1. What is the Australia A2P SMS Market and why is it significant?

The Australia A2P (Application‑to‑Person) SMS market comprises messaging services where enterprises transmit automated text messages to end‑users for notifications, authentication, marketing, and customer engagement. Its scope includes traditional managed messaging, cloud API platforms, and related value‑added services across multiple verticals. Significance stems from the high mobile penetration in Australia, regulatory support for secure messaging, and the growing reliance on omnichannel communication strategies that position A2P SMS as a reliable, instant, and cost‑effective channel for businesses of all sizes.

2. What are the main drivers, restraints, challenges, and opportunities shaping the Australia A2P SMS market?

Key drivers include the surge in digital transformation initiatives, expanding e‑commerce, and the need for two‑factor authentication (2FA) in banking and retail. Regulatory frameworks encouraging opt‑in compliance further boost adoption. Restraints involve tariff pressure from low‑cost consumer SMS alternatives and the increasing preference for OTT messaging apps. Challenges revolve around network congestion during peak periods and the necessity for robust data‑privacy measures. Opportunities arise from the integration of AI‑driven personalization, the rollout of 5G, and the rise of cloud‑based API platforms that enable rapid scalability for SMEs and large enterprises alike.

3. Which growth trends are currently influencing the Australia A2P SMS market?

Current trends feature a shift from legacy carrier‑managed services toward cloud API messaging platforms that offer real‑time analytics and programmable workflows. Enterprises are also adopting hybrid models that combine SMS with push notifications and email to create seamless omnichannel campaigns. Moreover, the proliferation of Internet‑of‑Things (IoT) devices is prompting new use cases such as remote device alerts and telematics updates via SMS.

4. How did COVID‑19 affect the Australia A2P SMS market and what is the recovery outlook?

The pandemic accelerated digital engagement as businesses moved online, driving a sharp uptick in authentication messages, order confirmations, and health‑related alerts. While initial spikes subsided, the market retained higher baseline volumes post‑COVID‑19 due to lasting changes in consumer behavior and the entrenchment of remote service models. Recovery is now steady, with growth projected to continue along the pre‑pandemic trajectory.

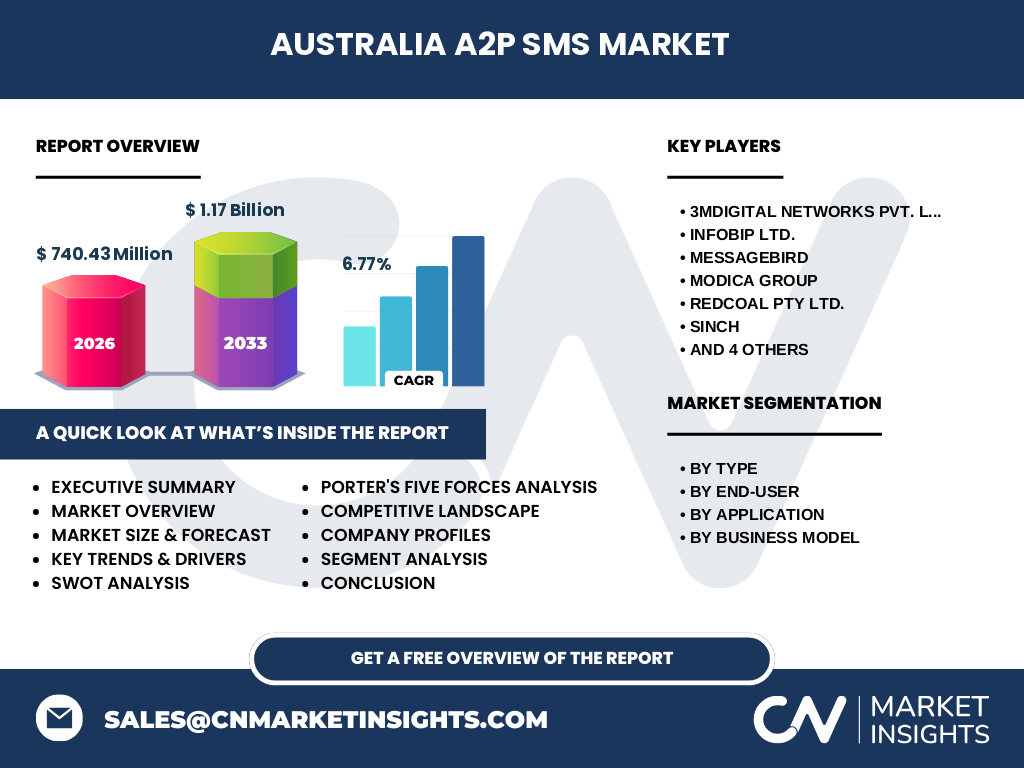

5. Who are the major competitors and what is the level of consolidation in the Australia A2P SMS market?

The competitive landscape features a mix of global telecom operators, pure‑play messaging platforms, and regional technology firms. Notable players include Optus (Singtel Optus Pty Limited), Vodafone Group plc, Twilio, Infobix Ltd., MessageBird, Sinch, and local innovators such as 3mDigital Networks and RedCoal Pty Ltd. Consolidation is moderate, driven by strategic acquisitions—particularly of niche API providers—aimed at expanding service portfolios and geographic reach.

6. What are the high‑level findings of the Australia A2P SMS market?

The market is valued at 740.43 million in 2026 and is forecast to reach 1.17 billion by 2033, reflecting a CAGR of 6.77 %. Growth is underpinned by strong demand across BFSI, retail, and travel sectors, and a clear shift toward cloud‑based API solutions. Competitive pressures are balanced by opportunities in AI‑enhanced personalization and 5G‑enabled services. The outlook remains positive, with robust adoption expected from both large enterprises and SMEs.

