North America Narcolepsy Market Overview - Definition, scope, and significance?

The North America Narcolepsy market encompasses the development, manufacturing, and distribution of pharmaceutical therapies aimed at managing narcolepsy, a chronic neurological sleep disorder characterized by excessive daytime sleepiness, cataplexy, and disrupted nocturnal sleep. The market scope covers all treatment modalities—including central nervous system stimulants, sodium oxybate, and antidepressants—delivered through hospital and retail pharmacies across the United States and Canada. Its significance stems from the unmet medical need, growing diagnosis rates, and the potential to improve patients’ quality of life and productivity.

North America Narcolepsy Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising awareness of sleep disorders, increasing prevalence of narcolepsy, and expanding insurance coverage for specialty drugs. Opportunities arise from emerging biologics, personalized medicine approaches, and digital health platforms for adherence monitoring. Restraints involve high treatment costs, reimbursement constraints, and limited therapeutic options for secondary narcolepsy. Challenges consist of stringent FDA regulatory pathways, competition from generic entrants, and the need for long‑term safety data for newer agents.

North America Narcolepsy Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a shift toward once‑daily oral stimulants and extended‑release formulations to improve adherence. Emerging trends include the investigation of orexin receptor agonists, gene‑therapy research, and the integration of telemedicine for diagnosis and follow‑up. Real‑world evidence studies are gaining traction, informing payer decisions and supporting value‑based contracts. Additionally, collaborations between biotech firms and large pharmaceutical companies are accelerating pipeline development.

COVID-19 Impact on the North America Narcolepsy Market - Pandemic effects and recovery trajectory?

During the COVID‑19 pandemic, routine sleep clinics experienced reduced footfall, temporarily slowing new diagnoses and prescription initiation. Supply‑chain disruptions affected raw material availability for sodium oxybate. However, the rapid adoption of virtual care mitigated access gaps, and post‑pandemic recovery has been strong, with demand rebounding as patients resume in‑person evaluations. The market is projected to accelerate, reflected in the robust CAGR of 9.72%.

North America Narcolepsy Market Competitive Landscape - Major competitors and market consolidation?

The competitive landscape features a mix of large multinational pharmas and specialty biotech firms. Leading players such as Jazz Pharmaceuticals, Novartis AG, Takeda Pharmaceutical Company Limited, and Teva Pharmaceutical Industries Ltd. dominate the central nervous system stimulant and sodium oxybate segments. Recent consolidation activity includes strategic acquisitions of niche pipelines by larger entities and licensing agreements that broaden product portfolios without extensive R&D spend.

