1. Asia Pacific Cancer Tissue Diagnostics Market Overview - Definition, scope, and significance?

The Asia Pacific Cancer Tissue Diagnostics market encompasses technologies and services used to analyze cancerous tissue samples for accurate diagnosis, prognosis, and therapeutic decision‑making. It includes immunohistochemical (IHC) tests and in situ hybridization (ISH) tests that detect protein expression and genetic alterations directly within tissue sections. The scope covers laboratory reagents, automated platforms, digital pathology solutions, and associated services delivered to hospitals, diagnostic labs, and research institutions across the region. Its significance lies in enabling personalized oncology care, improving treatment outcomes, and supporting clinical trial enrollment, thereby driving broader healthcare system efficiency and cost containment.

2. Asia Pacific Cancer Tissue Diagnostics Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising cancer incidence, expanding middle‑class populations with increased health spending, and strong government initiatives promoting early detection. The adoption of targeted therapies fuels demand for precise tissue‑based biomarker testing. Restraints stem from high upfront costs of automated platforms and variability in reimbursement policies across countries. Challenges involve limited skilled pathologists in some markets and fragmented regulatory frameworks. Opportunities arise from the integration of digital pathology, AI‑assisted interpretation, and the rollout of portable IHC/ISH solutions that can serve remote or under‑served areas.

3. Asia Pacific Cancer Tissue Diagnostics Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a steady shift from manual staining toward fully automated IHC and ISH workflows, driven by the need for higher throughput and reproducibility. Emerging trends include multiplex IHC panels that allow simultaneous detection of several biomarkers, and RNA‑based ISH assays that complement DNA testing. The region is also witnessing growing collaborations between diagnostics firms and oncology drug developers to co‑develop companion diagnostics. Finally, tele‑pathology platforms are gaining traction, enabling expert review across borders.

4. COVID-19 Impact on the Asia Pacific Cancer Tissue Diagnostics Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic initially disrupted elective cancer surgeries and biopsy collections, leading to a temporary dip in test volumes. However, the crisis accelerated the adoption of remote diagnostic services and digital pathology, as labs sought to maintain continuity while minimizing physical contact. Post‑pandemic, demand rebounded strongly, supported by delayed diagnoses and heightened awareness of health screening. The market is now on a clear recovery trajectory, with growth projected to outpace pre‑COVID levels.

