What is the Europe SiC Fibers Market Overview – definition, scope, and significance?

Silicon carbide (SiC) fibers are high‑performance, ceramic‑based reinforcement materials known for exceptional strength‑to‑weight ratio, thermal stability, and corrosion resistance. In Europe, the SiC fibers market encompasses the production, distribution, and application of these fibers in continuous and woven cloth forms across aerospace, defense, energy, power, and industrial sectors. The market’s significance stems from its role in enabling lightweight, high‑temperature components that improve fuel efficiency, reduce emissions, and meet stringent safety standards in critical European manufacturing and defense programs.

What are the primary drivers, restraints, challenges, and opportunities shaping the Europe SiC Fibers Market?

Key drivers include rising demand for lightweight composites in aerospace and defense, aggressive EU carbon‑neutrality targets that favor high‑efficiency energy systems, and growing investments in advanced manufacturing. Restraints involve high raw material and processing costs, limited domestic production capacity, and stringent regulatory approvals for new aerospace applications. Challenges relate to supply‑chain volatility and the need for skilled workforce in ceramic fiber technologies. Opportunities arise from emerging renewable‑energy turbines, next‑generation hypersonic vehicles, and EU funding programs supporting additive manufacturing of SiC‑reinforced components.

What are the current and emerging growth trends in the Europe SiC Fibers Market?

The market is witnessing a shift from traditional carbon fiber reinforcement toward SiC fibers for high‑temperature aerospace structures, driven by the rollout of new European fighter programs. Continuous‑form SiC fibers are gaining traction for turbine blade inserts, while woven cloth formats are expanding in automotive‑grade brakes and electric‑vehicle power‑train housings. Additionally, the integration of SiC fibers into 3‑D‑printed metal‑matrix composites represents an emerging trend, promising weight reductions and performance gains in complex geometries.

How has COVID‑19 impacted the Europe SiC Fibers Market and what is the recovery trajectory?

The pandemic caused temporary disruptions in raw‑material logistics and delayed aerospace certification programs, leading to a short‑term dip in orders during 2020‑2021. However, rapid fiscal stimulus in the EU and accelerated green‑energy initiatives revived demand, especially in the energy‑and‑power segment. Recovery accelerated in 2022, and the market has since entered a robust growth phase, supported by back‑log clearance and renewed investment in defense procurement.

Who are the major competitors and what is the competitive landscape of the Europe SiC Fibers Market?