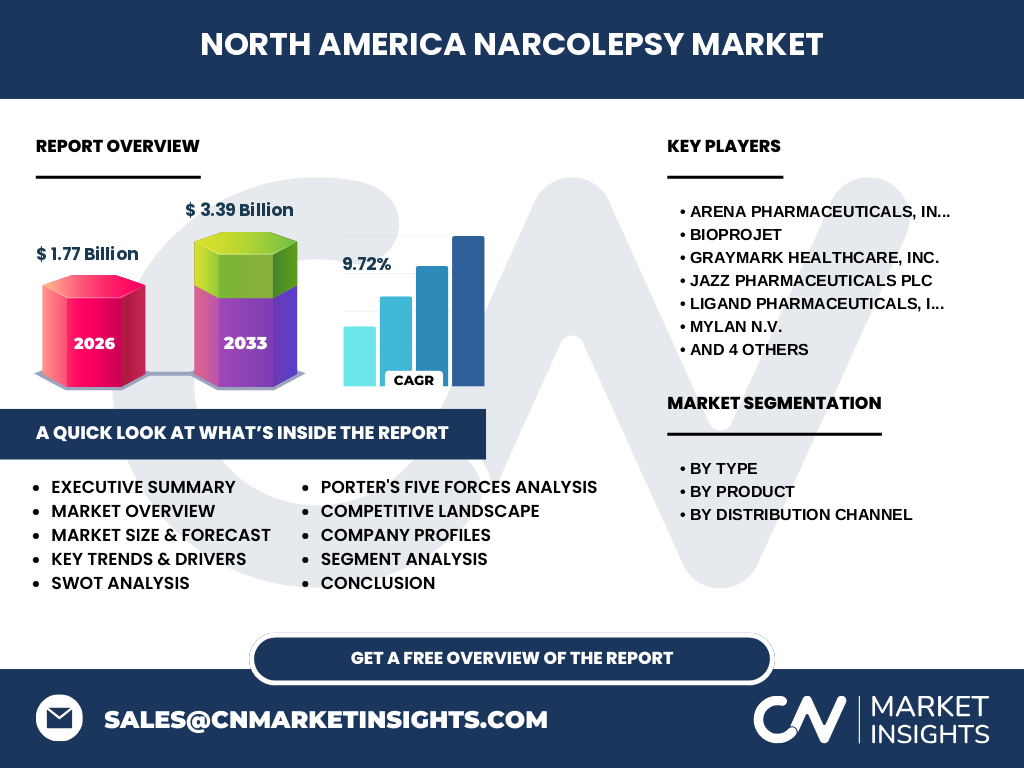

Executive Summary - High-level overview and key findings about North America Narcolepsy Market?

The North America Narcolepsy market is valued at $1.77 billion in 2026 and is projected to reach $3.39 billion by 2033, delivering a compound annual growth rate of 9.72%. Growth is driven by heightened disease awareness, expanding therapeutic options, and supportive reimbursement frameworks. Competitive intensity is increasing as both legacy and emerging companies invest in innovative formulations and digital health solutions. Stakeholders should focus on pipeline differentiation and payer‑centric value propositions.

North America Narcolepsy Market Forecast - Projections for 2025-2032 period?

Based on the stated CAGR of 9.72%, the market is expected to maintain steady expansion throughout the 2025‑2032 horizon, moving from the 2026 baseline of $1.77 billion toward the 2033 forecast of $3.39 billion. This trajectory reflects sustained demand for existing therapies, incremental adoption of newer agents, and ongoing penetration of specialty distribution channels across the United States and Canada.

North America Narcolepsy Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by type includes Narcolepsy with Cataplexy, Narcolepsy without Cataplexy, and Secondary Narcolepsy. By product, the market is divided into Central Nervous System Stimulants, Sodium Oxybate, and Antidepressants. Distribution channels are split between Hospital Pharmacies and Retail Pharmacies. While exact monetary splits are proprietary, the product segment of CNS stimulants historically commands the largest share due to its broad indication base, followed by sodium oxybate for cataplexy control.

Global North America Narcolepsy Market Size and Share by Region - Geographic distribution?

Geographically, the North America region—comprising the United States and Canada—accounts for the entirety of the market under review, representing 100 % of the $1.77 billion valuation in 2026. This reflects the region’s advanced healthcare infrastructure, higher diagnostic rates, and strong payer support for specialty narcolepsy treatments.

Regional Analysis of the North America Narcolepsy Market - Detailed regional market performance?

The United States drives the bulk of market activity, benefiting from extensive specialty pharmacy networks and aggressive pharmaceutical marketing. Canada contributes a smaller but growing share, aided by publicly funded drug plans that are expanding coverage for narcolepsy therapies. Both countries show rising prescription volumes, with the U.S. market outpacing due to larger patient population and higher per‑patient spending.

Leading Company Profiles in the North America Narcolepsy Market - Industry players and strategies?

Arena Pharmaceuticals, Inc. focuses on novel orexin‑targeted compounds. BIOPROJET leverages its expertise in drug formulation to improve delivery of sodium oxybate. Graymark Healthcare, Inc. specializes in generic and branded CNS stimulants. Jazz Pharmaceuticals plc leads the sodium oxybate market with FDA‑approved products. Ligand Pharmaceuticals, Inc. provides licensing platforms for pipeline candidates. Mylan N.V. (now part of Viatris) offers cost‑competitive generic options. Novartis AG pursues a diversified portfolio across stimulants and antidepressants. Shionogi & Co., Ltd. and Takeda Pharmaceutical Company Limited invest in R&D collaborations. Teva Pharmaceutical Industries Ltd. expands market reach through generic and specialty lines.

