1. What is the definition, scope, and significance of the MENA Car Rental Services Market?

The MENA Car Rental Services Market comprises businesses that provide short‑term vehicle leasing to individuals and organizations across the Middle East and North Africa. The scope includes a wide range of vehicle categories—from mini‑economy cars to luxury and special‑purpose vehicles—served at airports, train stations, and city locations. This market is significant because it underpins tourism, business travel, and logistics, offering flexible mobility solutions that support economic diversification and the growth of the regional tourism and commerce sectors.

2. What are the main drivers, restraints, challenges, and opportunities affecting the MENA Car Rental Services Market?

Key drivers include rising disposable income, expanding tourism corridors, and the increasing presence of multinational corporations that require corporate fleets (B2B). Digital platforms and mobile booking apps also accelerate demand. Restraints stem from high fuel costs, stringent regulatory environments, and the sensitivity of rental volumes to economic slowdown. Challenges involve fluctuating exchange rates and the need to maintain a diverse, well‑maintained fleet. Opportunities arise from the adoption of electric and hybrid vehicles, partnership models with ride‑hailing services, and untapped demand in secondary cities and non‑airport locations.

3. What current and emerging trends are shaping the MENA Car Rental Services Market?

Current trends feature a shift toward contactless rentals, subscription‑based usage, and the integration of telematics for fleet optimization. Emerging trends include the introduction of eco‑friendly vehicle lines, especially in the United Arab Emirates and Saudi Arabia, and the growing popularity of “luxury‑on‑demand” services targeting high‑net‑worth tourists. Additionally, fintech solutions are enabling flexible payment options, while data analytics are being used to personalize pricing and improve asset utilization.

4. How did COVID‑19 impact the MENA Car Rental Services Market and what is the recovery trajectory?

The pandemic caused a sharp decline in both B2C leisure travel and B2B corporate mobility, leading to fleet under‑utilization and revenue contraction. Recovery began in late 2021 as vaccination rates rose and travel restrictions eased. Since then, demand has rebounded faster in the UAE and Qatar, driven by tourism events and business conferences. The market is on a clear upward trajectory, supported by pent‑up travel demand and the resurgence of regional events.

