What is the GCC Ice Cream Market Overview – Definition, scope, and significance?

The GCC Ice Cream Market encompasses the production, distribution, and consumption of frozen dairy desserts across the Gulf Cooperation Council (Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Oman, and Bahrain). It includes all forms (cups, tubs, bars, soft‑serve cones, etc.), flavors, and categories (conventional and sugar‑free) sold through supermarkets, specialty stores, online retail, vending machines, and other channels. With a 2026 market size of US 1.93 billion, the sector represents a critical component of the region’s food‑and‑beverage industry, driven by high disposable incomes, a youthful population, and a growing preference for premium and health‑conscious desserts.

What are the GCC Ice Cream Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising per‑capita income, expanding tourism, and increasing urbanisation that boost demand for premium and novel ice‑cream formats. The growing health‑conscious segment fuels demand for sugar‑free and functional variants. Restraints stem from the region’s hot climate, which can limit year‑round consumption, and from stringent halal certification requirements. Challenges involve supply‑chain volatility for dairy inputs and heightened competition from frozen yogurt and plant‑based desserts. Opportunities arise from product innovation (e.g., exotic fruit flavors like mango and blueberry), digital sales channels, and partnerships with local retailers to expand distribution in underserved secondary cities.

What are the current GCC Ice Cream Market Growth Trends?

Trend analysis shows a shift toward premium, single‑serve formats such as cups and bars, driven by on‑the‑go lifestyles. Flavor diversification is prominent, with tropical and berry flavors (mango, raspberry, blueberry) gaining market traction alongside classic vanilla and chocolate. Sugar‑free and low‑calorie lines are expanding rapidly, reflecting consumer health awareness. Additionally, the adoption of online retail and contactless delivery has accelerated, especially for specialty and limited‑edition products. Brands are also leveraging limited‑time collaborations with local influencers and culinary personalities to create buzz.

How has COVID‑19 impacted the GCC Ice Cream Market and what is the recovery trajectory?

During the pandemic, on‑premise consumption (restaurants, cafés) declined sharply, while off‑premise sales (supermarkets, online orders) surged as consumers stocked up for home consumption. The sector experienced a brief contraction in early 2020, followed by strong rebound driven by increased household spending on comfort foods. Recovery has continued post‑pandemic, with a clear trend toward hybrid purchasing—customers buying core packs in stores but seeking niche flavors online. The market is now on a steady growth path, supported by the projected CAGR of 5.90% for 2027‑2033.

Who are the major competitors in the GCC Ice Cream Market and what is the competitive landscape?

The market is moderately consolidated, led by multinational and regional players. Key competitors include BR IP Holders LLC (Baskin‑Robbins), Nestlé SA, Unilever plc, General Mills Inc., IFFCO Group, Saudia Dairy & Foodstuff Company (SADAFCO), Bulla Dairy Foods, Pure Ice Cream Co LLC (Kwality), Unikai Foods PJSC, and Thrriv LLC. These firms compete on brand equity, flavor innovation, and distribution reach. Recent years have seen strategic acquisitions and joint ventures aimed at expanding product portfolios and strengthening local supply chains, indicating a trend toward deeper market integration.

