1. What is the Asia Pacific X‑Ray Security Scanner Market – definition, scope, and significance?

The Asia Pacific X‑Ray Security Scanner Market comprises manufacturers, distributors, and end‑users of X‑ray based screening equipment used to detect prohibited items in airports, seaports, rail stations, border checkpoints, and high‑security facilities across the Asia‑Pacific region. The market scope covers conventional X‑ray and computed tomography (CT) scanners, various scanning dimensions (small, medium, large), and multiple application types such as body, baggage, cargo and parcel scanning. Its significance lies in strengthening national security, facilitating safe trade, and supporting the rapid growth of passenger and freight traffic in a region that accounts for a substantial share of global trade volumes.

2. What are the key drivers, restraints, challenges, and opportunities shaping the market?

Key drivers include heightened terrorism threats, stricter governmental regulations on aviation and border security, and increasing investment in modernizing infrastructure. The expanding e‑commerce sector creates demand for parcel and cargo scanning solutions. Restraints stem from high capital expenditures, complex integration with legacy systems, and regulatory approval timelines. Challenges involve skilled‑personnel shortages and data‑privacy concerns linked to biometric integration. Opportunities arise from the adoption of AI‑enhanced image analytics, portable scanner development, and public‑private partnerships aimed at upgrading critical transit hubs.

3. What are the current and emerging growth trends in the market?

Current trends show a shift from conventional X‑ray units to high‑resolution CT scanners for superior 3‑D imaging and threat detection accuracy. Emerging trends include the integration of machine‑learning algorithms for automated threat recognition, the deployment of wireless, low‑footprint scanners for rapid screening, and the convergence of X‑ray systems with IoT platforms for real‑time monitoring. Additionally, there is a growing preference for modular tunnel designs that can be scaled from small to large dimensions based on site constraints.

4. How has COVID‑19 impacted the Asia Pacific X‑Ray Security Scanner Market and what is the recovery trajectory?

The pandemic caused a temporary dip in scanner installations due to reduced air travel and airport footfall. Supply‑chain disruptions delayed component deliveries, slowing project timelines. However, heightened health‑security protocols accelerated the adoption of contact‑less scanning solutions. As passenger numbers rebound, governments are accelerating security upgrades, leading to a robust recovery. The market is expected to regain momentum by 2024 and enter a high‑growth phase supported by pent‑up travel demand and renewed infrastructure spending.

