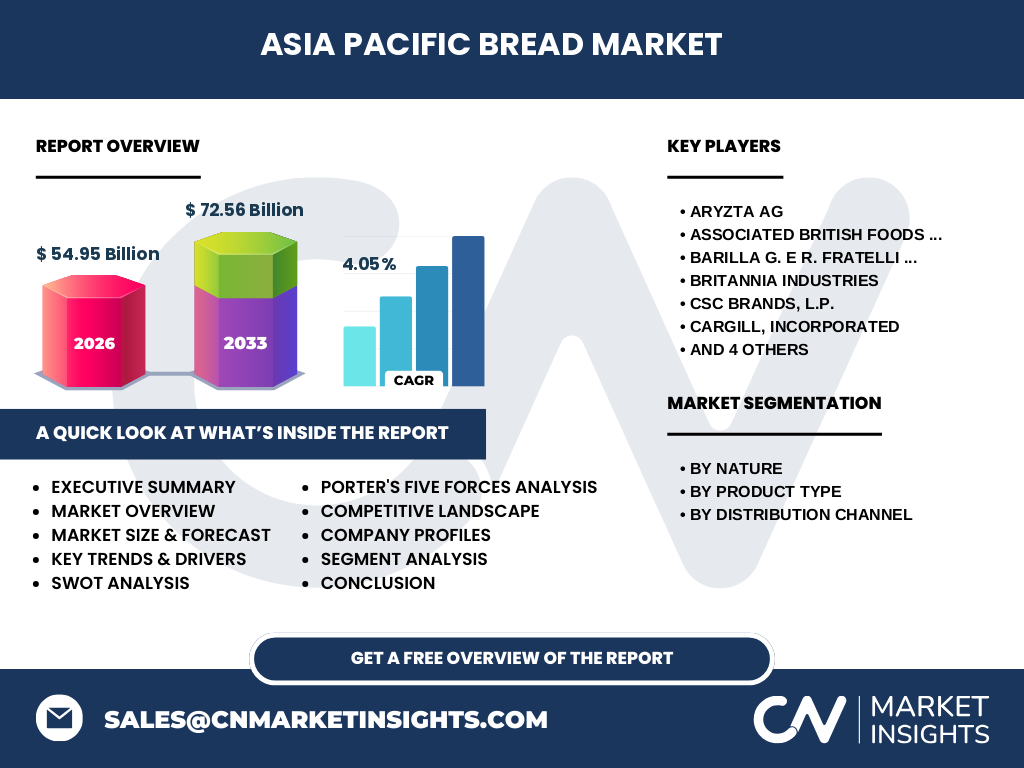

1. Asia Pacific Bread Market Overview – Definition, scope, and significance?

The Asia Pacific Bread Market encompasses the production, distribution, and consumption of bakery breads across the Asia Pacific region. It includes a broad range of product types—from traditional loaves and baguettes to specialty breads such as ciabatta and burger buns—served through multiple distribution channels including hyper‑markets, convenience stores, and online platforms. The market is defined by two primary nature categories: conventional and organic breads, reflecting consumer interest in both classic and health‑oriented offerings. With a 2026 valuation of US$54.95 billion, the sector represents a critical component of the region’s broader food‑processing industry, supporting agricultural supply chains, retail employment, and dietary trends across diverse economies.

2. Asia Pacific Bread Market Drivers, Restraints, Challenges, and Opportunities – Key growth factors and obstacles?

Drivers include rising urbanisation, expanding middle‑class incomes, and increasing demand for convenience foods, which boost consumption of ready‑to‑eat bread products. Health awareness stimulates growth of the organic segment, while the proliferation of modern retail formats expands shelf space for premium breads. Restraints involve volatile raw‑material costs (wheat, oil, and sugar) and stringent food‑safety regulations that can raise compliance expenses. Challenges arise from intense competition among multinational and local bakeries, leading to price pressure and the need for continuous product innovation. Opportunities are found in digital commerce—online channels are rapidly gaining market share—and in niche categories such as high‑protein or gluten‑free breads, which cater to evolving dietary preferences.

3. Asia Pacific Bread Market Growth Trends – Current and emerging trends shaping the market?

Key trends include the shift toward clean‑label and organic breads, driven by consumer desire for minimally processed foods. There is also a noticeable rise in artisan‑style offerings, such as ciabatta and sourdough, especially in metropolitan areas. Multi‑grain and fortified breads are gaining traction as functional foods. In distribution, e‑commerce platforms are becoming a primary purchase route for younger consumers, prompting bakeries to develop click‑and‑collect and home‑delivery solutions. Additionally, sustainability initiatives—such as waste‑reduction packaging and locally sourced ingredients—are influencing brand positioning.