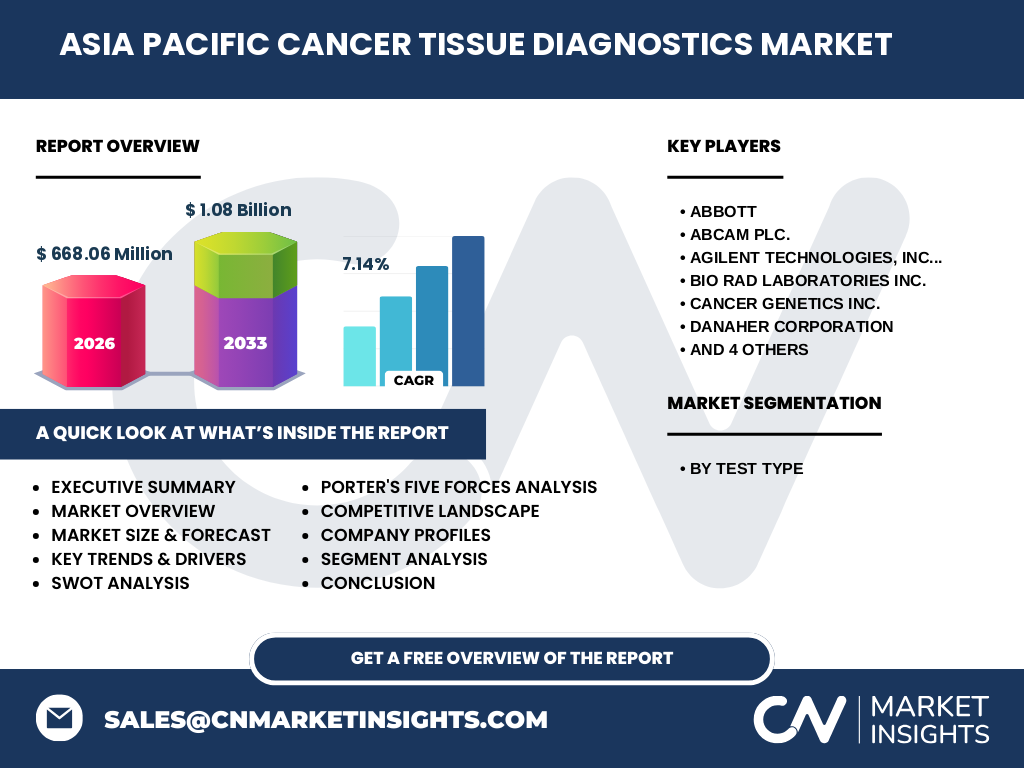

5. Asia Pacific Cancer Tissue Diagnostics Market Competitive Landscape - Major competitors and market consolidation?

The competitive environment is defined by a mix of global giants and specialized niche players. Leading companies such as Abbott, Agilent Technologies, Danaher Corporation, F. Hoffmann‑La Roche Ltd, Merck KGaA (Sigma‑Aldrich), Thermo Fisher Scientific, Bio‑Rad Laboratories, Abcam plc., Cancer Genetics Inc., and Enzo Life Sciences are actively expanding their IHC/ISH portfolios. Recent years have seen strategic acquisitions—e.g., large platform providers acquiring niche antibody developers—to broaden assay offerings and strengthen end‑to‑end solutions, contributing to moderate consolidation in the segment.

6. Executive Summary - High-level overview and key findings about Asia Pacific Cancer Tissue Diagnostics Market?

The Asia Pacific Cancer Tissue Diagnostics market is valued at USD 668.06 million in 2026 and is projected to reach USD 1.08 billion by 2033, delivering a CAGR of 7.14 % over the forecast horizon. Growth is propelled by rising cancer prevalence, government emphasis on early detection, and the expanding use of targeted therapies that require precise biomarker identification. While cost and skill gaps pose challenges, advances in automation, multiplex testing, and digital pathology create substantial upside. The competitive field is led by ten major firms that are investing heavily in innovation and strategic partnerships.

7. Asia Pacific Cancer Tissue Diagnostics Market Forecast - Projections for 2025‑2032 period?

Based on the indicated CAGR of 7.14 %, the market is expected to maintain a robust upward trajectory through 2032. The forecast reflects continued expansion of hospital networks, rising per‑capita health expenditures, and the rollout of national cancer screening programs across key economies such as China, Japan, South Korea, Australia, and India. Incremental adoption of next‑generation IHC and ISH assays—especially multiplex panels—will sustain demand, while the penetration of AI‑driven pathology workflows will enhance efficiency and drive higher test volumes.

8. Asia Pacific Cancer Tissue Diagnostics Market Size and Share by Segmentation - Breakdown by Test Type?

The market is segmented into two primary test types: Immunohistochemical (IHC) Tests and In Situ Hybridization (ISH) Tests. IHC remains the larger share owing to its broader application across solid tumors for protein expression profiling. ISH, while smaller, is gaining momentum due to its ability to detect gene amplifications and translocations, which are critical for newer targeted therapies. Both segments benefit from parallel growth in automation and multiplex capabilities, reinforcing the overall market expansion.

9. Global Asia Pacific Cancer Tissue Diagnostics Market Size and Share by Region - Geographic distribution?

Within the Asia Pacific landscape, market activity clusters in East Asia (China, Japan, South Korea) and the Australia‑New Zealand sub‑region, which together account for the majority of the 2026 market value of USD 668.06 million. South‑East Asia, led by Singapore, Malaysia, and Thailand, contributes a growing share driven by government‑backed cancer initiatives. The region’s collective share underscores its role as the primary growth engine for the global cancer tissue diagnostics industry.

10. Regional Analysis of the Asia Pacific Cancer Tissue Diagnostics Market - Detailed regional market performance?

China dominates the regional market due to its large patient pool, extensive network of tertiary hospitals, and supportive regulatory reforms that facilitate faster diagnostic approvals. Japan follows with high per‑test spending and strong private‑sector adoption of automated platforms. South Korea distinguishes itself through early adoption of digital pathology and AI integration. Australia and New Zealand benefit from mature healthcare systems and high reimbursement rates, leading to premium test utilization. Emerging economies such as India and Indonesia are expanding rapidly, supported by public‑private partnerships aimed at scaling cancer screening infrastructure.

11. Leading Company Profiles in the Asia Pacific Cancer Tissue Diagnostics Market - Industry players and strategies?

Key players include:

• Abbott – focuses on integrated IHC platforms and broad antibody libraries.

• Agilent Technologies – leverages its genomic expertise to offer combined DNA/RNA ISH solutions.

• Danaher Corporation – expands through its subsidiary Bio‑Rad, emphasizing high‑throughput automated staining.

• Roche – provides fully validated companion diagnostic kits aligned with its oncology drugs.

• Thermo Fisher Scientific – offers comprehensive assay kits and next‑generation multiplex panels.

These companies pursue strategies such as R&D investment in multiplex biomarkers, strategic alliances with pharma firms, and geographic expansion via local distribution networks.