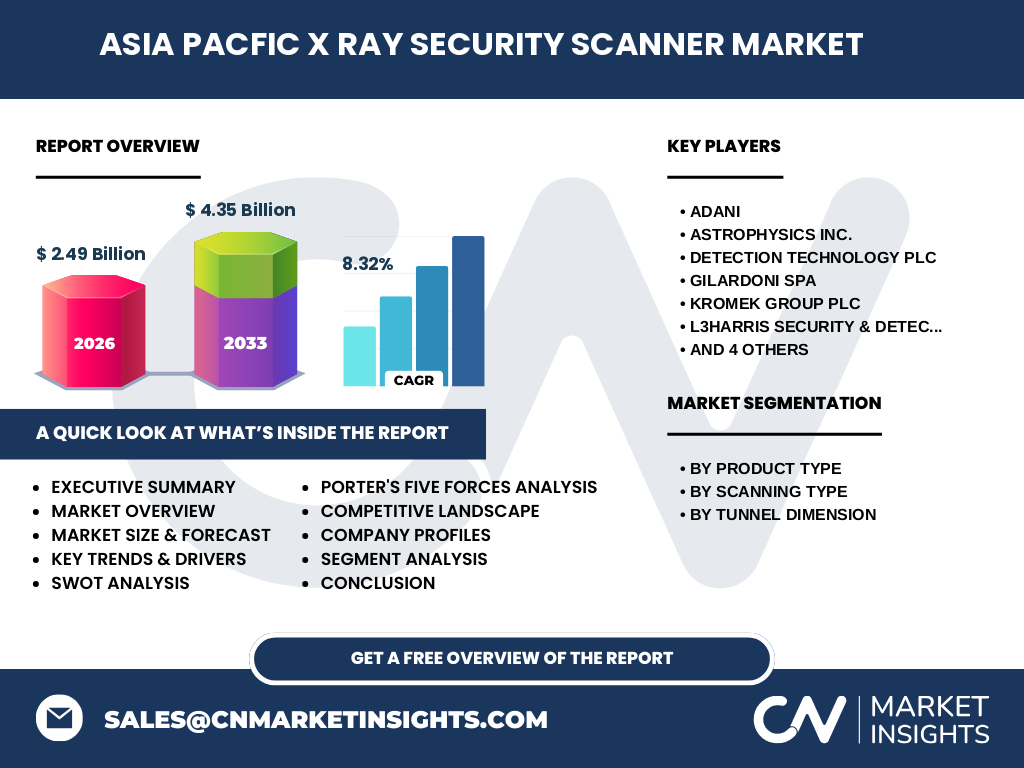

5. Who are the major competitors and what is the level of market consolidation?

Key players include Adani, Astrophysics Inc., Detection Technology Plc, Gilardoni SPA, Kromek Group PLC, L3Harris Security & Detection Systems, Nuctech Company Limited, OSI Systems, Inc., Smiths Detection, and Teledyne ICM. The competitive landscape is moderately consolidated, with a few large multinational firms holding significant technology leadership while niche specialists focus on specific scanner types or regional niches. Mergers, strategic alliances, and joint ventures are common as companies seek to broaden product portfolios and expand geographic reach.

6. What are the high‑level findings and key takeaways from the executive summary?

The Asia Pacific X‑Ray Security Scanner Market is valued at USD 2.49 billion in 2026 and is projected to reach USD 4.35 billion by 2033, reflecting a CAGR of 8.32 %. Growth is fueled by heightened security mandates, expanding air‑cargo volumes, and rapid technology adoption. CT scanners are gaining market share over conventional units, while AI‑driven analytics enhance detection efficiency. Despite capital intensity, the market presents strong upside for investors targeting the high‑growth security‑tech segment in a region with escalating trade activity.

7. What are the forecast expectations for 2025‑2032?

Based on the stated CAGR of 8.32 %, the market is expected to maintain a steady upward trajectory throughout 2025‑2032. Annual growth will be driven by continued government spending on border modernization, increased demand for cargo and parcel scanning in e‑commerce logistics, and the rollout of next‑generation CT solutions. By 2032, the market size is anticipated to approach the upper end of the forecast range, reinforcing the region’s status as a strategic growth engine for X‑ray security technologies.

8. How is the market sized and shared by product type, scanning type, and tunnel dimension?

By product type, the market is split between conventional X‑ray scanners and CT scanners, with CT scanners capturing a larger share due to superior imaging capabilities. Scanning type segmentation includes body, baggage, cargo, and parcel scanning; baggage and cargo scanning together command the majority of revenue because of high volumes at airports and seaports. Tunnel dimension segmentation comprises small, medium, and large tunnels, with medium‑sized solutions dominating the market because they balance footprint and throughput requirements for most mid‑size facilities.

9. What is the geographic distribution of market size and share across the Asia Pacific region?

The market’s geographic spread reflects the economic weight of key sub‑regions. East Asia (China, Japan, South Korea) accounts for the largest share owing to extensive airport networks and advanced manufacturing bases. Southeast Asia (Singapore, Malaysia, Thailand, Indonesia) follows, driven by rapid airport expansion and growing logistics hubs. South Asia (India) shows the fastest growth rate due to large‑scale passenger increases and government‑led security upgrades. Oceania contributes a modest yet steady share, primarily from Australia’s upgraded border infrastructure.

10. What are the detailed regional performance insights?

In China, government mandates for high‑throughput CT scanners at major hubs are accelerating large‑tunnel deployments. Japan focuses on integrating AI analytics into existing scanners to enhance threat detection. South Korea’s strategic partnerships with domestic manufacturers are boosting the adoption of compact scanners for regional airports. Singapore acts as a test‑bed for next‑generation, low‑radiation scanners, while Indonesia’s expanding secondary airports are driving demand for small‑to‑medium tunnel solutions. India’s “Smart Borders” initiative is expected to double scanner installations over the next five years.

11. Which companies lead the market and what are their strategic approaches?

Adani leverages its integrated security services portfolio to offer bundled scanner‑plus‑monitoring solutions. Nuctech Company Limited focuses on high‑resolution CT systems and strong after‑sales support in China. Smiths Detection emphasizes modular designs that can be rapidly retrofitted. L3Harris Security & Detection Systems pursues a technology‑licensing model to embed advanced AI algorithms. OSI Systems, Inc. drives growth through strategic acquisitions of niche sensor manufacturers, expanding its product breadth across all scanning dimensions.

