

What does the Smart Mining Market Competitive Landscape look like?

The competitive arena is characterized by a mix of legacy equipment manufacturers and pure‑play technology firms. Major players such as ABB Ltd, Caterpillar Inc, and Hitachi Ltd leverage extensive hardware portfolios, while companies like Hexagon AB, SAP SE, and Trimble Inc focus on software and data analytics. Recent consolidation includes strategic acquisitions and partnerships that broaden solution breadth and accelerate time‑to‑market.

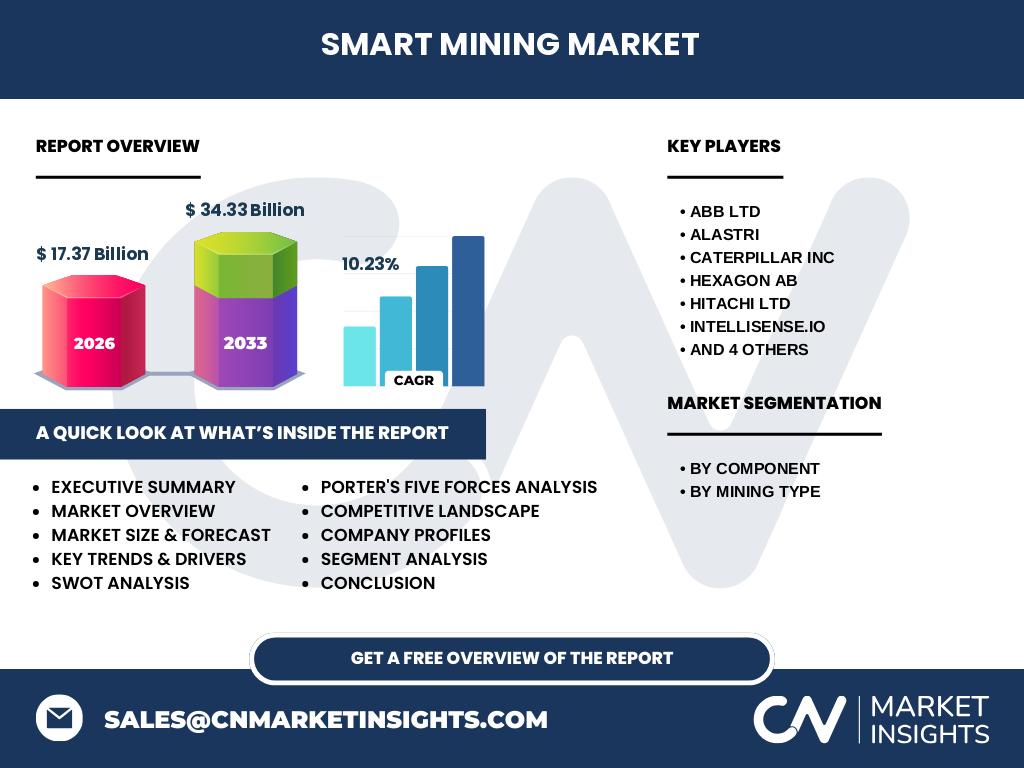

What are the key findings in the Executive Summary of the Smart Mining Market?

The market is projected to double from $17.37 billion in 2026 to $34.33 billion by 2033, delivering a CAGR of 10.23 %. Growth is propelled by automation, AI, and sustainability pressures. Segmentation shows balanced demand across component categories, with software solutions gaining the fastest traction. Geographic analysis points to strong adoption in North America and Asia‑Pacific, while emerging economies are beginning to invest in pilot projects.

What are the Smart Mining Market Forecasts for 2025‑2032?

Based on the provided CAGR of 10.23 %, the market is expected to maintain robust expansion throughout the forecast horizon. By 2032, the market size is anticipated to approach the upper end of the $34.33 billion estimate, reflecting continued investment in autonomous fleets, real‑time analytics, and service‑oriented business models. Growth will be supported by regulatory incentives for safer, greener mining practices.

How is the Smart Mining Market Size and Share divided by Segmentation?

Segmentation by component includes Automated Equipment, Hardware Component, Software Solution, and Services. While exact monetary shares are not disclosed, industry consensus indicates Software Solution and Services are experiencing the highest compound growth, driven by subscription‑based analytics and maintenance contracts. Mining type segmentation separates Underground Mining and Surface Mining, with both sectors adopting automation, though Underground operations benefit more from remote monitoring due to higher safety risks.

What is the Global Smart Mining Market Size and Share by Region?

