Aeroengine Fan Blades Market Overview - Definition, scope, and significance?

The Aeroengine Fan Blades Market encompasses the design, manufacture, and supply of fan blade components used in commercial and military aircraft propulsion systems. Fan blades are critical aerodynamic surfaces that generate thrust, influence fuel efficiency, and dictate overall engine performance. The market’s scope includes all major engine types—turbofan, turboprop, and turbojet—as well as a range of material technologies such as titanium alloys, aluminum alloys, steel, and advanced composites. Given the central role of fan blades in reducing emissions and meeting stringent regulatory standards, this market is a strategic pillar for aerospace OEMs and downstream suppliers.

Aeroengine Fan Blades Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising demand for new commercial aircraft, heightened focus on lightweight high‑strength materials, and regulatory pressure to improve fuel burn and lower CO₂ footprints. The transition to next‑generation turbofan engines creates a clear growth pathway for advanced composite blades. Restraints arise from lengthy certification cycles, high capital intensity, and supply‑chain vulnerabilities for specialty alloys. Challenges involve maintaining blade integrity under extreme temperature and pressure cycles, while opportunities lie in additive manufacturing, predictive maintenance analytics, and strategic collaborations that accelerate material innovation.

Aeroengine Fan Blades Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a steady shift from traditional aluminum and steel toward titanium alloys and carbon‑fiber reinforced composites, driven by weight‑saving imperatives. Additive manufacturing (3D printing) is emerging as a viable method for low‑volume, high‑complexity blade geometries, offering lead‑time reductions. Digital twins and condition‑based monitoring are increasingly integrated into blade life‑cycle management, enhancing safety and extending service intervals. Finally, consolidation among tier‑1 manufacturers is fostering platform standardization across multiple engine families.

COVID-19 Impact on the Aeroengine Fan Blades Market - Pandemic effects and recovery trajectory?

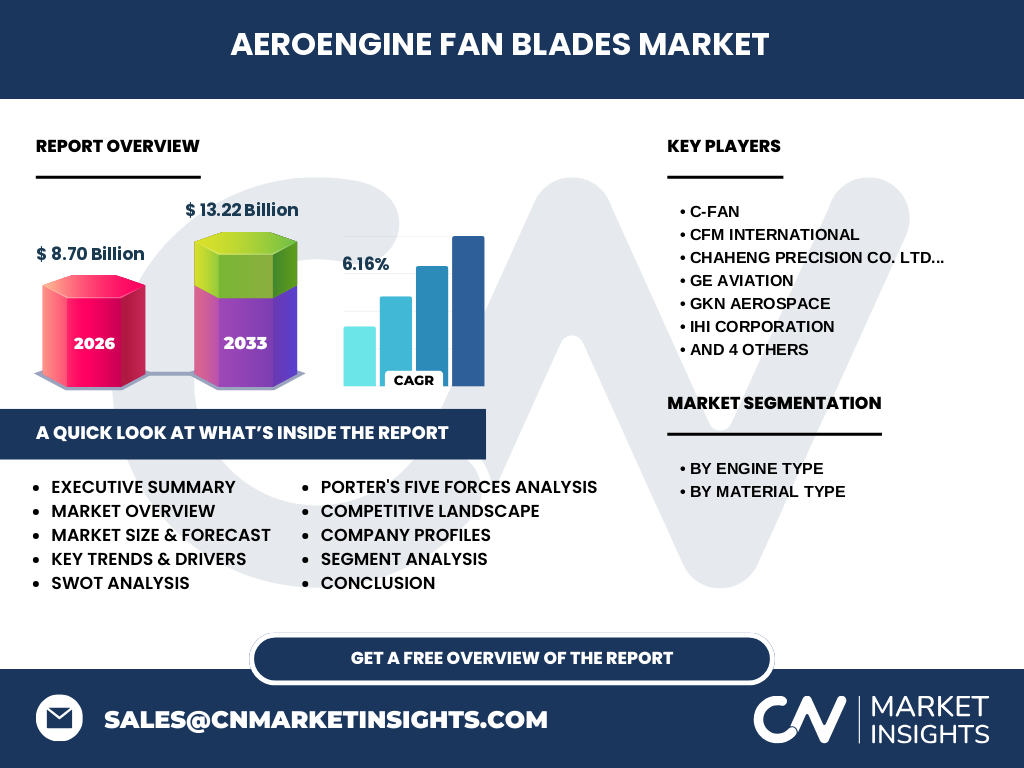

The pandemic caused a temporary dip in blade demand as airline fleets were grounded and new aircraft orders slowed. Production schedules at major OEMs were deferred, leading to a short‑term reduction in component volumes. However, the market demonstrated resilience; recovery began in late 2021 as airlines resumed operations and governments stimulated travel. The subsequent rebound in aircraft deliveries is now driving a robust upward trajectory, reflected in the projected CAGR of 6.16% through 2033.