7. What are the market forecasts for Australia A2P SMS from 2025 to 2032?

Based on the provided CAGR of 6.77 %, the market is projected to expand from roughly 680 million in 2025 to 1.17 billion by 2033. This trajectory suggests steady annual increases, driven by continued enterprise digitization, regulator‑mandated authentication, and expanding use of SMS for promotional and CRM activities across all end‑user segments.

8. How is the Australia A2P SMS market sized and shared across its main segments?

Segmentation by type distinguishes traditional & managed messaging services from cloud API platforms, with the latter gaining momentum due to developer‑friendly integration. By end‑user, finance, media, travel, hospitality, and retail each contribute to overall volume, with BFSI leading in authentication and fraud‑prevention traffic. Application segmentation shows pushed content services and interactive services as the primary drivers, while promotional campaigns and CRM services remain essential for brand engagement. The business model split highlights large enterprises demanding high‑volume, compliant solutions, whereas SMEs increasingly adopt API‑based, pay‑as‑you‑go models.

9. What is the geographic distribution of the Australia A2P SMS market globally?

Australia represents a mature, high‑value segment within the broader Asia‑Pacific A2P SMS landscape. While specific regional share percentages are not disclosed, the market’s size and growth rate position it as a key contributor to global A2P revenues, especially when compared with emerging markets that are still scaling basic mobile penetration.

10. How does the market perform across different regions within Australia?

Performance is strongest in major economic hubs such as New South Wales and Victoria, where financial services and technology firms concentrate. Secondary markets like Queensland and Western Australia show solid growth driven by tourism, mining communications, and regional retail chains. Nationwide, carrier coverage ensures uniform delivery reliability, supporting consistent adoption across all states.

11. Which companies lead the Australia A2P SMS market and what are their strategies?

Leading players include Optus and Vodafone, leveraging extensive carrier networks to offer bundled enterprise packages. Twilio and Sinch focus on developer ecosystems, providing robust APIs and global routing. MessageBird and Infobip emphasize multi‑channel platforms that combine SMS with chat apps and voice. Local firms such as 3mDigital Networks and RedCoal differentiate through customized compliance services for Australian regulations. Most competitors pursue a blend of organic product development and strategic acquisitions to broaden service breadth.

12. What does Porter’s Five Forces analysis reveal about the market?

Threat of new entrants is moderate; while cloud API platforms lower entry barriers, compliance and carrier relationships present hurdles. Bargaining power of buyers is high, as enterprises can switch between providers based on pricing and feature sets. Bargaining power of suppliers (mobile network operators) remains moderate since many A2P providers negotiate bulk SMS rates. Threat of substitutes is moderate‑low; OTT messaging lacks the universal reach and reliability of SMS for critical alerts. Competitive rivalry is intense, with many firms vying on price, latency, and value‑added analytics.

13. What are the SWOT highlights for the Australia A2P SMS market?

Strengths: Universal device compatibility, high open rates, and regulatory backing for secure messaging.

Weaknesses: Limited richness compared with OTT channels and cost sensitivity to high‑volume pricing.

Opportunities: AI‑driven personalization, 5G‑enabled ultra‑low latency, and expansion into IoT alerts.

Threats: Emerging consumer‑preferred messaging apps and potential regulatory changes affecting opt‑in practices.

14. How does the value chain of the Australia A2P SMS market operate?

The value chain starts with content creation (brands, agencies), moves to integration (API or platform setup), then routing through carrier aggregators or directly via mobile network operators. Delivery involves SMSC (Short Message Service Center) processing, followed by delivery reporting and analytics that feed back into campaign optimization. Supporting services such as compliance verification and number verification sit alongside each stage.

15. What investment insights are most relevant for stakeholders?

Investors should focus on companies that combine carrier‑level reach with scalable API ecosystems, as this hybrid model offers both reliability and growth potential. Strategic partnerships between telecom operators and cloud messaging innovators are likely to generate outsized returns. Additionally, funding AI‑enabled analytics platforms can capture value from higher‑margin, data‑driven services.

16. What are the key takeaways from the Australia A2P SMS market analysis?

The market is on a clear growth path, forecast to exceed 1.17 billion by 2033, driven by enterprise digitization, regulatory demand for secure communication, and the shift toward cloud API platforms. While competition is fierce, opportunities abound in AI personalization, 5G integration, and IoT use cases. Companies that can balance carrier reliability with innovative, developer‑friendly solutions are best positioned to capture market share.

17. How was the research for this report conducted?

The study combined primary interviews with industry experts, secondary data from carrier reports, regulatory publications, and financial filings of listed vendors. Trend analysis leveraged historical volume data, while forecasting applied the disclosed CAGR of 6.77 % to extrapolate future market size. Validation was performed through cross‑checking with independent market intelligence sources.

18. What is the scope of this research and its limitations?

The scope covers the entire Australian A2P SMS ecosystem, segmented by type, end‑user, application, and business model, and includes competitive, strategic, and financial analyses up to 2033. Limitations stem from the reliance on publicly available data and the exclusion of proprietary carrier pricing structures, which may affect granular cost‑benefit assessments.

19. Which companies are highlighted and what recent developments have they announced?

Key players such as Optus and Vodafone have rolled out enhanced API gateways supporting 5G latency targets. Twilio announced a partnership with Australian fintech firms to streamline 2FA compliance. Sinch introduced AI‑based message routing to improve delivery confidence. MessageBird expanded its multi‑channel hub with native integration to Australian CRM platforms. Local innovators like 3mDigital Networks launched a compliance‑focused dashboard that automates opt‑in verification for SMEs. These developments illustrate a market moving toward greater automation, regulatory alignment, and cross‑channel flexibility.