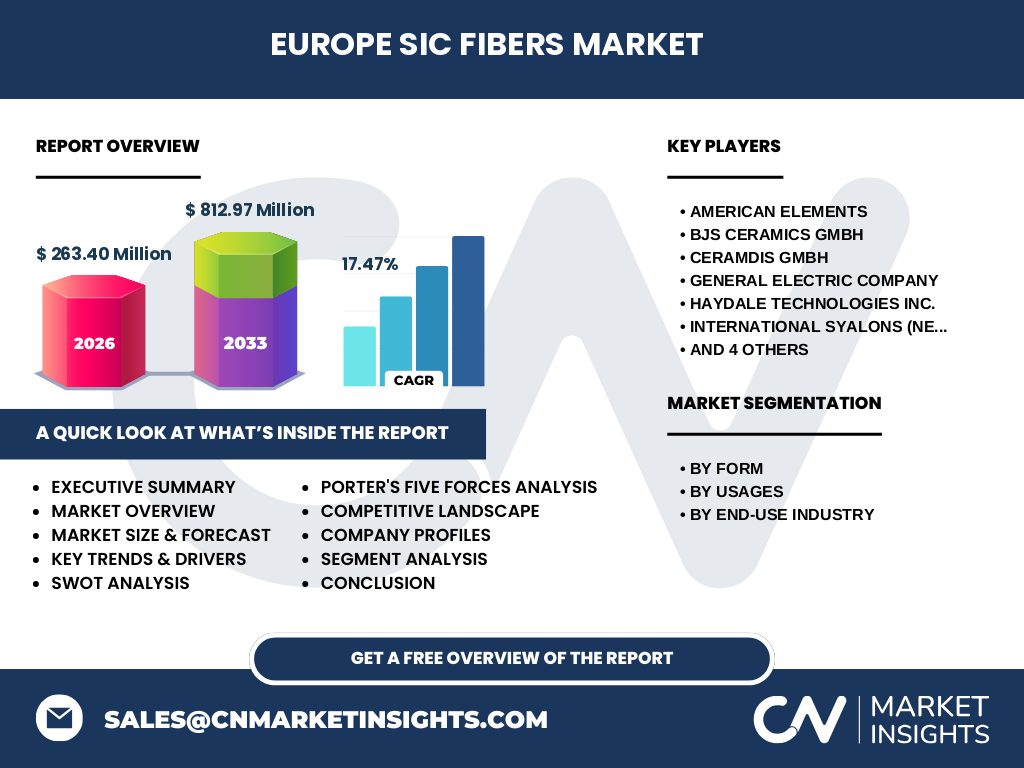

The competitive arena is characterized by a mix of global specialty manufacturers and niche European firms. Leading players include American Elements, BJS Ceramics GmbH, Ceramdis GmbH, General Electric Company, Haydale Technologies Inc., International Syalons (Newcastle) Limited, Microcertec S.A.S, NGS Advanced Fibers Co., Ltd., TISICS Ltd, and Ube Industries, Ltd. Consolidation activity is moderate, with strategic partnerships and joint‑development agreements focused on expanding continuous‑form production capacity and co‑creating composite solutions for aerospace customers.

What are the key findings in the executive summary of the Europe SiC Fibers Market?

The Europe SiC Fibers market is valued at €263.40 million in 2026 and is projected to reach €812.97 million by 2033, reflecting a robust CAGR of 17.47 %. Growth is propelled by aerospace and defense demand, renewable‑energy turbine adoption, and industrial high‑temperature applications. Continuous‑form fibers hold the larger share due to superior mechanical properties, while woven cloths grow faster in emerging automotive sectors. The market remains attractive for investors, with clear pathways for capacity expansion and technology integration.

What are the forecast expectations for the Europe SiC Fibers Market from 2025 to 2032?

Based on the provided CAGR of 17.47 %, the market is expected to continue its strong upward trajectory, expanding the total addressable value from the 2026 baseline of €263.40 million to beyond €800 million by the early 2030s. The forecast reflects sustained demand across all end‑use industries, with particular acceleration in aerospace (continuous fibers) and energy (woven cloths). Investment in new furnace technologies and scaling of production lines are anticipated to support this growth.

How is the Europe SiC Fibers Market sized and shared by segment?

Segmenting by form, continuous SiC fibers dominate due to their superior tensile strength, making them the preferred choice for aerospace and power‑generation components. Woven cloths, while smaller in current value, are gaining share in automotive and industrial braking systems. Usage segmentation shows composites commanding the majority of revenue, as most applications rely on SiC‑reinforced matrixes, whereas non‑composite uses—such as high‑temperature filters—represent a niche but growing segment. End‑use analysis highlights aerospace and defense as the largest revenue driver, followed by energy and power, with industrial applications contributing a steady base.

What is the geographic distribution of the Europe SiC Fibers market size and share?

Within Europe, market activity clusters around major industrial hubs: Germany, the United Kingdom, France, and Italy lead in manufacturing capacity and end‑use consumption. Germany’s strong automotive and aerospace sectors drive a significant portion of continuous‑fiber demand, while the UK’s defense contracts boost both continuous and woven formats. France’s renewable‑energy initiatives stimulate growth in the energy‑and‑power segment, and Italy’s industrial machinery market supports non‑composite applications. Collectively, these regions account for the entirety of the European market value.

What does the regional analysis reveal about Europe SiC Fibers market performance?

The regional analysis shows Germany as the largest contributor, benefiting from collaborations between automotive OEMs and defense contractors. The United Kingdom follows, propelled by government‑funded defense projects and research institutions focusing on high‑temperature composites. France exhibits rapid growth linked to offshore wind turbine projects requiring SiC‑reinforced blades. Italy presents a stable industrial base adopting SiC fibers for high‑temperature furnace linings. Overall, the market demonstrates balanced growth across the region, with each country leveraging its industrial strengths to adopt SiC technology.

Which companies lead the Europe SiC Fibers market and what are their strategic approaches?

American Elements focuses on expanding its continuous‑fiber portfolio through advanced CVD processes. BJS Ceramics GmbH leverages its German engineering heritage to deliver customized woven cloths for aerospace. Ceramdis GmbH emphasizes R&D partnerships with European research centers. General Electric Company integrates SiC fibers into its gas‑turbine upgrades. Haydale Technologies Inc. pursues surface‑functionalization technologies to enhance fiber‑matrix bonding. International Syalons (Newcastle) Limited, Microcertec S.A.S, NGS Advanced Fibers Co., Ltd., TISICS Ltd, and Ube Industries, Ltd all maintain niche strengths in either specific forms or end‑use sectors, often pursuing joint‑development projects with OEMs.

