1. Europe Cochlear Implants Market Overview - Definition, scope, and significance?

The Europe Cochlear Implants Market comprises manufacturers, distributors, and service providers of electronic medical devices that restore hearing for individuals with severe to profound sensorineural hearing loss. The market scope covers both adult and pediatric end‑users and includes unilateral and bilateral implantation procedures. Its significance stems from the growing prevalence of hearing impairment, advances in digital signal processing, and strong public health initiatives across European nations that promote early detection and rehabilitation of hearing loss.

2. Europe Cochlear Implants Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising awareness of hearing health, supportive reimbursement policies in countries such as Germany, France, and the UK, and continuous innovation in implant miniaturization and sound‑processing algorithms. Restraints involve high upfront costs, stringent regulatory approvals, and limited access in less affluent regions of Europe. Challenges relate to the need for skilled surgeons and post‑operative audiology support, while opportunities arise from expanding pediatric screening programs, the advent of remote fitting technologies, and potential collaborations between device makers and tele‑health providers.

3. Europe Cochlear Implants Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a shift toward bilateral implantation to enhance sound localization and speech perception in noisy environments. Emerging trends feature fully implantable systems, AI‑driven adaptive sound processing, and integration with smartphone applications for real‑time user customization. Additionally, there is a noticeable increase in demand for minimally invasive surgical techniques that reduce operative time and postoperative complications.

4. COVID-19 Impact on the Europe Cochlear Implants Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic temporarily slowed elective surgeries, leading to a short‑term dip in implantation volumes across Europe. However, the market rebounded quickly as hospitals reinstated non‑emergency procedures and tele‑audiology services expanded, enabling remote programming and follow‑up care. The recovery trajectory is positive, supported by pent‑up demand, especially among pediatric patients whose early intervention windows were delayed during lockdowns.

5. Europe Cochlear Implants Market Competitive Landscape - Major competitors and market consolidation?

The competitive landscape is dominated by established players such as Cochlear Ltd., MED‑EL, and Sonova, alongside strong challengers like Demant A/S, GN Hearing A/S, and Starkey. Recent years have witnessed strategic mergers, joint ventures, and acquisitions aimed at broadening product portfolios and geographic reach. Companies are also investing heavily in R&D to differentiate through advanced signal processing, battery longevity, and wireless connectivity.

