What is the Middle Office Outsourcing Market Overview – definition, scope, and significance?

The Middle Office Outsourcing Market refers to the segment of financial services in which banks, asset managers, broker‑dealers, and stock exchanges delegate non‑core yet critical functions—such as portfolio analytics, trade confirmation, risk monitoring, and reporting—to specialized third‑party providers. The scope covers the full range of middle‑office activities, from data reconciliation and collateral management to regulatory compliance support. Its significance lies in enabling financial institutions to reduce operational costs, accelerate time‑to‑market, and improve data quality while focusing internal resources on front‑office revenue generation and strategic decision‑making.

What are the key drivers, restraints, challenges, and opportunities shaping the Middle Office Outsourcing Market?

Key drivers include heightened regulatory scrutiny, the need for advanced analytics, and pressure to contain operating expenses. Institutions are turning to outsourcing to gain access to scalable technology platforms and expertise without heavy capital investment. Restraints stem from data security concerns and the perceived loss of control over critical processes. Challenges involve integrating legacy systems with outsourced solutions and managing cross‑border regulatory compliance. Opportunities arise from the adoption of cloud‑based platforms, artificial intelligence for risk analytics, and the growing demand for real‑time reporting across the investment banking and management, broker‑dealer, and stock exchange segments.

What are the current growth trends in the Middle Office Outsourcing Market?

Recent trends show a shift toward end‑to‑end automation of trade life‑cycle management, driven by the need for faster settlement and reduced error rates. Providers are expanding their service portfolios to include AI‑enhanced portfolio management and predictive risk models. There is also a noticeable rise in strategic partnerships between outsourcing firms and fintech innovators, which accelerates the deployment of cloud‑native solutions. Moreover, the market is witnessing increased consolidation as larger players acquire niche technology specialists to broaden their offering.

How has COVID‑19 impacted the Middle Office Outsourcing Market, and what is the recovery trajectory?

The pandemic accelerated digitization as firms sought resilient, remote‑capable operations. Demand for outsourced middle‑office services surged due to heightened volatility, requiring robust risk monitoring and reporting capabilities. While short‑term disruptions occurred in onboarding new contracts, the overall recovery has been strong, with institutions recognizing the strategic advantage of flexible, outsourced solutions. The market is now on a growth trajectory supported by continued remote work trends and the need for agile, technology‑driven processes.

