1. What is the Biopolymer Packaging Market Overview – definition, scope, and significance?

The Biopolymer Packaging Market encompasses the production and application of packaging materials derived from renewable biological sources such as plant starches, cellulose, and microbial polymers. Its scope includes films, containers, trays, and flexible wraps used across food‑and‑beverage, cosmetics, personal care, and pharmaceutical sectors. The significance lies in offering a sustainable alternative to conventional petroleum‑based plastics, reducing carbon footprints, and meeting stricter regulatory and consumer demands for environmentally responsible packaging.

2. What are the market drivers, restraints, challenges, and opportunities?

Key drivers include increasing government mandates on single‑use plastic bans, rising consumer preference for eco‑friendly packaging, and expanding applications of biopolymers in high‑growth end‑use sectors. Restraints stem from higher production costs relative to traditional plastics and limited large‑scale recycling infrastructure. Challenges involve achieving performance parity—such as barrier properties and shelf life—with existing petro‑chemical solutions. Opportunities arise from advances in biotechnology that improve material properties, the emergence of circular economy models, and partnerships that enable cost‑effective scaling.

3. What growth trends are currently shaping the Biopolymer Packaging Market?

Current trends feature a shift toward compostable and biodegradable films, the integration of bio‑PE and bio‑PET into mainstream packaging lines, and the adoption of multilayer structures that combine biopolymers with barrier additives. Emerging trends include the use of microbial polyhydroxyalkanoates (PHAs) for premium applications, customization of polymer blends to meet specific functional requirements, and increasing investment in pilot facilities that demonstrate commercial viability.

4. How has COVID‑19 impacted the Biopolymer Packaging Market and what is the recovery trajectory?

The pandemic disrupted supply chains and temporarily reduced demand in hospitality‑related packaging, but it also accelerated e‑commerce growth, driving higher consumption of sustainable take‑out and delivery containers. Consumer awareness of waste issues increased, strengthening long‑term demand for biopolymers. Recovery is on a positive trajectory, with the market rebounding as manufacturers ramp up capacity and new contracts are secured across food, cosmetics, and pharma segments.

5. What does the competitive landscape look like and are there signs of consolidation?

The competitive landscape is characterized by a mix of large chemical conglomerates and specialized bioplastic innovators. Major players such as Arkema Group, BASF SE, The Dow Chemical Company, and NatureWorks LLC dominate through extensive R&D budgets and global distribution networks. Smaller innovators like Biome Bioplastics Limited and Cardia Bioplastics focus on niche material developments. Recent years have seen strategic acquisitions and joint ventures aimed at expanding product portfolios and geographic reach, indicating moderate consolidation.