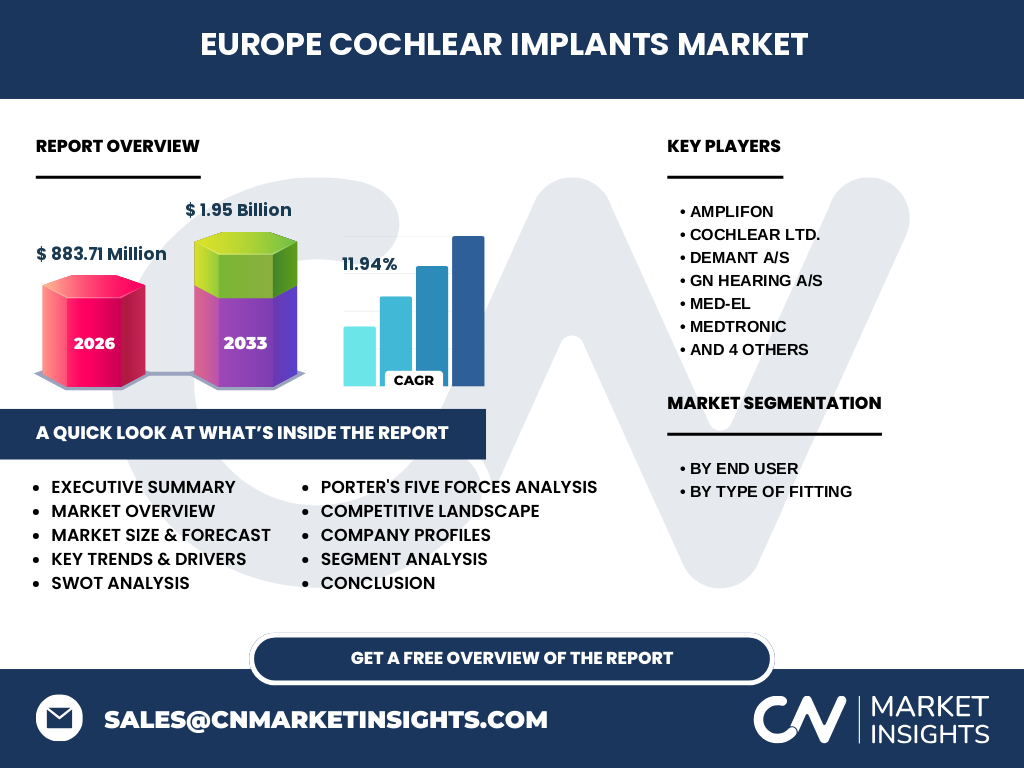

6. Executive Summary - High-level overview and key findings about Europe Cochlear Implants Market?

The Europe Cochlear Implants Market is valued at €883.71 million in 2026 and is projected to reach €1.95 billion by 2033, reflecting a robust CAGR of 11.94%. Growth is propelled by demographic aging, heightened pediatric screening, and supportive reimbursement frameworks. While cost and regulatory hurdles persist, innovation in bilateral and fully implantable solutions, coupled with expanding tele‑fit services, positions the market for sustained expansion throughout the forecast period.

7. Europe Cochlear Implants Market Forecast - Projections for 2025-2032 period?

Based on the stated CAGR of 11.94%, the market is expected to maintain a strong upward trajectory from 2025 through 2032. The forecast underscores continued year‑on‑year growth, driven by increasing implantation rates, especially in bilateral procedures, and the rollout of next‑generation devices that address both adult and pediatric needs. Investment in training programs for otologic surgeons is also anticipated to support this expansion.

8. Europe Cochlear Implants Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by end‑user reveals two primary groups: Adults and Pediatrics. Both segments are experiencing growth, with pediatrics benefiting from nationwide newborn hearing screening initiatives, while adults drive volume through age‑related hearing loss. By type of fitting, unilateral implantation remains the baseline offering, but bilateral implantation is gaining market share due to superior auditory outcomes and patient preference for immersive sound experiences.

9. Global Europe Cochlear Implants Market Size and Share by Region - Geographic distribution?

Europe accounts for a significant portion of the global cochlear implant landscape, anchored by mature healthcare systems and high per‑capita spending on medical technologies. The region’s market size of €883.71 million in 2026 illustrates its leading role, with the forecasted €1.95 billion by 2033 indicating that Europe will continue to command a sizable share of worldwide demand alongside North America and Asia‑Pacific.

10. Regional Analysis of the Europe Cochlear Implants Market - Detailed regional market performance?

Western Europe, led by Germany, the United Kingdom, and France, shows the highest adoption rates due to robust reimbursement schemes and well‑established audiology networks. Northern Europe, particularly Scandinavia, demonstrates strong market penetration driven by early technology adoption and comprehensive public health programs. Southern and Eastern European markets are emerging, with growing governmental support and rising awareness contributing to incremental uptake.

11. Leading Company Profiles in the Europe Cochlear Implants Market - Industry players and strategies?

Key players include Cochlear Ltd., MED‑EL, Sonova, Demant A/S, GN Hearing A/S, Amplifon, Medtronic, Nurotron Biotechnology Co. Ltd., Starkey, and WIDEX A/S. These firms focus on product diversification, strategic partnerships with hospitals and audiology clinics, and expansion of service networks. R&D investment is concentrated on wireless connectivity, AI‑enabled sound processing, and fully implantable device platforms to capture premium market segments.

12. Porter's Five Forces Analysis of the Europe Cochlear Implants Market - Competitive forces assessment?

• Threat of new entrants: Low, due to high capital requirements and regulatory barriers.