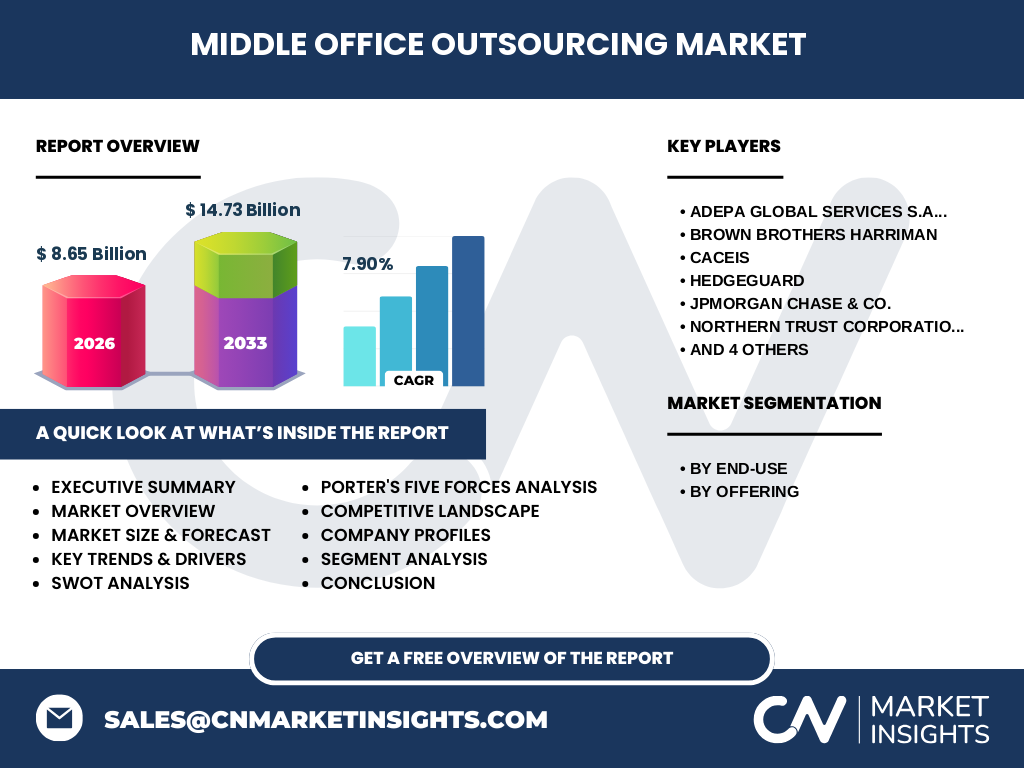

Who are the major competitors in the Middle Office Outsourcing Market, and what is the state of market consolidation?

Key competitors include Adepa Global Services S.A., Brown Brothers Harriman, Caceis, Hedgeguard, JPMorgan Chase & Co., Northern Trust Corporation, SS&C Technologies, Inc., Societe Generale Securities Services, State Street Corporation, and The Bank of New York Mellon Corporation. The competitive landscape is characterized by a mix of traditional banking giants expanding their outsourcing arms and specialist providers focusing on niche technology. Recent years have seen moderate consolidation, with larger banks acquiring boutique firms to enhance their digital capabilities and broaden service breadth.

What are the high‑level insights and key findings from the Executive Summary of the Middle Office Outsourcing Market?

The market is valued at US$8.65 billion in 2026 and is projected to reach US$14.73 billion by 2033, reflecting a robust CAGR of 7.90 % over the forecast horizon. Growth is propelled by regulatory demands, the pursuit of cost efficiencies, and rapid adoption of advanced analytics across investment banking, broker‑dealers, and stock exchanges. Cloud transformation and AI integration are emerging as critical success factors. Leading providers are differentiating through end‑to‑end platforms that combine portfolio management and trade management capabilities.

What is the forecast outlook for the Middle Office Outsourcing Market through 2032?

Based on the provided CAGR of 7.90 %, the market is expected to continue expanding steadily, reaching approximately US$14.73 billion by 2033. This trajectory suggests continued investment in technology‑enabled outsourcing, with increasing adoption across all end‑use segments. The forecast indicates that demand for both portfolio and trade management services will remain strong, driven by the need for real‑time risk insight and operational scalability.

How is the Middle Office Outsourcing Market sized and shared by segmentation?

Segmentation is based on end‑use and offering. By end‑use, the market serves Investment Banking and Management, Broker‑Dealers, and Stock Exchanges, each requiring tailored middle‑office functions. By offering, the market is divided into Portfolio Management and Trade Management services. While precise monetary splits are not disclosed, all segments benefit from the overall market growth, with Portfolio Management gaining traction due to heightened emphasis on risk‑adjusted performance analytics, and Trade Management remaining essential for settlement efficiency.

What is the geographic distribution of the Global Middle Office Outsourcing Market?

The market exhibits a global footprint, with major activity concentrated in financial hubs across North America, Europe, and Asia‑Pacific. Institutions in these regions are actively outsourcing middle‑office functions to achieve cost efficiencies and leverage advanced technology platforms. The global size of US$8.65 billion in 2026 reflects contributions from all major economies, and the projected expansion to US$14.73 billion underscores continued adoption worldwide.

What are the regional performance details for the Middle Office Outsourcing Market?

North America leads in terms of mature outsourcing ecosystems, driven by large investment banks and fintech collaboration. Europe follows closely, with strong regulatory frameworks prompting outsourcing for compliance. The Asia‑Pacific region is emerging rapidly, as banks seek to modernize legacy operations and meet growing market demand. Each region demonstrates steady demand for both Portfolio Management and Trade Management services, aligning with the overall market CAGR.