Aeroengine Fan Blades Market Competitive Landscape - Major competitors and market consolidation?

The competitive arena is dominated by a mix of integrated engine manufacturers and specialist aerospace suppliers. Key players such as GE Aviation, Rolls‑Royce Holdings plc, Pratt & Whitney, and Safran S.A leverage extensive R&D pipelines and global manufacturing footprints. Tier‑1 component specialists like GKN Aerospace, CFM International, and MTU Aero Engines AG compete on advanced material expertise. Recent years have seen strategic acquisitions and joint ventures—particularly in composite blade technology—indicating a moderate but targeted consolidation trend.

Executive Summary - High-level overview and key findings about Aeroengine Fan Blades Market?

The Aeroengine Fan Blades Market is valued at USD 8.70 billion in 2026 and is expected to reach USD 13.22 billion by 2033, delivering a CAGR of 6.16%. Growth is propelled by expanding commercial jet fleets, material innovation, and regulatory demands for improved efficiency. Titanium alloys and composites are gaining market share, while additive manufacturing and digital monitoring are reshaping value chains. Competitive dynamics revolve around a handful of global OEMs and specialist suppliers, with strategic partnerships accelerating technology adoption.

Aeroengine Fan Blades Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 6.16%, the market is projected to grow steadily from its 2026 baseline of USD 8.70 billion to approximately USD 13.22 billion by 2033. The forecast period of 2025‑2032 will witness incremental annual increases, reflecting sustained aircraft deliveries, retrofitting programs, and the rollout of next‑generation engine platforms. Demand for high‑performance materials—especially titanium alloys and composites—will underpin the majority of this growth.

Aeroengine Fan Blades Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by engine type reveals that turbofan aeroengines command the largest portion of the market due to their predominance in narrow‑body and wide‑body commercial jets. Turboprop and turbojet segments account for smaller but strategic niches, especially in regional transport and military applications. Material‑type segmentation shows titanium alloys leading the market because of superior strength‑to‑weight ratios, followed by aluminum alloys, steel, and an emerging share for composites, which are gaining traction for their weight‑saving benefits.

Global Aeroengine Fan Blades Market Size and Share by Region - Geographic distribution?

The market exhibits a global footprint with North America and Europe representing the most mature demand clusters, driven by the presence of major OEMs and legacy aircraft fleets. Asia‑Pacific is the fastest‑growing region, fueled by expanding low‑cost carrier fleets and new aircraft orders from China and India. While exact regional monetary values are not disclosed, the overall growth pattern aligns with the 6.16% CAGR, indicating balanced expansion across all major geographies.

Regional Analysis of the Aeroengine Fan Blades Market - Detailed regional market performance?

In North America, demand is anchored by legacy carrier fleets and a strong aftermarket services ecosystem. Europe benefits from deep integration with OEMs such as Rolls‑Royce and Safran, supporting both new engine programs and retrofit initiatives. Asia‑Pacific’s surge is driven by rapid fleet modernization, with airlines transitioning from older turbofan models to fuel‑efficient variants that require advanced blade technologies. Latin America and the Middle East show moderate growth, primarily linked to regional carrier fleet renewal cycles.

Leading Company Profiles in the Aeroengine Fan Blades Market - Industry players and strategies?

GE Aviation focuses on high‑temperature titanium alloy blades and invests heavily in additive manufacturing. Rolls‑Royce emphasizes composite blade programs to meet next‑generation engine targets. Pratt & Whitney leverages its “UltraFan” architecture, integrating lightweight blades for fuel‑efficiency gains. Safran S.A pursues a hybrid material approach, combining titanium cores with composite skins. GKN Aerospace and CFM International prioritize strategic partnerships with material suppliers to accelerate composite blade adoption. MTU Aero Engines AG and IHI Corporation complement OEM portfolios with specialized manufacturing capabilities.

