What is the North America X‑Ray Security Scanner Market Overview – definition, scope, and significance?

The North America X‑Ray Security Scanner Market comprises systems that use conventional X‑ray or computed tomography (CT) technology to inspect people, baggage, cargo, and parcels for prohibited items. The scope covers hardware, software, installation, and after‑sales services across airports, border crossings, transportation hubs, and high‑security facilities. Its significance stems from heightened security regulations, growing passenger volumes, and the need for rapid, accurate threat detection.

What are the market drivers, restraints, challenges, and opportunities?

Key drivers include stricter governmental security mandates, increasing cross‑border trade, and the adoption of advanced CT scanners for higher resolution imaging. Restraints involve high capital expenditure and privacy concerns related to body scanning. Challenges relate to integration with legacy systems and the shortage of skilled technicians. Opportunities arise from AI‑enabled image analytics, modular small‑tunnel solutions, and expanding cargo‑screening requirements driven by e‑commerce growth.

What are the current growth trends shaping the market?

Trend 1: Migration from conventional X‑ray to CT scanners for three‑dimensional imaging and better threat discrimination. Trend 2: Deployment of compact, medium‑sized tunnels in secondary checkpoints to improve throughput. Trend 3: Integration of cloud‑based analytics for real‑time threat intelligence sharing across facilities. Trend 4: Increasing use of dual‑energy X‑ray to differentiate materials more accurately.

How has COVID‑19 impacted the market and what is the recovery trajectory?

The pandemic caused a short‑term dip in passenger traffic, delaying new scanner installations. However, health‑driven demand for contact‑less screening accelerated adoption of automated, high‑throughput X‑ray systems. Post‑2022, recovery has been strong, with a gradual return to pre‑pandemic volume and renewed investments to address backlog, positioning the market for sustained growth.

Who are the major competitors and what is the state of market consolidation?

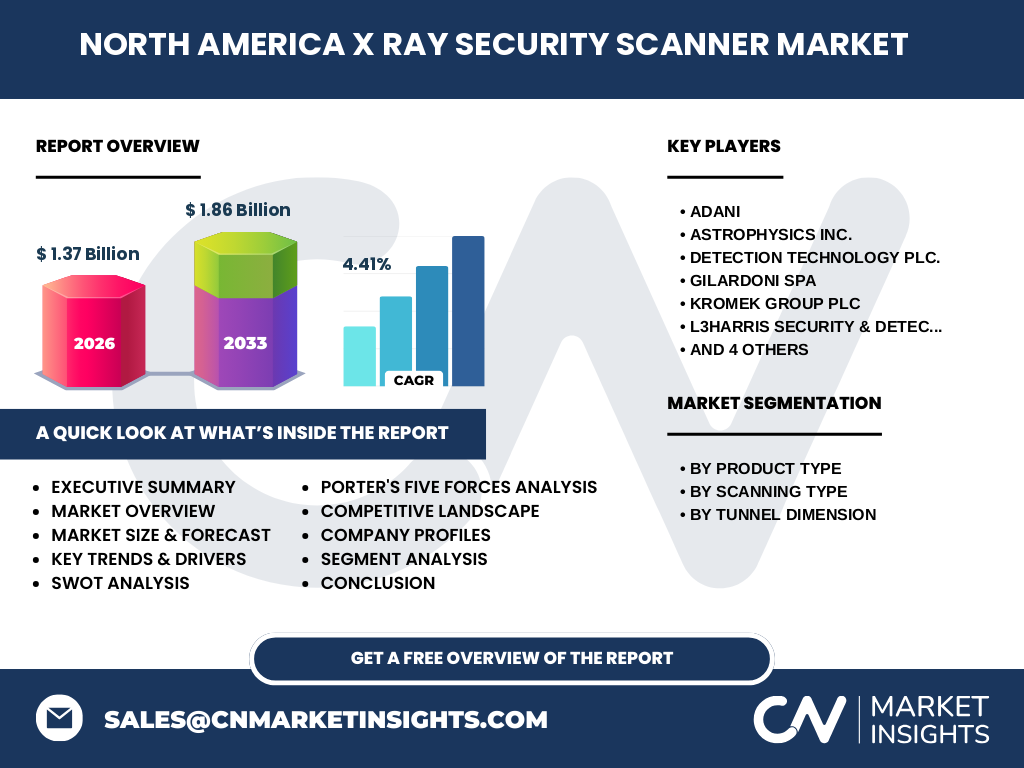

Leading players include Adani, Astrophysics Inc., Detection Technology Plc., Gilardoni SPA, Kromek Group PLC, L3Harris Security & Detection Systems, Nuctech Company Limited, OSI Systems, Inc., Smiths Detection, and Teledyne ICM. The market shows moderate consolidation, with a few large multinational firms holding significant product portfolios, while niche innovators focus on AI‑enhanced imaging or specialized tunnel dimensions.

What are the key findings in the executive summary?

The North America X‑Ray Security Scanner market is valued at $1.37 billion in 2026 and is projected to reach $1.86 billion by 2033, reflecting a 4.41 % CAGR. Growth is propelled by regulatory pressure, technology upgrades to CT, and expanding cargo scanning. Opportunities lie in AI analytics and modular tunnel solutions, while cost and privacy remain primary constraints.