12. Porter's Five Forces Analysis of the Asia Pacific Cancer Tissue Diagnostics Market - Competitive forces assessment?

Threat of New Entrants: Moderate. High capital requirements and regulatory hurdles limit newcomers, but niche biotech firms can enter via specialized antibody or probe development.

Bargaining Power of Suppliers: Low to moderate. Reagents are commoditized, though unique antibody patents can give certain suppliers leverage.

Bargaining Power of Buyers: Growing. Large hospital groups negotiate volume discounts, pressuring pricing.

Threat of Substitutes: Low. Alternative diagnostic modalities (e.g., liquid biopsy) complement rather than replace tissue testing.

Industry Rivalry: High. Ten major players compete on technology, assay breadth, and service support, driving continuous innovation and occasional consolidation.

13. SWOT Analysis of the Asia Pacific Cancer Tissue Diagnostics Market - Strengths, weaknesses, opportunities, threats?

Strengths: Robust demand driven by cancer burden; mature technology base; strong pipeline of multiplex assays.

Weaknesses: High cost of automation; shortage of skilled pathologists in some markets.

Opportunities: Expansion of AI‑enabled digital pathology; rise of companion diagnostics linked to emerging targeted therapies; untapped markets in South‑East Asia.

Threats: Potential regulatory tightening; price pressure from payers; disruptive technologies such as liquid biopsy that may shift testing preferences.

14. Asia Pacific Cancer Tissue Diagnostics Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with upstream raw material suppliers (antibodies, probes, reagents), proceeds to manufacturers of diagnostic platforms and kits, then to distributors and regional service providers. Laboratories and hospitals constitute the downstream segment, performing the actual testing and generating clinical reports. Post‑analytical services, including data management, AI interpretation, and tele‑pathology, add further value. Collaboration between platform vendors and software firms enhances the end‑to‑end solution, creating a tightly integrated chain.

15. Key Investment Insights in the Asia Pacific Cancer Tissue Diagnostics Market - Strategic investment recommendations?

Investors should focus on companies that combine robust assay portfolios with automation and digital pathology capabilities, as these are positioned to capture the shift toward high‑throughput, AI‑augmented diagnostics. Partnerships with oncology drug developers for companion diagnostics represent a high‑value growth avenue. Additionally, targeting emerging markets through localized manufacturing or joint ventures can accelerate revenue diversification. Monitoring regulatory developments and reimbursement trends will be essential for risk mitigation.

16. Asia Pacific Cancer Tissue Diagnostics Market Conclusion - Summary and key takeaways?

The Asia Pacific Cancer Tissue Diagnostics market is on a clear growth path, underpinned by a 7.14 % CAGR and an expansion from USD 668.06 million in 2026 to USD 1.08 billion by 2033. Drivers such as rising cancer prevalence, government screening programs, and the need for precise biomarker data are strong. While cost and talent gaps pose challenges, technological advances in automation, multiplex testing, and AI present compelling opportunities. Leading firms are consolidating and innovating, making the sector attractive for strategic investment.

17. Research Methodology - How this research was conducted?

The study employed a mixed‑method approach, combining primary interviews with key opinion leaders, laboratory managers, and vendor executives across the Asia Pacific region, with secondary data from industry reports, company filings, and peer‑reviewed publications. Market sizing utilized a bottom‑up approach, aggregating revenue from major product categories and adjusting for regional pricing differentials. Forecasting applied a compound annual growth rate (CAGR) of 7.14 % derived from historical trends and projected adoption rates of emerging technologies.

18. Research Scope - Coverage and limitations?

Scope includes the IHC and ISH test segments within the Asia Pacific geography, covering major economies and emerging markets. The analysis spans the period 2025‑2032, with a focus on market size, segmentation, competitive dynamics, and growth drivers. Limitations are inherent to the reliance on publicly disclosed financials and the absence of granular regional revenue breakdowns beyond the aggregate figures provided. Nonetheless, the findings present a comprehensive view of market direction.

19. Key Companies and Recent Developments in the Asia Pacific Cancer Tissue Diagnostics Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent activities include Abbott’s launch of a next‑generation automated IHC staining system designed for high‑volume labs in China and Japan. Agilent announced a collaboration with a leading Japanese pharma company to co‑develop an ISH assay for HER2‑amplified gastric cancer. Danaher’s Bio‑Rad introduced a multiplex IHC kit covering PD‑L1, Ki‑67, and EGFR, targeting clinical trials in South‑East Asia. Roche expanded its companion diagnostic portfolio with a newly FDA‑cleared IHC test for KRAS G12C, aligning with its targeted therapy pipeline. Thermo Fisher unveiled an AI‑integrated digital pathology platform that enables remote review and quantitative scoring, currently being piloted in Australian cancer centers. These developments illustrate the strategic emphasis on automation, multiplexing, and partnership‑driven innovation across the market.