1. Europe RTLS for Healthcare Market Overview – Definition, scope, and significance?

Real‑time locating systems (RTLS) for healthcare in Europe refer to the integrated set of technologies—such as RFID, Wi‑Fi, Bluetooth, GPS and Ultra‑Wideband (UWB)—that enable the continuous, real‑time tracking of assets, patients, staff and environmental conditions within medical facilities. The scope spans hospitals, clinics, senior‑living communities and related healthcare infrastructures, covering applications from asset inventory to patient safety and workflow automation. The significance of RTLS lies in its ability to improve operational efficiency, reduce loss of high‑value equipment, enhance patient outcomes through better monitoring, and support compliance with stringent regulatory standards across the European healthcare sector.

2. Europe RTLS for Healthcare Market Drivers, Restraints, Challenges, and Opportunities – Key growth factors and obstacles?

Key drivers include rising pressure on healthcare budgets, increasing demand for patient‑centred care, and the need for tighter infection‑control measures, all of which push hospitals to adopt automation solutions. The expansion of telehealth and the growing prevalence of chronic diseases further stimulate demand for precise asset and personnel tracking. Primary restraints involve high upfront capital costs and concerns over data privacy under GDPR. Challenges stem from integration complexity with legacy hospital information systems and the variability of technological standards across European countries. Opportunities arise from the ongoing rollout of 5G networks, which can enhance bandwidth for Wi‑Fi and Bluetooth solutions, and from government incentives promoting digital transformation in healthcare.

3. Europe RTLS for Healthcare Market Growth Trends – Current and emerging trends shaping the market?

Current trends highlight a shift from simple RFID tag‑based tracking toward hybrid solutions that combine Wi‑Fi, Bluetooth Low Energy (BLE) and UWB to deliver higher accuracy and richer data sets. Artificial intelligence and analytics are increasingly being layered on top of RTLS data to predict equipment utilization and optimize staff allocation. Emerging trends include the integration of RTLS with electronic health records (EHR) to create seamless patient journeys, and the use of battery‑free, chip‑enabled RFID for sterile environments. Furthermore, sustainability concerns are driving demand for low‑power, long‑life sensor technologies.

4. COVID‑19 Impact on the Europe RTLS for Healthcare Market – Pandemic effects and recovery trajectory?

The COVID‑19 pandemic accelerated adoption of RTLS as hospitals sought real‑time visibility of personal protective equipment (PPE), ventilators and mobile isolation units. Contact‑less tracking helped reduce staff exposure and improve quarantine compliance. Although initial procurement slowed during the first lockdowns due to budget constraints, the recovery has been robust, with many facilities prioritizing RTLS in post‑pandemic resilience plans. The market is now experiencing a rebound driven by heightened awareness of infection control and an increased focus on operational agility.