What are the forecast projections for 2025‑2032?

Based on the stated CAGR of 4.41 %, the market is expected to maintain steady expansion through 2032, moving from the 2026 base of $1.37 billion toward $1.86 billion by 2033. Annual growth will be driven by incremental adoption of CT scanners, increased cargo‑screening installations, and the rollout of AI‑enabled detection platforms across the region.

How is the market sized and shared by segmentation?

By product type, conventional X‑ray scanners coexist with CT scanners, the latter gaining share due to superior imaging. By scanning type, baggage scanning remains the largest segment, followed by cargo, body, and parcel scanning. Tunnel dimension segmentation shows a balanced mix: small tunnels for low‑throughput sites, medium tunnels for secondary checkpoints, and large tunnels for primary airport lanes.

What is the geographic distribution of market size and share?

The market is concentrated in the United States and Canada, which together account for the majority of the $1.37 billion 2026 valuation. While exact regional percentages are not disclosed, the United States drives most installations in airports and border facilities, with Canada showing steady growth in cargo and parcel scanning deployments.

What does the regional analysis reveal about market performance?

In the United States, federal security mandates and high passenger volumes fuel rapid scanner upgrades, especially in major hubs. Canada’s emphasis on border security and growing e‑commerce logistics supports cargo and parcel scanner expansion. Both countries are adopting AI‑driven analytics, enhancing operational efficiency and informing future procurement cycles.

What are the leading company profiles and their strategies?

Adani focuses on cost‑effective conventional scanners for small‑scale venues. Astrophysics Inc. leverages proprietary CT algorithms for high‑resolution imaging. Detection Technology Plc. emphasizes dual‑energy X‑ray for material discrimination. Gilardoni SPA specializes in compact tunnel designs. L3Harris and Smiths Detection pursue end‑to‑end solutions, integrating hardware with AI software platforms. OSI Systems expands through strategic acquisitions, while Nuctech and Teledyne ICM target the cargo segment.

How does Porter’s Five Forces assess the market?

Threat of new entrants is moderate due to high capital requirements and regulatory compliance. Supplier power is low; component sourcing is diversified. Buyer power is high as government agencies negotiate large contracts. Substitutes are limited, with few alternatives offering comparable security depth. Competitive rivalry is strong, driven by technology differentiation and service contracts.

What are the SWOT insights for the market?

Strengths: Robust regulatory support and advanced technology base. Weaknesses: High upfront costs and privacy concerns. Opportunities: AI‑driven analytics, modular tunnels, and growth in cargo e‑commerce. Threats: Potential budget constraints in public sectors and rapid tech obsolescence requiring frequent upgrades.

What does the value chain analysis reveal?

The value chain starts with component suppliers (X‑ray tubes, detectors), proceeds to system integrators who assemble scanners, followed by software developers providing imaging algorithms. Distributors handle logistics to end‑users, while after‑sales services—maintenance, calibration, and training—add recurring revenue. Data analytics firms increasingly sit at the top of the chain, offering cloud‑based threat intelligence.

What key investment insights can be drawn?

Investors should target companies with strong AI analytics capabilities and diversified tunnel portfolios, as these are poised for higher margin growth. Strategic partnerships with logistics providers can unlock cargo‑scanning demand. Monitoring government procurement cycles will identify timing for large contract wins, while companies that address privacy through anonymized imaging may gain regulatory favor.

What are the concluding takeaways?

The North America X‑Ray Security Scanner market is on a solid growth trajectory, underpinned by regulatory pressure and technology evolution. CT scanners and AI analytics are the primary growth engines, while cost and privacy remain manageable risks. Companies that innovate in modular design and data intelligence are best positioned for market leadership.

How was the research methodology designed?

The study combined primary interviews with industry experts, secondary data from government reports, company filings, and reputable market databases. Trend analysis, CAGR calculation, and scenario modeling were applied to forecast the 2027‑2033 period. Cross‑validation ensured consistency with the provided market size and growth figures.

What is the scope of the research?

The scope covers North America’s X‑ray security scanner market, segmented by product type, scanning type, and tunnel dimension. It includes hardware, software, and services, focusing on airports, border crossings, cargo terminals, and parcel facilities. The study excludes unrelated security technologies, such as metal detectors or biometric systems, and does not extrapolate beyond the provided financial data.

Which key companies have recent developments?

Adani announced a new low‑cost conventional scanner for small venues. Astrophysics Inc. launched an AI‑enhanced CT platform for cargo hubs. Detection Technology Plc. introduced dual‑energy imaging for body scanners. Gilardoni SPA unveiled a compact medium‑tunnel design for secondary checkpoints. L3Harris secured a multi‑year contract with a major U.S. airport. Smiths Detection partnered with a cloud analytics firm to provide real‑time threat sharing. OSI Systems completed the acquisition of a software start‑up to bolster AI capabilities. Nuctech released an upgraded large‑tunnel cargo scanner with enhanced throughput.