12. How does Porter’s Five Forces assess the market dynamics?

• Threat of new entrants – Moderate: High capital requirements and regulatory hurdles limit newcomers, but niche innovators can enter via specialized software. • Bargaining power of suppliers – Low to moderate: Multiple component suppliers (detectors, X‑ray tubes) reduce dependency on any single source. • Bargaining power of buyers – High: Governments and large airport authorities negotiate long‑term contracts and demand cost‑effective solutions. • Threat of substitutes – Low: Alternative screening technologies (millimeter‑wave, trace detection) complement rather than replace X‑ray systems. • Competitive rivalry – High: Established players compete on technology, service, and price, leading to frequent product upgrades and partnership deals.

13. What are the SWOT insights for the overall market?

Strengths: Proven detection efficacy, regulatory support, and growing demand for cargo security. Weaknesses: High upfront costs and technical complexity. Opportunities: AI‑driven analytics, portable scanners, and expansion into emerging airports and logistics parks. Threats: Rapid technology obsolescence, potential regulatory changes on radiation exposure, and geopolitical trade tensions affecting supply chains.

14. How is the value chain structured for X‑ray security scanners?

The value chain starts with raw‑material suppliers (lead‑glass, scintillators), followed by component manufacturers (X‑ray tubes, detectors). System integrators assemble scanners and embed software. Distributors and system integrators handle regional sales, installation, and training. After‑sales services, including maintenance contracts and software updates, complete the chain. Companies that control multiple stages—particularly integration and service—gain competitive advantage through tighter cost control and customer lock‑in.

15. What investment insights should stakeholders consider?

Investors should focus on companies with strong R&D pipelines in AI imaging and those securing long‑term government contracts. Partnerships with local system integrators accelerate market entry and reduce regulatory risk. Funding rounds targeting portable and low‑radiation technologies present high upside as airports seek passenger‑friendly solutions. Monitoring policy initiatives—such as “Smart Border” programs—can uncover early‑stage investment opportunities.

16. What conclusions can be drawn from the market analysis?

The Asia Pacific X‑Ray Security Scanner Market is on a decisive growth trajectory, underpinned by security imperatives and technological innovation. CT scanners are becoming the default choice, while AI and modular designs differentiate market leaders. Despite cost challenges, the region’s expanding travel and trade volumes ensure sustained demand. Companies that adapt through advanced analytics, flexible tunnel solutions, and strategic alliances are positioned to capture the largest share of the projected USD 4.35 billion market by 2033.

17. How was the research conducted?

The study combined primary interviews with industry executives, secondary data from government publications, trade journals, and financial reports, and quantitative modeling using the provided market size, forecast, and CAGR figures. Trend analysis incorporated technology adoption rates, regulatory timelines, and macro‑economic indicators across the Asia Pacific region.

18. What is the scope and any limitations of the research?

The scope covers the full spectrum of X‑ray security scanning equipment sold and deployed in the Asia Pacific from 2025 to 2033, segmented by product type, scanning application, and tunnel dimension. Geographic coverage includes East, Southeast, South Asia, and Oceania. Limitations stem from the reliance on publicly available data for competitive dynamics and the absence of exact market‑share percentages for individual companies.

19. Which key companies have recent developments, and what are those developments?

Adani announced a joint venture with a leading AI firm to embed real‑time threat analytics in its scanners. Astrophysics Inc. launched a lightweight, battery‑operated baggage scanner targeting remote airports. Detection Technology Plc secured a multi‑year contract with a major Southeast Asian airport for large‑tunnel CT installations. Gilardoni SPA introduced a compact parcel scanner designed for e‑commerce fulfillment centers. Kromek Group PLC released a next‑gen detector that reduces radiation dose by 30 %. L3Harris rolled out a cloud‑based monitoring platform for remote scanner management. Nuctech unveiled a high‑throughput cargo scanner with integrated RFID scanning. OSI Systems completed the acquisition of a niche software vendor to enhance its AI portfolio. Smiths Detection announced a strategic partnership with a regional rail operator to deploy body scanning kiosks. Teledyne ICM introduced a modular scanner line that can be reconfigured from small to medium tunnel sizes within weeks.