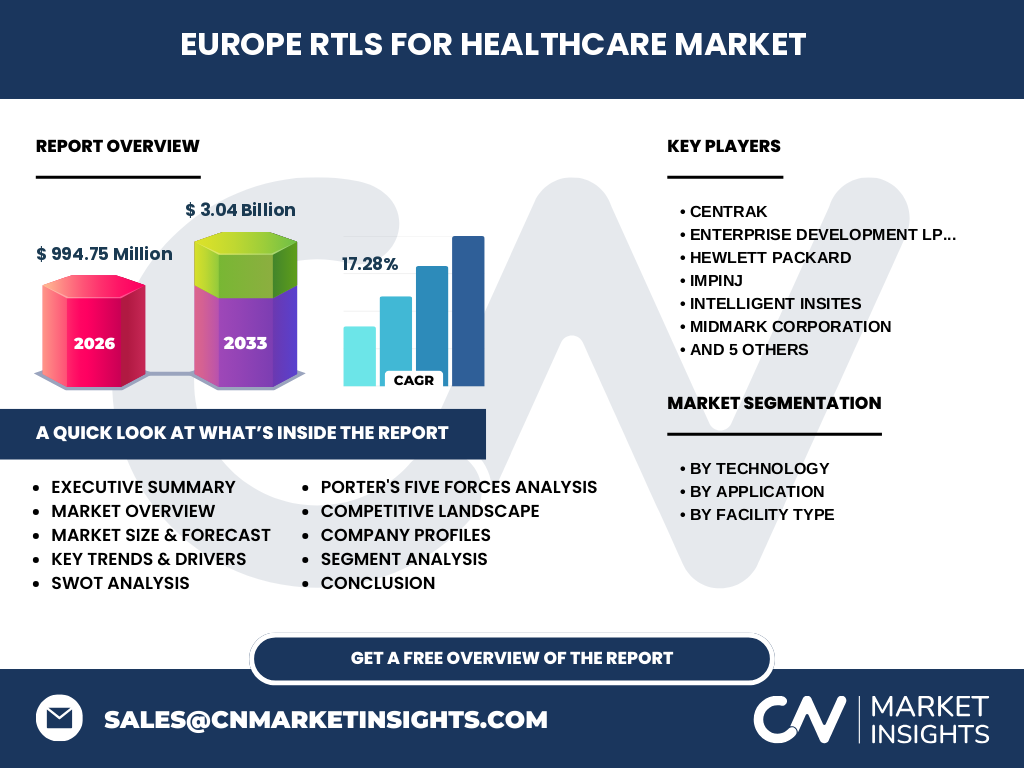

5. Europe RTLS for Healthcare Market Competitive Landscape – Major competitors and market consolidation?

The competitive arena is populated by a mix of specialized vendors and large technology conglomerates. Key players include Centrak, Enterprise Development LP (Aruba), Hewlett Packard, IMPINJ, Intelligent Insites, Midmark Corporation, Sanitag, Sonitor Technologies, Stanley Healthcare, Teletracking Technologies, Inc., and Zebra Technologies Corp. Recent years have seen strategic partnerships—such as collaborations between RFID specialists and cloud‑service providers—to enhance end‑to‑end solutions. While no major mergers have reshaped the market dramatically, the landscape reflects steady consolidation through joint ventures and technology licensing agreements aimed at broadening portfolio coverage across the five core technology segments.

6. Executive Summary – High‑level overview and key findings about Europe RTLS for Healthcare Market?

The Europe RTLS for Healthcare market is valued at €994.75 million in 2026 and is projected to reach €3.04 billion by 2033, delivering a robust CAGR of 17.28 %. Growth is propelled by cost‑containment pressures, patient‑safety imperatives and the digital‑health momentum accelerated by COVID‑19. RFID remains the dominant technology, yet Wi‑Fi, Bluetooth and UWB are gaining rapid traction. Asset tracking holds the largest application share, while patient and staff monitoring shows the fastest growth. Hospitals dominate the facility type segment, with senior‑living facilities emerging as a secondary growth driver. The market is competitive yet fragmented, offering ample room for innovative entrants and strategic collaborations.

7. Europe RTLS for Healthcare Market Forecast – Projections for 2025‑2032 period?

Based on the disclosed CAGR of 17.28 %, the market is expected to continue expanding at a double‑digit pace through 2032. By 2027, the market size will approach €1.2 billion, crossing the €2 billion threshold by 2030, and culminating near €3 billion by 2033. Growth will be strongest in regions with mature healthcare infrastructure and strong governmental support for digital health, notably Western and Northern Europe. Investment in AI‑enabled analytics and integration with emerging 5G networks will further accelerate adoption rates across all segments.

8. Europe RTLS for Healthcare Market Size and Share by Segmentation – Breakdown by segment?

Segmentation by technology distributes market demand across RFID, Wi‑Fi, Bluetooth, GPS and UWB, with RFID accounting for the largest share due to its proven reliability in sterile environments. Wi‑Fi and Bluetooth are expanding quickly as hospitals adopt IoT‑centric strategies, while GPS is limited to outdoor and campus‑wide tracking. UWB, recognized for centimeter‑level precision, is emerging in high‑acuity areas such as operating rooms. Application‑wise, inventory and asset tracking dominate, followed by patient and staff tracking, which is experiencing the fastest compound growth. Facility‑type analysis shows hospitals hold the bulk of market spend, while senior‑living facilities are projected to increase their share as the aging population expands.

9. Global Europe RTLS for Healthcare Market Size and Share by Region – Geographic distribution?

Europe represents a substantial portion of the global RTLS for healthcare market, anchored by well‑funded public health systems and a strong regulatory framework encouraging technology adoption. While specific regional percentages are not disclosed, the market’s €994.75 million valuation in 2026 underscores Europe’s leading role, with growth expectations outpacing many other regions due to coordinated digital‑health initiatives across the EU.

10. Regional Analysis of the Europe RTLS for Healthcare Market – Detailed regional market performance?

Western Europe, encompassing Germany, France, the United Kingdom and the Benelux nations, leads in deployment intensity, driven by high hospital density and proactive government funding. Northern Europe, including Scandinavia, shows strong interest in UWB and AI‑driven analytics for patient safety. Southern Europe exhibits steady growth, focusing on RFID‑based asset management to curb operational costs. Eastern European markets are emerging, with early adopters leveraging cost‑effective Bluetooth solutions to modernize legacy facilities.

11. Leading Company Profiles in the Europe RTLS for Healthcare Market – Industry players and strategies?

Key companies such as Centrak and Zebra Technologies provide end‑to‑end RFID platforms with robust tag ecosystems. Hewlett Packard leverages its enterprise networking strengths to integrate Wi‑Fi‑based RTLS with hospital IT infrastructures. IMPINJ and Sonitor Technologies focus on UWB and Bluetooth solutions respectively, emphasizing high‑accuracy location data for critical care zones. Stanley Healthcare and Teletracking Technologies specialize in patient‑flow analytics, combining sensor data with workflow software. These firms pursue strategies that include expanding service layers, forming alliances with EHR vendors, and investing in AI‑enabled data platforms to differentiate their offerings.