• Bargaining power of suppliers: Moderate, as component suppliers for micro‑electronics hold some influence, but large manufacturers often negotiate long‑term contracts.

• Bargaining power of buyers: Growing, with health insurers and national health services demanding cost‑effectiveness and outcome data.

• Threat of substitutes: Low, because alternative hearing solutions (e.g., hearing aids) cannot fully address severe sensorineural loss.

• Industry rivalry: High, driven by a concentrated group of innovators competing on technology, clinical evidence, and service quality.

13. SWOT Analysis of the Europe Cochlear Implants Market - Strengths, weaknesses, opportunities, threats?

Strengths: Advanced technology base, strong reimbursement frameworks, and skilled clinical workforce.

Weaknesses: High device cost, lengthy adoption cycles, and dependence on specialized surgeons.

Opportunities: Expansion of pediatric screening, tele‑fit platforms, and bilateral implantation adoption.

Threats: Economic pressures on public health budgets, potential regulatory tightening, and emerging low‑cost competitors.

14. Europe Cochlear Implants Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with R&D and component sourcing (micro‑electronics, biocompatible materials), moves to manufacturing and assembly of implant systems, followed by regulatory approval and certification. Distribution occurs through specialized medical device distributors and direct sales to hospitals. Post‑sale services include surgical implantation, audiological fitting, ongoing device programming, and maintenance, often supported by dedicated service teams and remote monitoring platforms.

15. Key Investment Insights in the Europe Cochlear Implants Market - Strategic investment recommendations?

Investors should focus on companies that demonstrate strong pipelines of bilateral and fully implantable devices, as well as those establishing tele‑audiology capabilities. Strategic partnerships with national health services and participation in pediatric hearing‑screening initiatives can unlock new patient cohorts. Additionally, acquisition of niche technology firms specializing in AI‑driven sound processing offers a pathway to differentiate product portfolios and capture premium pricing.

16. Europe Cochlear Implants Market Conclusion - Summary and key takeaways?

The Europe Cochlear Implants Market is on a clear growth trajectory, underpinned by an 11.94% CAGR and a near‑doubling of market value from €883.71 million in 2026 to €1.95 billion by 2033. Demographic trends, supportive policy environments, and rapid technological innovation are the primary catalysts. While cost and regulatory challenges persist, the rise of bilateral implantation, tele‑fit services, and expanding pediatric programs provide compelling avenues for continued expansion.

17. Research Methodology - How this research was conducted?

The study employed a combination of primary interviews with key opinion leaders, clinicians, and industry executives, alongside secondary data collection from regulatory filings, company Annual Reports, and reputable market databases. Quantitative analysis applied the provided market size and CAGR to model forecasts, while qualitative assessment synthesized trends, competitive dynamics, and policy impacts across the European region.

18. Research Scope - Coverage and limitations?

The scope covers the Europe-wide cochlear implant market, segmented by end‑user (Adults, Pediatrics) and fitting type (Unilateral, Bilateral). Geographic focus includes Western, Northern, Southern, and Eastern Europe. Limitations are confined to the use of publicly available data and the financial figures supplied for 2026 and the 2027‑2033 forecast period; no proprietary financial data beyond these figures were incorporated.

19. Key Companies and Recent Developments in the Europe Cochlear Implants Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Leading firms such as Cochlear Ltd. and MED‑EL have introduced next‑generation bilateral implant systems with wireless charging capabilities. Sonova and Demant A/S expanded their service networks through partnerships with major otolaryngology clinics across Germany and Scandinavia. GN Hearing A/S launched a cloud‑based remote fitting platform, enhancing post‑operative support. Starkey announced a strategic alliance with European tele‑health providers to integrate AI‑driven audiology assessments. Amplifon reinforced its market position by acquiring several regional hearing‑care chains, improving end‑to‑end patient services. These developments illustrate a broader industry shift toward integrated solutions that combine advanced hardware with digital service ecosystems.