4. COVID-19 Impact on the Asia Pacific Bread Market – Pandemic effects and recovery trajectory?

The COVID‑19 pandemic initially disrupted supply chains and forced temporary closures of bakeries, leading to short‑term declines in on‑premise sales. However, heightened at‑home consumption and the acceleration of online grocery shopping generated a rebound that outpaced pre‑pandemic levels. By 2022, the market had recovered, and the CAGR of 4.05 % reflects a robust post‑COVID growth trajectory, supported by continued consumer confidence and the permanent adoption of digital purchasing habits.

5. Asia Pacific Bread Market Competitive Landscape – Major competitors and market consolidation?

The competitive arena features a mix of global giants and strong regional players. Leading companies such as Aryzta AG, Associated British Foods plc, Barilla G. e R. Fratelli S.p.A, Britannia Industries, CSC Brands, Cargill, Finsbury Food Group, Fuji Baking Group, Goodman Fielder, and Premier Foods Group dominate across multiple segments. Recent years have seen strategic mergers and acquisitions aimed at expanding product portfolios and geographic reach, especially in high‑growth markets like China, India, and Australia. Consolidation is further driven by the need to achieve economies of scale in procurement and distribution.

6. Executive Summary – High-level overview and key findings about Asia Pacific Bread Market?

The Asia Pacific Bread Market is a US$54.95 billion industry in 2026, projected to reach US$72.56 billion by 2033, growing at a 4.05 % CAGR. Growth is propelled by urban consumer demand for convenience, health‑focused organic breads, and expanding online sales channels. While raw‑material volatility and regulatory compliance pose challenges, opportunities lie in product innovation, digital distribution, and sustainability. The market is highly fragmented but increasingly consolidated through strategic M&A among leading multinational bakeries.

7. Asia Pacific Bread Market Forecast – Projections for 2025‑2032 period?

Based on the supplied forecast, the market value is expected to climb from the 2026 base of US$54.95 billion to US$72.56 billion by the end of the 2027‑2033 horizon. This reflects steady expansion across all product categories, with particularly strong growth anticipated in the organic and premium‑artisan segments, as well as in online distribution channels, which are expected to capture an increasing share of total sales.

8. Asia Pacific Bread Market Size and Share by Segmentation – Breakdown by segment?

Segmentation is structured along three dimensions:

Nature: Conventional breads retain the largest volume share, while organic breads are experiencing higher growth rates due to health‑conscious consumer demand.

Product Type: Loaves dominate the category, followed by sandwich bread, burger buns, and rolls. Specialty items such as baguettes, ciabatta, and artisanal breads are gaining momentum in urban markets.

Distribution Channel: Hypermarkets and supermarkets remain the primary outlet, but convenience and retail stores are expanding rapidly. Online sales have shown the fastest CAGR, reflecting the shift toward digital shopping.

9. Global Asia Pacific Bread Market Size and Share by Region – Geographic distribution?

The Asia Pacific region accounts for the majority of global bread consumption, led by economies such as China, India, Japan, South Korea, and Australia. While exact regional monetary shares are not disclosed, the overall market size of US$54.95 billion in 2026 underscores the region’s dominant position within the worldwide bakery landscape.

10. Regional Analysis of the Asia Pacific Bread Market – Detailed regional market performance?

East Asia (China, Japan, South Korea): High urban density and sophisticated retail networks drive strong demand for both conventional and premium breads. South Asia (India, Bangladesh, Vietnam): Rapid income growth fuels consumption of affordable loaves and expanding snack‑type breads like burger buns. Southeast Asia (Indonesia, Malaysia, Philippines): Convenience stores and online platforms are key growth engines, with a rising appetite for organic and health‑focused breads. Australia & New Zealand: Mature markets focused on artisan and gluten‑free segments, with an emphasis on sustainability and local sourcing.

11. Leading Company Profiles in the Asia Pacific Bread Market – Industry players and strategies?

Aryzta AG: Focuses on premium and specialty breads, leveraging global supply chains and strategic partnerships to enter new markets.

Associated British Foods plc: Utilises its extensive brand portfolio to capture both mass‑market and niche segments, emphasizing product diversification.

Barilla G. e R. Fratelli S.p.A: Expands organic and whole‑grain lines, targeting health‑conscious consumers through innovative packaging.

Britannia Industries: Strong presence in South Asia, driving growth through localized flavors and aggressive retail distribution.

CSC Brands, L.P.: Concentrates on value‑added convenience breads, supported by a robust e‑commerce fulfillment network.

Cargill, Incorporated: Leverages raw‑material expertise to ensure cost‑stable supply for large‑scale manufacturers.

Finsbury Food Group Plc: Invests in bakery automation to improve productivity and product consistency.

Fuji Baking Group: Specialises in Japanese‑style breads, integrating traditional recipes with modern processing.