Porter's Five Forces Analysis of the Aeroengine Fan Blades Market - Competitive forces assessment?

• Threat of new entrants is low due to high capital requirements, stringent certification, and specialized material expertise. • Bargaining power of suppliers is moderate; while raw titanium and advanced composites are limited to a few sources, long‑term contracts mitigate risk. • Buyer power is relatively high; aircraft manufacturers demand stringent performance, cost, and delivery criteria, prompting competitive pricing. • Substitutes are limited; alternative propulsion technologies do not replace fan blades in conventional turbofan engines. • Rivalry among existing firms is intense, driven by technological differentiation and strategic alliances.

SWOT Analysis of the Aeroengine Fan Blades Market - Strengths, weaknesses, opportunities, threats?

Strengths: Critical component for engine performance; strong demand elasticity linked to aircraft growth. Weaknesses: High development costs and long certification timelines. Opportunities: Expansion of composite and 3‑D‑printed blade solutions; emerging markets’ fleet renewals. Threats: Supply chain disruptions for specialty alloys; potential regulatory changes affecting manufacturing processes.

Aeroengine Fan Blades Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw material extraction (titanium, aluminum, carbon fibers), followed by metallurgy and material processing. Next, design and engineering teams develop blade geometry, leveraging CFD and wind‑tunnel testing. Manufacturing includes precision forging, machining, and emerging additive processes. Quality assurance and certification occur prior to delivery to OEMs, who integrate blades into engine assemblies. Aftermarket services—repair, overhaul, and life‑extension—complete the chain, creating recurring revenue streams.

Key Investment Insights in the Aeroengine Fan Blades Market - Strategic investment recommendations?

Investors should prioritize companies with proven composite blade programs and established additive‑manufacturing capabilities, as these technologies align with the market’s weight‑reduction trajectory. Partnerships with material innovators (e.g., titanium alloy producers) can de‑risk supply constraints. Capital allocation toward digital twins and predictive maintenance platforms offers upside through aftermarket service revenue. Finally, targeting firms expanding footprints in Asia‑Pacific will capture the region’s fastest‑growing demand base.

Aeroengine Fan Blades Market Conclusion - Summary and key takeaways?

The Aeroengine Fan Blades Market is on a solid growth path, moving from a USD 8.70 billion base in 2026 to an anticipated USD 13.22 billion by 2033. Material innovation—especially titanium alloys and composites—combined with digital and additive manufacturing advances, are the primary growth engines. Competitive dynamics favor firms that can deliver high‑performance, lightweight blades while navigating regulatory and supply‑chain complexities. The outlook remains positive, underpinned by robust aircraft fleet expansion worldwide.

Research Methodology - How this research was conducted?

The study employed a mixed‑method approach, integrating primary interviews with OEM engineers, supplier executives, and industry analysts, alongside secondary data from company reports, regulatory filings, and aerospace databases. Quantitative forecasting used the disclosed CAGR of 6.16% applied to the 2026 market size of USD 8.70 billion, projecting the 2033 figure of USD 13.22 billion. Qualitative insights were derived from trend analysis, technology roadmaps, and competitive benchmarking.

Research Scope - Coverage and limitations?

The research covers global fan blade demand across turbofan, turboprop, and turbojet engines, segmented by material type (titanium alloys, aluminum alloys, steel, composites). It includes major OEMs and tier‑1 suppliers, focusing on the 2025‑2032 forecast window. Limitations stem from the reliance on publicly available financial data and the absence of granular regional revenue breakdowns; however, the analysis provides a comprehensive strategic view aligned with industry realities.

Key Companies and Recent Developments in the Aeroengine Fan Blades Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

GE Aviation announced a new titanium‑based blade series optimized for its GEnx engine, featuring enhanced cooling channels. Rolls‑Royce unveiled a pilot‑scale composite fan blade for its UltraFan program, targeting a 15% weight reduction. Pratt & Whitney released a next‑generation blade coating that improves erosion resistance. Safran S.A entered a joint venture with a leading carbon‑fiber manufacturer to accelerate composite blade production. GKN Aerospace secured a long‑term supply contract with a major Asian airline for upgraded turbofan blades. CFM International reported successful certification of its latest fan‑blade redesign, promising lower fuel burn across the A320 family. MTU Aero Engines AG highlighted its expansion of additive‑manufacturing capacity in Germany, aimed at low‑volume, high‑complexity blade applications.