12. Porter's Five Forces Analysis of the Europe RTLS for Healthcare Market – Competitive forces assessment?

Threat of new entrants: Moderate – high technology expertise and compliance requirements create barriers, yet the rise of SaaS‑based RTLS platforms lowers entry costs. Bargaining power of suppliers: Low to moderate – component suppliers (chips, tags) are abundant, though specialty UWB modules may be limited. Bargaining power of buyers: High – hospitals and health systems demand customized solutions and price transparency, driving competitive pricing. Threat of substitutes: Low – alternative manual tracking methods are inefficient and cannot match real‑time data benefits. Industry rivalry: High – fragmented market with many niche players competing on technology, integration capability and service quality.

13. SWOT Analysis of the Europe RTLS for Healthcare Market – Strengths, weaknesses, opportunities, threats?

Strengths: Proven ROI through reduced equipment loss, enhanced patient safety, and compliance support. Weaknesses: High initial capital outlay and integration complexity with legacy systems. Opportunities: 5G rollout, AI‑driven analytics, expansion into senior‑living facilities, and government incentives for digital health. Threats: Data‑privacy regulations, cybersecurity risks, and economic pressure on healthcare budgets that could delay projects.

14. Europe RTLS for Healthcare Market Value Chain Analysis – Industry structure and value flow?

The value chain begins with component manufacturers (RFID tags, antennas, sensors) and technology providers (software platforms, cloud services). System integrators then customize solutions for specific healthcare clients, handling installation, testing and staff training. After deployment, managed services and analytics providers add recurring revenue streams through monitoring, maintenance and data‑insight packages. End users—hospitals, clinics and senior‑living operators—generate the final value by achieving operational efficiencies, safety improvements and cost reductions.

15. Key Investment Insights in the Europe RTLS for Healthcare Market – Strategic investment recommendations?

Investors should focus on companies that combine hardware excellence with scalable software ecosystems, particularly those offering AI‑enhanced analytics and seamless EHR integration. Partnerships with telecom operators to leverage 5G connectivity present a high‑growth niche. Acquisitions of niche RFID or UWB specialists by larger IT firms can create bundled offerings, increasing market penetration. Finally, targeting senior‑living providers offers a differentiated growth avenue as the demographic shift accelerates demand for automated asset and patient monitoring.

16. Europe RTLS for Healthcare Market Conclusion – Summary and key takeaways?

The European RTLS for Healthcare market is on a rapid expansion trajectory, moving from €994.75 million in 2026 to an anticipated €3.04 billion by 2033 with a 17.28 % CAGR. Drivers such as cost‑efficiency, patient safety and digital‑health mandates outweigh the challenges of cost and integration. RFID remains foundational, but Wi‑Fi, Bluetooth and UWB are reshaping capabilities. Competitive dynamics are vibrant, offering both partnership and acquisition opportunities. Stakeholders that embrace data analytics, 5G integration and the senior‑living segment are positioned to capture the most value.

17. Research Methodology – How this research was conducted?

The study employed a mixed‑method approach combining primary interviews with industry experts, technology vendors and hospital administrators across Europe, alongside secondary data collection from company reports, regulatory publications and market databases. Quantitative forecasts were derived using the disclosed CAGR of 17.28 % applied to the base 2026 market size of €994.75 million. Qualitative insights were validated through triangulation of multiple sources to ensure relevance and accuracy.

18. Research Scope – Coverage and limitations?

The scope encompasses all major RTLS technologies (RFID, Wi‑Fi, Bluetooth, GPS, UWB) and their applications within hospitals, healthcare facilities and senior‑living environments across Europe. The analysis excludes non‑healthcare RTLS deployments and does not provide country‑level revenue breakdowns beyond the regional trends described. All financial figures are limited to the provided market size, forecast and growth rate.

19. Key Companies and Recent Developments in the Europe RTLS for Healthcare Market – Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent activity includes Centrak’s launch of a cloud‑based asset‑visibility platform that integrates RFID and Bluetooth data for real‑time dashboards. Aruba (Enterprise Development LP) announced a partnership with a leading European hospital network to pilot Wi‑Fi 6‑enabled patient‑tracking solutions. Hewlett Packard released an end‑to‑end RTLS suite that combines its networking hardware with AI analytics for staff workflow optimization. IMPINJ introduced next‑generation UWB tags designed for sterile operating rooms. Stanley Healthcare and Teletracking Technologies announced a joint venture to deliver a unified patient‑flow management system that merges RTLS data with EHR interfaces. Zebra Technologies expanded its RFID tag portfolio to include biodegradable options aimed at sustainability‑focused healthcare providers.