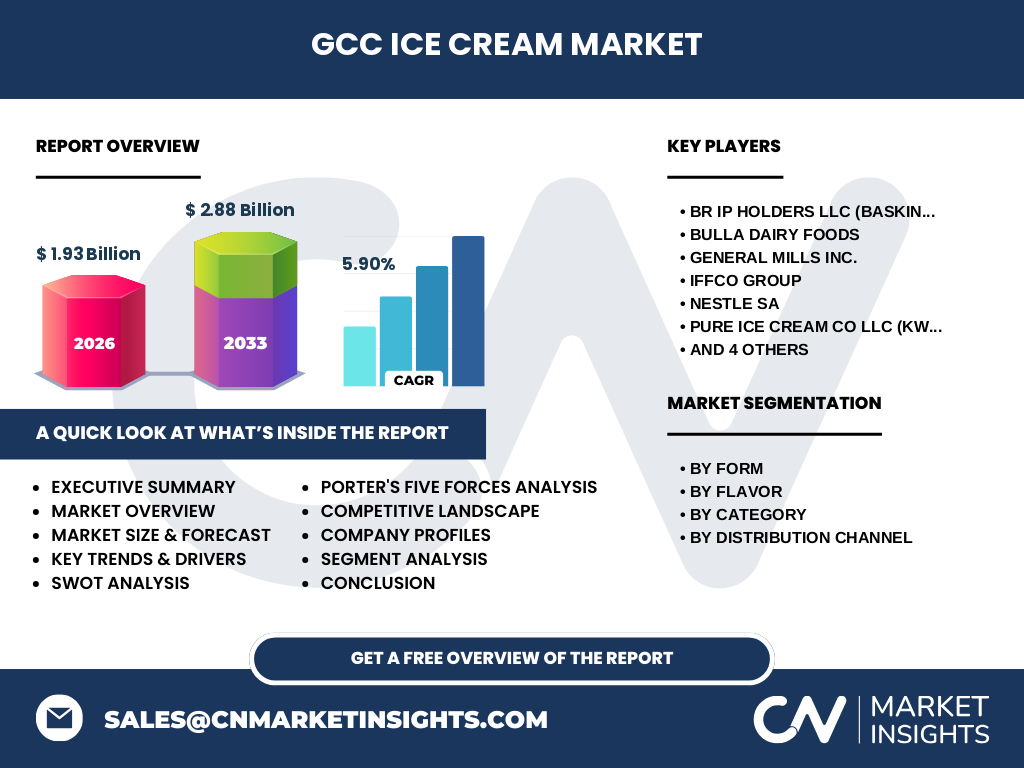

What does the Executive Summary reveal about the GCC Ice Cream Market?

The GCC Ice Cream Market is valued at US 1.93 billion in 2026 and is expected to reach US 2.88 billion by 2033, delivering a robust CAGR of 5.90%. Growth is propelled by premiumization, health‑focused categories, and expanding digital sales channels. Core segments—cups and tubs, followed by bars and sticks—command the largest volume, while mango, raspberry, and blueberry flavors are emerging growth drivers. Competitive dynamics are shaped by a blend of global giants and agile regional firms, all investing in product differentiation and omnichannel distribution. The outlook remains positive, with strong demand fundamentals and ample opportunities for innovation.

What are the forecasts for the GCC Ice Cream Market from 2025 to 2032?

Based on the provided CAGR of 5.90%, the market is projected to expand from its 2026 base of US 1.93 billion to approximately US 2.88 billion by the end of the forecast horizon (2033). This translates into consistent year‑over‑year growth, with each segment—form, flavor, category, and channel—expected to contribute proportionally to the overall increase. Premium and health‑oriented product lines are likely to outpace the market average, while traditional mass‑market formats will maintain stable volume.

How is the GCC Ice Cream Market sized and shared by segmentation?

By Form, cups and tubs lead the market owing to their convenience and variety, followed by bars and sticks, soft‑serve and cones, and an “others” category covering niche formats. By Flavor, classic vanilla and chocolate retain strong share, while fruit‑based options—mango, raspberry, blueberry—are gaining momentum. By Category, conventional ice cream dominates, but the sugar‑free segment is expanding rapidly as health trends intensify. By Distribution Channel, supermarkets and hypermarkets hold the largest share, with specialty stores, online retail, and vending machines providing supplemental growth avenues.

What is the Global GCC Ice Cream Market size and share by region?

The GCC region contributes a significant portion of the global ice‑cream market, with a 2026 valuation of US 1.93 billion. While precise global figures are not disclosed, the GCC’s growth rate of 5.90% surpasses many mature markets, highlighting its importance as a high‑growth hub within the worldwide frozen dessert landscape.

What does the Regional Analysis of the GCC Ice Cream Market reveal?

Within the GCC, Saudi Arabia and the United Arab Emirates are the largest consumers, driven by population size and robust retail networks. Qatar and Kuwait exhibit higher per‑capita spending on premium ice‑cream formats, whereas Oman and Bahrain show steady growth in traditional channels. All six states demonstrate parallel trends in flavor diversification and sugar‑free adoption, but the pace of digital channel penetration varies, with the UAE leading online retail sales.

Which companies lead the GCC Ice Cream Market and what are their strategies?

Leading firms include BR IP Holders LLC (Baskin‑Robbins), focusing on brand experience stores and limited‑edition flavors; Nestlé SA, leveraging its extensive R&D to launch sugar‑free lines; Unilever plc, capitalizing on its global “Ben & Jerry’s” brand for premium positioning; General Mills Inc., expanding its snack‑style ice‑cream bars; IFFCO Group, emphasizing locally sourced dairy and halal compliance; SADAFCO, reinforcing its domestic production capacity; Bulla Dairy Foods, targeting family‑size packs; Pure Ice Cream Co LLC (Kwality), offering niche regional flavors; Unikai Foods PJSC, developing private‑label solutions; and Thrriv LLC, innovating with plant‑based alternatives.