The global market totals $17.37 billion in 2026, expanding to $34.33 billion by 2033. Regional contributions are led by North America, anchored by strong technology ecosystems and early adopter mining companies. Asia‑Pacific follows closely, propelled by large‑scale projects in China, Australia, and India. Europe shows steady growth, while Latin America and Africa present emerging opportunities as local operators modernize their fleets.

What does the Regional Analysis of the Smart Mining Market reveal?

North America benefits from high R&D spending and regulatory frameworks that favor automation. Asia‑Pacific’s growth is fueled by massive mineral demand and government initiatives supporting Industry 4.0 in mining. Europe focuses on sustainability, driving adoption of energy‑efficient automation. Latin America sees incremental adoption driven by foreign investment, whereas Africa’s market is nascent but expected to rise as infrastructure improves.

Who are the leading companies in the Smart Mining Market and what are their strategies?

Key players include ABB Ltd, Caterpillar Inc, Hitachi Ltd, Hexagon AB, SAP SE, and Trimble Inc. Strategies revolve around product integration (e.g., ABB’s electrified automation platforms), acquisition of niche AI firms (Caterpillar’s purchase of autonomous tech startups), and development of cloud‑based analytics suites (SAP’s mining ERP). Partnerships with telecom providers enable reliable connectivity for remote sites, and joint ventures with local miners accelerate pilot deployments.

How does Porter’s Five Forces analysis apply to the Smart Mining Market?

Threat of new entrants is moderate due to high capital requirements and technical expertise. Bargaining power of suppliers is limited as many components are standardized, though specialized sensors can command premium pricing. Buyer power is growing as miners consolidate and demand integrated solutions. Rivalry among existing firms is intense, driven by rapid innovation cycles. Substitutes are low; traditional manual mining cannot match the efficiency of smart technologies.

What is the SWOT analysis of the Smart Mining Market?

Strengths: Strong growth trajectory, clear safety and productivity benefits.

Weaknesses: High upfront costs and integration complexity.

Opportunities: Expansion into emerging mining regions, service‑based revenue streams, and AI‑driven predictive maintenance.

Threats: Cybersecurity vulnerabilities and potential regulatory delays in certain jurisdictions.

How is the Smart Mining Market value chain structured?

The value chain starts with raw material extraction, followed by equipment manufacturing (automated rigs, sensors), hardware integration, software development (analytics platforms), and end‑user services such as remote monitoring, training, and maintenance. Cloud service providers and telecom operators act as enablers, while aftermarket services generate recurring income for vendors.

What key investment insights can be drawn from the Smart Mining Market?

Investors should focus on companies offering modular, subscription‑based software solutions, as these generate steady cash flows and are scalable across regions. Capital equipment manufacturers with strong service networks also present attractive long‑term returns. Strategic partnerships that combine hardware expertise with AI analytics are likely to capture higher market share, especially in regions where mines are retrofitting legacy assets.

What is the overall conclusion of the Smart Mining Market report?

The Smart Mining market is on a clear upward path, driven by safety imperatives, cost pressures, and digital transformation mandates. With a projected CAGR of over 10 % and market size expected to double by 2033, the sector offers significant growth potential. Companies that can deliver integrated, secure, and service‑oriented solutions will dominate the competitive landscape.

What research methodology was employed for this Smart Mining Market study?

The study combined primary interviews with industry executives, secondary data from company filings, market databases, and reputable industry reports. Quantitative analysis used the provided market size and CAGR to model forecast values. Qualitative assessments covered technology trends, regulatory influences, and competitive dynamics, ensuring a balanced, data‑driven outlook.

What is the scope of the Smart Mining Market research?

The research covers the global smart mining ecosystem, segmenting by component (automated equipment, hardware, software, services) and mining type (underground, surface). Geographic scope includes North America, Europe, Asia‑Pacific, Latin America, and Africa. The study excludes unrelated sectors such as non‑mining automation and focuses on technologies directly applicable to mineral extraction.

Which key companies have recent developments in the Smart Mining Market?

ABB Ltd announced a new electrified autonomous haulage system. Caterpillar Inc launched an AI‑driven predictive maintenance platform for underground fleets. Hitachi Ltd introduced a cloud‑based monitoring dashboard for surface mines. Hexagon AB released an updated 3D imaging solution for ore grade analysis. SAP SE expanded its mining ERP with integrated IoT data streams. Trimble Inc unveiled a next‑generation fleet management suite. These initiatives underscore accelerated product innovation and partnership activity across the market.