6. Can you provide an executive summary with key findings?

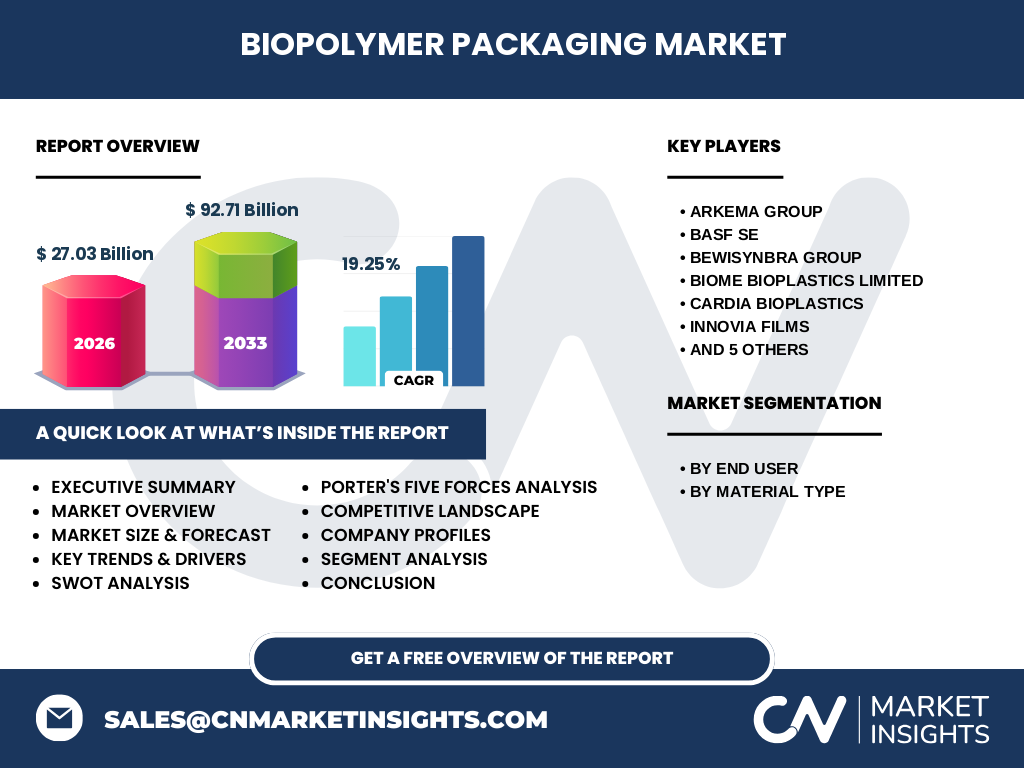

The Biopolymer Packaging Market is poised for rapid expansion, projected to reach 92.71 billion USD by 2033 with a CAGR of 19.25 % from 2027 to 2033. Growth is fueled by regulatory pressure, consumer sustainability preferences, and material‑innovation breakthroughs. Food‑and‑beverage remains the largest end‑user, while pharma and cosmetics offer strong tailwinds. Competitive intensity is increasing, prompting collaborations and technology licensing. Investment in scalable production and recycling infrastructure will be decisive for market leaders.

7. What are the market forecasts for 2025‑2032?

Based on the provided CAGR of 19.25 %, the market is expected to maintain robust upward momentum throughout the 2025‑2032 horizon. The 2026 baseline of 27.03 billion USD serves as a springboard, with cumulative growth driving the market toward the 2033 forecast of 92.71 billion USD. This trajectory reflects expanding adoption across all listed end‑use categories and continued material diversification.

8. How is the market sized and shared by segmentation?

Segmentation by end‑user reveals three primary categories: Food and Beverages, Cosmetic and Personal Care, and Pharmaceutical. By material type, the market includes Polylactides, Bio‑Polyethylene, Bio‑Polyethylene Terephthalate, Starch, Cellulose, PBAT, Polyhydroxyalkanoates, and Polybutylene succinate. While exact share percentages are not disclosed, each segment contributes to the overall market value, with polylactides and bio‑PE historically capturing the largest portions due to their widespread commercial availability.

9. What is the global market size and share by region?

The global Biopolymer Packaging Market is valued at 27.03 billion USD in 2026 and is projected to expand to 92.71 billion USD by 2033. Geographic distribution spans North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa. Each region exhibits varying adoption rates, with North America and Europe leading due to stringent regulations, while Asia‑Pacific shows the fastest growth driven by expanding manufacturing bases and rising consumer environmental awareness.

10. What does the regional analysis reveal about market performance?

North America benefits from strong policy frameworks and early‑stage consumer adoption, supporting higher per‑capita usage of biopolymer packaging. Europe’s circular‑economy initiatives and extended producer responsibility schemes further boost demand. Asia‑Pacific’s large food‑processing industry and cost‑sensitive market foster rapid scale‑up of bio‑PE and starch‑based solutions. Latin America and Middle East & Africa present emerging opportunities as local governments introduce waste‑reduction targets.