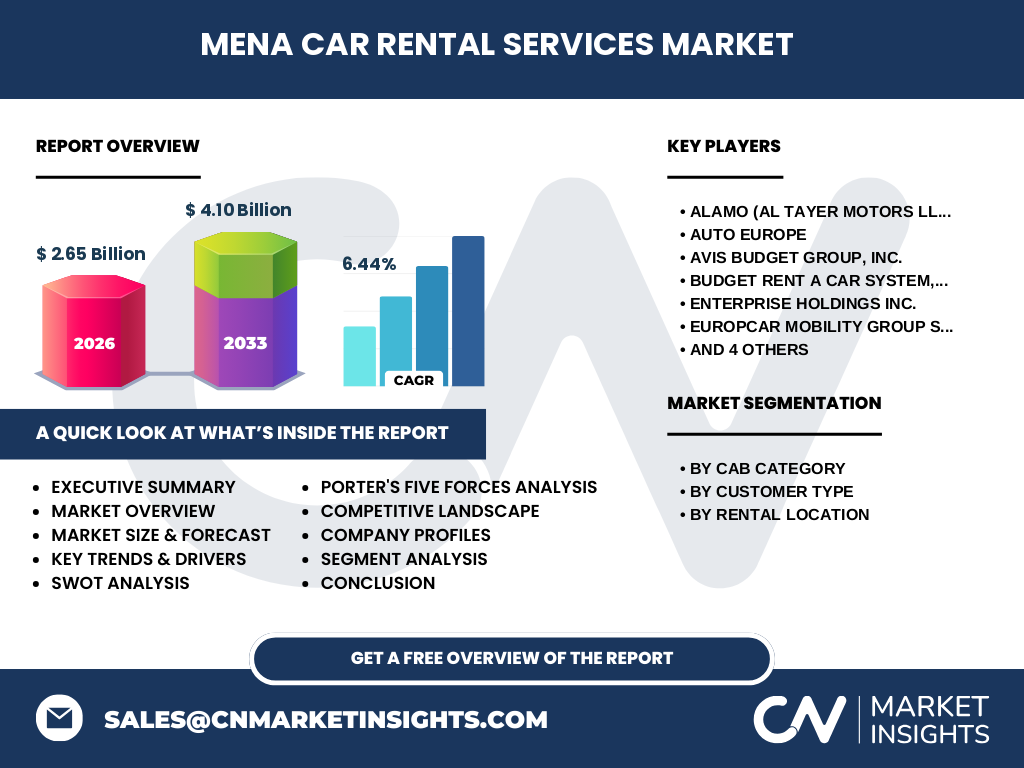

5. Who are the major competitors and what is the level of market consolidation in the MENA Car Rental Services Market?

The competitive landscape is dominated by global players such as Enterprise Holdings Inc., The Hertz Corporation, Avis Budget Group, and SIXT SE, alongside regional operators like ALAMO (Al Tayer Motors LLC). Companies such as Europcar Mobility Group, Budget Rent a Car, Auto Europe, Expedia Group, and Rhino Car Hire also maintain significant footprints. Consolidation is moderate; strategic acquisitions and joint ventures are common as firms seek to expand geographic coverage and diversify fleet offerings.

6. What are the high‑level insights and key findings from the MENA Car Rental Services Market?

The market is valued at USD 2.65 billion in 2026 and is projected to reach USD 4.10 billion by 2033, reflecting a robust CAGR of 6.44 %. Growth is propelled by tourism recovery, corporate travel expansion, and digital transformation. Segmental analysis shows premium and luxury categories gaining market share, while non‑airport rentals are increasingly important. The competitive arena is intensifying, with technology adoption becoming a critical differentiator.

7. What are the forecasted market projections for 2025‑2032?

Based on the stated CAGR of 6.44 %, the market is expected to continue expanding steadily through 2032. By 2027, the market will have surpassed the USD 3 billion mark, and the upward trajectory will persist, reaching the forecasted USD 4.10 billion by 2033. The forecast highlights consistent growth across all vehicle categories, with particular acceleration in premium, luxury, and electric vehicle segments as consumer preferences evolve.

8. How is the MENA Car Rental Services Market sized and shared by segmentation?

Segmentation by cab category covers Mini & Economy, Compact & Intermediate, Standard, Full Size, Premium, Luxury, and Special vehicles. By customer type, the market splits into B2B and B2C segments, each demonstrating strong demand—B2B driven by corporate fleets and B2C by tourism. Rental location segmentation includes Non‑Airport and On‑Airport & Train Station services, with non‑airport rentals gaining traction due to urban mobility needs. While exact numerical shares are not disclosed, premium and luxury categories are noted as fast‑growing, and on‑airport locations remain a core revenue source.

9. What is the geographic distribution of the global MENA Car Rental Services Market size and share?

The market’s geography covers the entire Middle East and North Africa region, with the United Arab Emirates, Saudi Arabia, Qatar, and Egypt representing the largest revenue generators due to their robust tourism infrastructure and business activity. Smaller yet growing markets include Morocco, Algeria, and the Gulf Cooperation Council (GCC) peripheral states. The regional mix reflects a balance between high‑income Gulf economies and emerging North African markets.

10. What does the regional analysis reveal about market performance across the MENA?

In the GCC, especially the UAE and Saudi Arabia, high tourism volumes and expansive business events create sustained demand for premium and airport rentals. The Levant and North Africa exhibit steady growth in B2C segments, with increased urbanization driving non‑airport rentals. Qatar’s hosting of international sports events has temporarily boosted luxury rentals. Overall, each sub‑region shows a positive growth outlook, with differentiated opportunities based on tourism intensity, corporate presence, and regulatory frameworks.