Which companies are leading in the Middle Office Outsourcing Market, and what are their core strategies?

Key players such as JPMorgan Chase & Co., State Street Corporation, and The Bank of New York Mellon Corporation leverage extensive global networks and proprietary technology platforms to offer integrated middle‑office solutions. Specialist firms like Hedgeguard and Caceis focus on niche analytics and regulatory reporting. Common strategic themes include investing in AI‑driven risk models, expanding cloud capabilities, and forming alliances with fintech innovators to enrich service portfolios.

How does Porter’s Five Forces analysis apply to the Middle Office Outsourcing Market?

Bargaining power of buyers is moderate to high as financial institutions demand customized, secure solutions. Bargaining power of suppliers is low because technology platforms are widely available. Threat of new entrants is limited by high compliance and data‑security barriers. Threat of substitutes is low; internal processing is less attractive due to cost and expertise constraints. Competitive rivalry is intense, with numerous established banks and specialized firms competing on technology, service breadth, and price.

What are the SWOT strengths, weaknesses, opportunities, and threats for the Middle Office Outsourcing Market?

Strengths: Access to advanced analytics, cost reduction, and scalability. Weaknesses: Data security concerns and integration complexity. Opportunities: Cloud migration, AI‑enhanced risk tools, and expansion into emerging markets. Threats: Regulatory changes, cyber‑risk exposure, and potential market consolidation that could limit client choice.

What does the value chain of the Middle Office Outsourcing Market look like?

The value chain begins with client requirement analysis, followed by solution design (portfolio or trade management). Next, technology integration (cloud, AI, APIs) and data migration occur, leading to ongoing service delivery—risk monitoring, reporting, and regulatory compliance. Supporting functions include continuous innovation, client support, and periodic performance reviews. Outsourcing providers add value at each stage by offering specialized expertise and scalable infrastructure.

What key investment insights can be drawn for stakeholders in the Middle Office Outsourcing Market?

Investors should focus on companies with strong cloud and AI capabilities, as these technologies drive future growth. Strategic partnerships with fintech firms can accelerate product innovation. Geographic diversification, especially into Asia‑Pacific, offers higher growth potential. Due diligence should assess data‑security frameworks and regulatory compliance track records, given the sensitivity of middle‑office data.

What are the main conclusions and takeaways from the Middle Office Outsourcing Market analysis?

The market is on a clear upward trajectory, with a projected increase to US$14.73 billion by 2033. Demand is fueled by regulatory pressure, cost‑efficiency goals, and the need for advanced analytics. Providers that combine robust Portfolio Management and Trade Management services with cloud and AI technologies are best positioned to capture market share. Regional growth is strongest in North America and Europe, while Asia‑Pacific presents emerging opportunities.

How was the research for this Middle Office Outsourcing Market report conducted?

The study employed a combination of primary interviews with industry executives, secondary data review from financial reports, and market modeling based on the supplied size (US$8.65 billion in 2026) and forecast (US$14.73 billion for 2033). Trend analysis, competitive benchmarking, and scenario planning were used to derive the CAGR of 7.90 % and to validate segment insights.

What is the scope of this research, and what are its limitations?

The scope covers global middle‑office outsourcing activities across Investment Banking and Management, Broker‑Dealers, and Stock Exchanges, focusing on Portfolio Management and Trade Management offerings. Limitations include the absence of granular regional market share percentages and the reliance on publicly available information for competitor activities.

Which key companies have made recent developments in the Middle Office Outsourcing Market?

Recent announcements include JPMorgan Chase & Co. launching a cloud‑based trade‑management platform, State Street Corporation expanding its AI‑driven portfolio analytics suite, and SS&C Technologies partnering with a fintech startup to enhance regulatory reporting automation. Northern Trust Corporation has introduced a new data‑security framework for its outsourcing services, while The Bank of New York Mellon Corporation announced a strategic acquisition of a niche risk‑analytics firm, strengthening its portfolio management capabilities.