11. Which leading companies operate in this market and what are their strategies?

Key companies include Arkema Group, BASF SE, BEWiSynbra Group, Biome Bioplastics Limited, Cardia Bioplastics, Innovia Films, NatureWorks LLC, Plantic Technologies Limited, Spectra Packaging Ltd., The Dow Chemical Company, and United Biopolymers, S.A. Strategies range from expanding production capacity (e.g., NatureWorks’ new PLA plant) and securing long‑term supply contracts, to investing in R&D for new polymer blends (e.g., BASF’s bio‑PET initiatives). Partnerships with packaging converters and brand owners accelerate market penetration.

12. How does Porter’s Five Forces assess the market?

*Threat of new entrants* is moderate due to high capital requirements but lowered by advances in fermentation technology. *Bargaining power of suppliers* is relatively low as raw material feedstocks (e.g., corn, sugarcane) are widely available. *Bargaining power of buyers* is growing, with major consumer brands demanding sustainable solutions. *Threat of substitutes* remains low because biopolymers uniquely address biodegradability mandates. *Industry rivalry* is intense, driven by rapid innovation and price competition.

13. What are the SWOT insights for the Biopolymer Packaging Market?

Strengths: Renewable feedstock base, alignment with environmental regulations, and increasing consumer acceptance. Weaknesses: Higher cost structure and limited recycling streams. Opportunities: Technological breakthroughs in polymer performance, expansion into high‑value pharma packaging, and development of closed‑loop recycling. Threats: Potential policy reversals, volatility in agricultural commodity prices, and competition from advanced petro‑chemical recycling.

14. What does the value chain analysis reveal?

The value chain starts with feedstock cultivation (e.g., corn, sugarcane), proceeds to monomer synthesis, polymerization, and material processing into films or containers. Mid‑stream activities involve formulation of blends and additives to meet barrier and mechanical specifications. Downstream, packaging converters fabricate final products, which are then distributed to end‑users. Supporting services such as certification, waste‑management, and composting infrastructure add value and influence market adoption.

15. What key investment insights emerge for stakeholders?

Investors should prioritize companies with scalable production facilities and robust R&D pipelines, particularly those advancing PHAs and bio‑PET. Strategic bets on circular‑economy models—like take‑back schemes and industrial composting partnerships—can de‑risk long‑term demand. Geographic diversification into fast‑growing Asia‑Pacific markets offers upside, while collaborations with major brand owners secure volume contracts and enhance market credibility.

16. How can the market be concluded in a concise manner?

The Biopolymer Packaging Market is on a decisive growth trajectory, underpinned by regulatory pushes, consumer demand for sustainability, and rapid material innovation. With a projected market size of 92.71 billion USD by 2033, the sector presents compelling opportunities for manufacturers, investors, and brand owners willing to navigate cost challenges and develop integrated value‑chain solutions.

17. What research methodology was employed for this report?

The study combined primary interviews with industry experts, secondary data extraction from company filings, trade publications, and market databases. Quantitative forecasting applied the disclosed CAGR of 19.25 % to the 2026 baseline, while qualitative analysis synthesized trends, competitive moves, and policy impacts. Cross‑validation ensured consistency across segment and regional assessments.

18. What is the scope of the research and its limitations?

The research covers global biopolymer packaging applications across food‑and‑beverage, cosmetics, personal care, and pharmaceutical end‑users, and evaluates all listed material types. Limitations include the reliance on publicly available financial figures and the absence of granular market‑share percentages for individual segments or regions, which are reserved for the full proprietary report.

19. Which key companies have recent developments worth noting?

Recent announcements include NatureWorks’ expansion of its PLA production capacity, BASF’s launch of a bio‑PET pilot line, Arkema’s introduction of a high‑performance PBAT blend, and The Dow Chemical Company’s partnership with a major food‑service chain to trial compostable packaging. Innovia Films unveiled a new cellulose‑based film targeting cosmetics, while United Biopolymers, S.A. secured a strategic supply agreement with a leading pharmaceutical packaging provider.