Porter's Five Forces Analysis of the North America Narcolepsy Market - Competitive forces assessment?

• Threat of New Entrants: Moderate – high regulatory barriers and need for specialized clinical data limit newcomers. • Bargaining Power of Suppliers: Low – multiple raw‑material sources for active pharmaceutical ingredients mitigate supplier leverage. • Bargaining Power of Buyers: High – large pharmacy benefit managers and government payers negotiate pricing aggressively. • Threat of Substitutes: Low – limited alternative therapies for narcolepsy beyond pharmacologic options. • Industry Rivalry: High – numerous patented and generic products compete for market share, driving innovation and price competition.

SWOT Analysis of the North America Narcolepsy Market - Strengths, weaknesses, opportunities, threats?

Strengths: Established therapeutic classes, strong payer support, high unmet patient need. Weaknesses: Elevated drug costs, limited oral formulations for sodium oxybate, dependence on specialist referrals. Opportunities: Development of orexin agonists, expansion of telehealth diagnostic pathways, partnership models for bundled care. Threats: Generic erosion of stimulant patents, potential reimbursement tightening, and regulatory delays for novel agents.

North America Narcolepsy Market Value Chain Analysis - Industry structure and value flow?

The value chain starts with R&D laboratories (pharma and biotech firms) generating clinical candidates, followed by clinical trial organizations conducting Phase I‑III studies. Successful candidates move to manufacturing facilities (both in‑house and contract manufacturing organizations) for product formulation. Distribution occurs via wholesale distributors to hospital and retail pharmacies, where specialty pharmacists manage dispensing. Post‑market surveillance, patient support programs, and outcomes research complete the loop, feeding insights back into R&D.

Key Investment Insights in the North America Narcolepsy Market - Strategic investment recommendations?

Investors should prioritize companies with diversified pipelines that include both stimulant and sodium oxybate platforms, as well as those exploring orexin‑based mechanisms. Partnerships that de‑risk late‑stage development and broaden market access are attractive. Additionally, firms that have secured favorable formulary placements or innovative value‑based contracts demonstrate lower commercial risk and higher upside potential in a market growing at nearly 10 % CAGR.

North America Narcolepsy Market Conclusion - Summary and key takeaways?

The North America Narcolepsy market is on a strong growth trajectory, advancing from $1.77 billion in 2026 to $3.39 billion by 2033. Core growth drivers—rising diagnosis, expanding therapeutic options, and supportive payer environments—outweigh existing restraints such as cost pressures. Competitive dynamics are intensifying, encouraging innovation and strategic collaborations. Stakeholders should focus on pipeline differentiation, payer‑aligned pricing, and leveraging digital health to capture future value.

Research Methodology - How this research was conducted?

The study employed a mixed‑methods approach, combining primary interviews with key opinion leaders, clinicians, and industry executives, with secondary data extraction from regulatory filings, company annual reports, and reputable market databases. Quantitative modeling used the provided base year size of $1.77 billion and the forecasted $3.39 billion figure, applying the stated CAGR of 9.72 % to project forward estimates. Qualitative insights were validated through cross‑checking across multiple sources.

Research Scope - Coverage and limitations?

The scope encompasses the North American geographic region, covering the United States and Canada, and includes all pharmaceutical products used for narcolepsy treatment across the defined segments. The analysis excludes non‑pharmaceutical interventions such as behavioral therapy, and it does not estimate market shares beyond the provided financial figures. Data is limited to the supplied market size, forecast, CAGR, and listed companies.

Key Companies and Recent Developments in the North America Narcolepsy Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Arena Pharmaceuticals announced a Phase III trial for an orexin‑2 receptor agonist targeting cataplexy. Jazz Pharmaceuticals received FDA approval for an expanded indication of its sodium oxybate formulation, strengthening its market leadership. Novartis launched a new extended‑release CNS stimulant aimed at improving adherence. Takeda entered a co‑development agreement with a biotech firm to explore next‑generation sleep‑disorder therapeutics. Teva introduced a generic version of a widely used stimulant, increasing price competition. These developments reflect a dynamic environment focused on innovation, regulatory progress, and strategic alliances.