How does Porter’s Five Forces analysis apply to the GCC Ice Cream Market?

Threat of new entrants is moderate; high capital requirements and strict halal certification create barriers, yet digital‑first brands can bypass traditional distribution. Bargaining power of suppliers is moderate, as dairy inputs are regionally sourced but vulnerable to price volatility. Bargaining power of buyers is strong, given the abundance of brands and price sensitivity in mass‑market segments. Threat of substitutes is rising, with frozen yogurt, gelato, and plant‑based desserts competing for health‑oriented consumers. Rivalry among existing firms is intense, driven by continuous product innovation and aggressive promotional activities.

What are the SWOT insights for the GCC Ice Cream Market?

Strengths: High disposable income, young demographic, and strong retail infrastructure. Weaknesses: Climate constraints limiting consumption periods and reliance on imported dairy inputs. Opportunities: Expansion of sugar‑free and functional ice creams, digital sales channels, and localized flavor development. Threats: Emerging health‑focused desserts, price pressure from private‑label brands, and potential regulatory changes impacting ingredient sourcing.

How is the value chain structured in the GCC Ice Cream Market?

The value chain begins with raw‑material procurement (milk, cream, sweeteners, flavors)—often sourced locally or imported under halal standards—followed by processing and formulation at manufacturing plants. Finished products are then packaged and distributed through a mix of centralized logistics hubs and direct‑store delivery for supermarkets, hypermarkets, and specialty outlets. Online retail adds a last‑mile delivery layer, while vending machines provide impulse sales in high‑traffic locations. Marketing and brand management overlay the entire chain, driving consumer awareness and loyalty.

What key investment insights can be drawn for the GCC Ice Cream Market?

Investors should focus on companies that are expanding sugar‑free and functional portfolios, as these segments are projected to outpace overall market growth. Acquisitions of local dairies or partnerships with regional distributors can mitigate supply‑chain risks and enhance halal compliance. Digital platforms present a high‑return avenue; allocating capital to e‑commerce capabilities and data‑driven marketing will capture the accelerating online demand. Finally, targeting niche flavor innovations aligned with regional taste preferences (e.g., mango, raspberry) offers differentiation and premium pricing power.

What are the main conclusions of the GCC Ice Cream Market report?

The GCC Ice Cream Market is on a solid upward trajectory, moving from US 1.93 billion in 2026 to an estimated US 2.88 billion by 2033, driven by a 5.90% CAGR. Premiumization, health‑focused product lines, and digital distribution are the key levers of growth. While climate and ingredient volatility pose challenges, the region’s affluent consumer base and evolving retail landscape provide ample opportunities for brands that innovate and adapt quickly.

What research methodology was employed for this market study?

The study combines primary interviews with industry executives, distributors, and retail buyers across the GCC, with secondary data sourced from company reports, trade publications, and government statistics. Forecasts were generated using a compound annual growth rate (CAGR) model based on the provided market size figures (US 1.93 billion in 2026 and US 2.88 billion in 2033) and validated through cross‑checking with historical trends.

What is the scope of this research and its limitations?

The research covers the entire GCC region, addressing all major product forms, flavors, categories, and distribution channels. It focuses on the period 2025‑2032 for forward‑looking insights. Limitations include the absence of granular market share percentages for individual companies and the unavailability of country‑specific revenue breakdowns, which are typical constraints in regional aggregate studies.

Which key companies are highlighted and what recent developments have they announced?

Prominent firms include BR IP Holders LLC (Baskin‑Robbins), which recently launched a limited‑edition Arabian spice flavor; Nestlé SA, introducing a new line of sugar‑free ice creams in partnership with local supermarkets; Unilever plc, expanding its Ben & Jerry’s boutique stores in Dubai; General Mills Inc., rolling out snack‑size ice‑cream bars targeting on‑the‑go consumers; IFFCO Group, announcing a joint venture to secure dairy supply from the UAE; SADAFCO, investing in a new production facility in Riyadh; Bulla Dairy Foods, releasing a family‑size mango pack; Pure Ice Cream Co LLC (Kwality), unveiling a regional “Desert Date” flavor; Unikai Foods PJSC, securing a private‑label contract with a Gulf‑wide retail chain; and Thrriv LLC, launching a plant‑based ice‑cream line aimed at health‑conscious millennials.