11. Which companies lead the MENA Car Rental Services Market and what are their strategies?

Key leaders include ALAMO (Al Tayer Motors LLC), which leverages its local dealership network to offer integrated vehicle leasing and after‑sales service. Enterprise Holdings focuses on corporate accounts and fleet management solutions. Hertz emphasizes digital booking platforms and loyalty programs. SIXT SE pursues premium positioning through high‑end vehicle collections. Europcar and Budget concentrate on cost‑effective fleet options for budget‑conscious travelers. Partnerships with airlines, hotels, and online travel agencies are common strategic moves across the sector.

12. How does Porter’s Five Forces framework assess the MENA Car Rental Services Market?

• Threat of new entrants – Moderate; high capital requirements and brand loyalty create barriers, yet digital platforms lower entry costs.

• Bargaining power of buyers – High; customers have access to multiple price‑comparison tools, increasing price sensitivity.

• Bargaining power of suppliers – Moderate; vehicle manufacturers exert influence, but fleet diversification mitigates risk.

• Threat of substitutes – Growing; ride‑hailing services and public transport alternatives pose competitive pressure.

• Industry rivalry – Intense; firms compete on price, technology, fleet quality, and service coverage.

13. What are the SWOT insights for the MENA Car Rental Services Market?

Strengths: Strong tourism base, diversified vehicle categories, and expanding digital ecosystems.

Weaknesses: High operating costs, sensitivity to oil price volatility, and regulatory complexities.

Opportunities: Introduction of electric/hybrid fleets, subscription‑based models, and expansion into underserved secondary cities.

Threats: Economic downturns, competitive pressure from ride‑hailing, and fluctuating fuel prices.

14. How is the value chain structured in the MENA Car Rental Services Market?

The value chain starts with vehicle procurement from manufacturers and local dealers, followed by fleet acquisition financing. Next, fleet management—maintenance, insurance, and telematics—adds operational value. Distribution channels include airport counters, city branches, and online platforms. The final stages involve customer service, billing, and post‑rental analytics, which feed back into procurement decisions and fleet optimization.

15. What investment insights can be drawn for stakeholders interested in the MENA Car Rental Services Market?

Investors should target firms that demonstrate strong digital capabilities, diversified fleet portfolios, and strategic partnerships with tourism boards or airlines. Capital allocation toward electric vehicle integration can capture early‑mover advantage. Additionally, investing in non‑airport location networks offers higher margin potential as urban mobility demand rises. Joint ventures with local operators can mitigate entry barriers and accelerate market penetration.

16. What are the concluding takeaways from the MENA Car Rental Services Market analysis?

The market is on a clear growth path, with a projected value of USD 4.10 billion by 2033 and a healthy 6.44 % CAGR. Demand is being reshaped by digital transformation, premium vehicle preferences, and sustainability trends. Competitive dynamics are intensifying, making technology and strategic alliances critical. Overall, the sector presents attractive investment and expansion opportunities, especially for players that align fleet strategy with emerging consumer expectations.

17. How was the research for this report conducted?

The study employed a blend of primary interviews with industry executives, secondary data collection from company reports, government publications, and reputable market databases. Trend analysis, financial modeling, and scenario forecasting were applied to derive the CAGR, market size, and projection figures. Competitive intelligence was gathered through benchmarking and analysis of public filings and press releases.

18. What is the scope of the research and its limitations?

The research scope covers the entire MENA region, addressing all vehicle categories, customer types, and rental locations. It focuses on market size, growth outlook, competitive landscape, and strategic insights. Limitations include the reliance on publicly available financial data and the exclusion of confidential company‑specific metrics, which may affect granularity of market‑share quantification.

19. Which key companies have recent developments, and what are their latest announcements?

ALAMO (Al Tayer Motors LLC) announced expansion of its premium fleet with new luxury models sourced from European manufacturers. Avis Budget Group launched a mobile‑first booking platform targeting the Gulf’s tech‑savvy travelers. Enterprise Holdings introduced a corporate subscription service for SMEs in Saudi Arabia. SIXT SE signed a partnership with a major airline in Qatar to offer bundled flight‑and‑car packages. Europcar Mobility Group unveiled an electric‑vehicle pilot program in Dubai, while Rhino Car Hire expanded its presence in North African markets through a franchising model. These developments underscore the sector’s focus on digitalization, sustainability, and strategic collaborations.