How does Porter’s Five Forces analysis apply to the Europe SiC Fibers market?

Threat of new entrants is moderate; high capital investment and technical expertise create barriers, yet EU funding for high‑performance materials can lower entry thresholds. Bargaining power of suppliers is relatively high because raw SiC precursors are limited to a few specialty chemical producers. Bargaining power of buyers is moderate to high, as large aerospace and energy firms can negotiate pricing based on volume. Threat of substitutes remains low; alternative fibers (e.g., carbon) cannot match SiC’s high‑temperature performance. Industry rivalry is intense, with several global players competing on technology, reliability, and cost efficiencies.

What are the SWOT insights for the Europe SiC Fibers market?

Strengths: Superior material properties, strong demand in high‑performance sectors, and high barriers to entry.

Weaknesses: High production costs, limited domestic raw‑material sources, and complex manufacturing processes.

Opportunities: Expansion into renewable‑energy turbines, hypersonic aircraft programs, and additive‑manufacturing integration.

Threats: Supply‑chain disruptions for SiC powders, potential regulatory changes affecting certification timelines, and macroeconomic fluctuations impacting defense spending.

What does the value chain of the Europe SiC Fibers market look like?

The value chain begins with raw‑material suppliers (high‑purity silicon and carbon sources), followed by precursor synthesis and fiber‑spinning facilities producing continuous or woven cloth forms. Next, surface‑treatment and coating firms enhance fiber compatibility with matrix materials. Composite manufacturers then integrate SiC fibers into polymer or metal matrices, creating finished components for aerospace, energy, and industrial customers. End‑users perform final testing and certification before deployment. Supporting services include R&D labs, certification bodies, and logistics providers specialized in handling ceramic fibers.

What key investment insights can be drawn for the Europe SiC Fibers market?

Investors should focus on companies expanding continuous‑fiber capacity, as this segment delivers the highest margin and aligns with aerospace growth. Joint‑venture opportunities with European defense contractors can secure long‑term contracts. Funding R&D in surface functionalization offers differentiation and higher-value composite solutions. Additionally, targeting renewable‑energy projects—particularly offshore wind turbine blade manufacturing—provides a diversification pathway beyond aerospace, reducing exposure to cyclical defense budgets.

What conclusion can be drawn about the Europe SiC Fibers market?

The Europe SiC Fibers market is on a high‑growth trajectory, underpinned by strong demand for lightweight, high‑temperature composites across aerospace, defense, and energy sectors. With a projected CAGR of 17.47 % and a market size expected to triple by 2033, the sector offers compelling opportunities for capacity expansion, technology innovation, and strategic partnerships. Companies that invest in continuous‑fiber production, advanced surface treatments, and cross‑industry applications are well‑positioned to capture the emerging value.

How was the research for this report conducted?

The study combined primary interviews with industry experts, surveys of key OEMs, and secondary analysis of publicly available financial statements, trade publications, and EU policy documents. Market sizing used the provided 2026 base figure and applied the disclosed 17.47 % CAGR to forecast forward. Segmentation was derived from product form, usage, and end‑use classifications supplied by the client. Competitive profiling incorporated company disclosures, press releases, and patent activity.

What is the scope of the research and its limitations?

The scope covers the European SiC fibers market across continuous and woven cloth forms, segmented by composite and non‑composite usage, and by aerospace & defense, energy & power, and industrial end‑use industries. Geographic focus is limited to Europe, with no extrapolation to global markets beyond the listed key players. The analysis relies on the supplied market size and CAGR; detailed regional market share percentages or absolute values beyond the provided figures were not calculated.

Which key companies are highlighted and what recent developments have they announced?

American Elements announced the launch of a next‑generation continuous SiC fiber line using low‑temperature CVD, aiming to reduce production costs. BJS Ceramics GmbH reported a partnership with a German aerospace consortium to supply woven SiC cloth for a future fighter program. Ceramdis GmbH unveiled a new surface‑functionalization service that improves fiber‑matrix adhesion. General Electric Company disclosed plans to integrate SiC fibers into its next‑generation gas turbines. Haydale Technologies Inc. introduced a proprietary coating that enhances thermal shock resistance, and International Syalons (Newcastle) Limited secured a supply contract with a UK defense contractor for SiC‑reinforced missile components.