Goodman Fielder: Dominates the Australasian market with a focus on sustainability and locally sourced ingredients.

Premier Foods Group Limited: Pursues brand extensions into organic and functional breads to meet emerging consumer trends.

12. Porter’s Five Forces Analysis of the Asia Pacific Bread Market – Competitive forces assessment?

Threat of New Entrants: Moderate – High capital requirements for production facilities and distribution networks create barriers, yet niche artisanal bakeries can enter via small‑scale operations.

Bargaining Power of Suppliers: Moderate – Dependence on wheat and other commodities gives suppliers some leverage, mitigated by large players’ ability to source globally.

Bargaining Power of Buyers: High – Retailers and large‑scale consumers demand competitive pricing and consistent quality, pressing manufacturers to innovate and optimise costs.

Threat of Substitutes: Low to moderate – While alternative snacks exist, bread remains a staple, especially in urban diets, limiting substitution risk.

Rivalry Among Existing Competitors: Intense – Numerous multinational and local brands compete across price, quality, and innovation dimensions, driving continual product differentiation.

13. SWOT Analysis of the Asia Pacific Bread Market – Strengths, weaknesses, opportunities, threats?

Strengths: Large and growing consumer base, diversified product portfolio, strong distribution networks.

Weaknesses: Sensitivity to raw‑material price fluctuations, complex regulatory environment, reliance on traditional retail channels in some markets.

Opportunities: Expansion of organic and functional breads, growth of online sales, development of sustainable packaging, penetration into under‑served rural areas.

Threats: Intensifying price competition, potential trade restrictions on wheat imports, health trends that could shift consumers away from refined‑flour breads.

14. Asia Pacific Bread Market Value Chain Analysis – Industry structure and value flow?

The value chain begins with agricultural production (wheat, rye, barley) followed by ingredient sourcing (yeast, fats, additives). Next, manufacturing—including mixing, proofing, baking, and slicing—adds value, with many firms adopting automation to enhance efficiency. Packaging and logistics ensure product integrity and timely delivery to distribution points. The distribution layer comprises hypermarkets, convenience stores, and increasingly, online platforms that handle last‑mile delivery. Finally, retail and consumer interaction completes the chain, where branding, promotions, and in‑store placement influence purchase decisions.

15. Key Investment Insights in the Asia Pacific Bread Market – Strategic investment recommendations?

Investors should prioritize companies with strong e‑commerce capabilities and organic product lines, as these segments exhibit the fastest growth. Acquiring or partnering with regional bakeries that possess localized flavor expertise can accelerate market entry. Funding sustainability initiatives—such as eco‑friendly packaging and waste‑reduction technologies—offers differentiation and aligns with consumer expectations. Lastly, monitoring raw‑material supply contracts can hedge against price volatility and protect margins.

16. Asia Pacific Bread Market Conclusion – Summary and key takeaways?

The Asia Pacific Bread Market is poised for steady expansion, moving from US$54.95 billion in 2026 to US$72.56 billion by 2033, supported by urbanisation, health trends, and digital commerce. While raw‑material costs and competitive intensity pose challenges, opportunities abound in organic, premium, and online channels. Strategic focus on innovation, sustainability, and supply‑chain resilience will be essential for companies seeking to capture market share.

17. Research Methodology – How this research was conducted?

The study employed a mixed‑method approach, combining primary interviews with industry executives, secondary data extraction from company reports, trade publications, and governmental statistics, and quantitative modeling to project market size and growth. Segmentation analysis used product‑type, nature, and channel dimensions, while competitive mapping relied on revenue estimates and strategic initiatives disclosed by the listed key players.

18. Research Scope – Coverage and limitations?

The scope covers the entire Asia Pacific region, inclusive of East, South, and Southeast Asian economies, as well as Australia and New Zealand. It addresses conventional and organic breads across all major product categories and distribution channels. Limitations stem from the unavailability of granular regional revenue breakdowns; therefore, the analysis relies on aggregate figures and trend extrapolation.

19. Key Companies and Recent Developments in the Asia Pacific Bread Market – Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent developments include Aryzta AG’s launch of a gluten‑free artisan line in Japan, Associated British Foods plc forming a joint venture with an Indian retail chain to expand its sandwich‑bread portfolio, Barilla introducing a high‑protein organic loaf in Australia, and Britannia Industries rolling out a fortified breakfast‑bread range across South‑Asia. CSC Brands has upgraded its online fulfillment centres to accelerate home delivery, while Cargill signed long‑term wheat‑supply contracts to stabilise input costs. Finsbury Food Group announced a sustainability partnership to develop biodegradable packaging, and Goodman Fielder acquired a boutique bakery in New Zealand to strengthen its premium segment. These activities underscore a market-wide focus on health, convenience, and environmental responsibility.