Smart Water Metering Market Overview - Definition, scope, and significance

Smart water metering represents a technological advancement in water consumption measurement and management systems. These systems utilize advanced communication technologies, sensors, and data analytics to provide real-time monitoring, automated reading capabilities, and enhanced water usage insights. The market encompasses various types of smart meters including Advanced Metering Infrastructure (AMI) and Automated Meter Reading (AMR) systems, serving residential, industrial, and commercial end users. The significance of this market lies in its ability to address critical water management challenges, reduce water loss through leak detection, enable accurate billing, and promote water conservation efforts globally. As water scarcity becomes an increasingly pressing issue worldwide, smart water metering solutions offer municipalities and utilities the tools needed to optimize water distribution networks and improve operational efficiency.

Smart Water Metering Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The smart water metering market is driven by several key factors including increasing water scarcity concerns, aging water infrastructure requiring modernization, government initiatives promoting water conservation, and the need for accurate billing systems. The growing demand for real-time data monitoring and the integration of Internet of Things (IoT) technologies in water management systems further accelerate market growth. However, the market faces restraints such as high initial installation costs, concerns about data security and privacy, and the complexity of integrating smart meters with existing infrastructure. Challenges include the need for skilled workforce to manage these systems and resistance from traditional utility providers. Opportunities exist in emerging markets where water infrastructure is still developing, technological advancements in meter accuracy and communication protocols, and the potential for integrating artificial intelligence for predictive maintenance and consumption pattern analysis.

Smart Water Metering Market Growth Trends - Current and emerging trends shaping the market

The smart water metering market is experiencing several notable growth trends. The adoption of AMI systems is accelerating due to their two-way communication capabilities and real-time data transmission features. There is an increasing trend toward the integration of advanced analytics and cloud computing platforms with smart metering systems, enabling utilities to gain deeper insights into consumption patterns. The market is also witnessing a shift toward ultrasonic and electromagnetic meter types due to their higher accuracy and longer lifespan compared to traditional mechanical meters. Additionally, the growing emphasis on sustainability and water conservation is driving utilities to implement smart metering solutions as part of broader smart city initiatives. The emergence of 5G technology is expected to further enhance the capabilities of smart water metering systems by providing faster and more reliable communication networks.

COVID-19 Impact on the Smart Water Metering Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially disrupted the smart water metering market through supply chain interruptions, delayed infrastructure projects, and reduced capital expenditure by utilities facing economic uncertainties. Installation and maintenance activities were hindered due to lockdown measures and social distancing requirements. However, the pandemic also highlighted the importance of remote monitoring and automated systems, accelerating interest in smart water metering solutions. Utilities recognized the value of these systems in enabling contactless operations and maintaining service continuity during crisis situations. As economies recover, the market is witnessing renewed investment in water infrastructure modernization projects, with smart metering being a key component. The recovery trajectory shows a shift toward more resilient and digitally-enabled water management systems, with increased focus on real-time monitoring and predictive maintenance capabilities.

Smart Water Metering Market Competitive Landscape - Major competitors and market consolidation

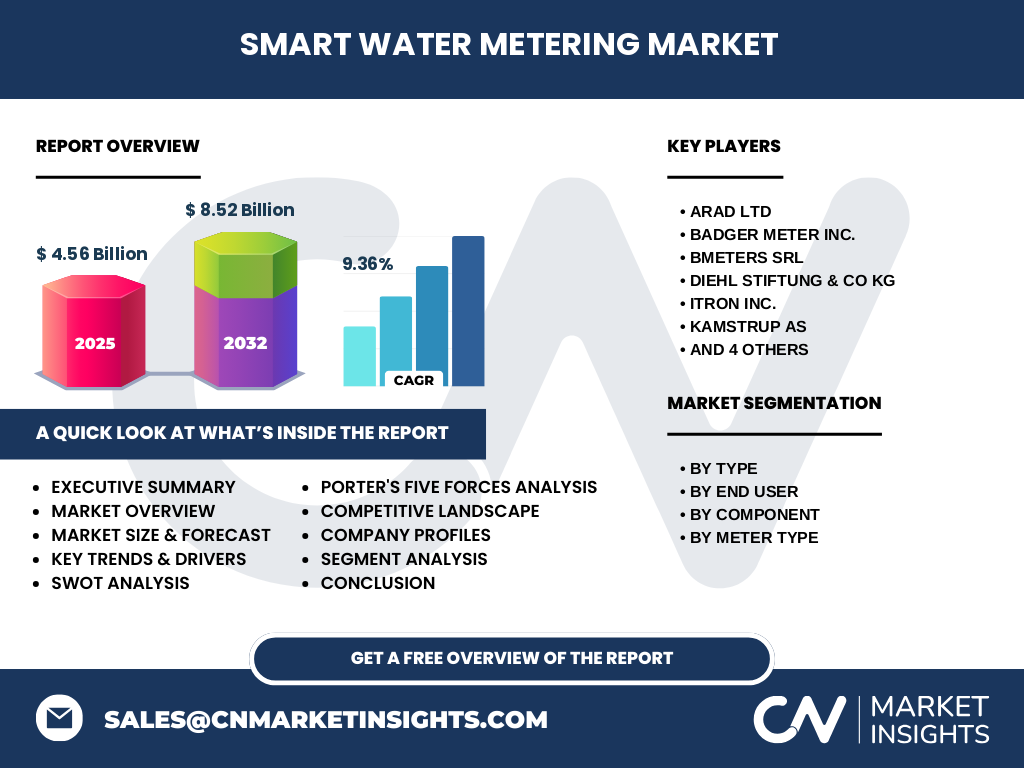

The smart water metering market features a mix of established players and emerging companies competing for market share. Major competitors include Arad Ltd, Badger Meter Inc., Bmeters SRL, Diehl Stiftung & Co KG, Itron Inc., Kamstrup AS, Mueller Water Products Inc., Neptune Technology Group Inc., Sensus USA Inc, and WAVIoT Integrated Systems LLC. The competitive landscape is characterized by ongoing technological innovation, strategic partnerships, and mergers and acquisitions aimed at expanding product portfolios and geographic presence. Companies are focusing on developing advanced metering solutions with improved accuracy, longer battery life, and enhanced communication capabilities. The market is witnessing increased consolidation as larger players acquire smaller innovative companies to strengthen their technological capabilities and market position. Competition is intensifying in emerging markets where water infrastructure development presents significant growth opportunities.

Executive Summary - High-level overview and key findings about Smart Water Metering Market

The smart water metering market is experiencing robust growth, driven by the increasing need for efficient water management solutions and infrastructure modernization. With a market size of 4.56 Billion in 2025 and projected to reach 8.52 Billion by 2032, growing at a CAGR of 9.36%, the market presents significant opportunities for stakeholders. The market is segmented by type (AMI and AMR), end user (residential and industrial), component (controlling unit, display storage and integrated software), and meter type (ultrasonic meters, electromagnetic meters, and electromechanical meter). Key players are focusing on technological innovation and strategic partnerships to maintain competitive advantage. The market is characterized by increasing adoption of advanced metering infrastructure, integration of IoT and analytics capabilities, and growing emphasis on water conservation. Despite challenges such as high initial costs and data security concerns, the long-term benefits of smart water metering systems are driving widespread adoption across various regions and applications.

Smart Water Metering Market Forecast - Projections for 2025-2032 period

The smart water metering market is projected to experience substantial growth between 2025 and 2032, with the market size expected to increase from 4.56 Billion in 2025 to 8.52 Billion by 2032, representing a compound annual growth rate (CAGR) of 9.36%. This growth trajectory is supported by increasing investments in water infrastructure modernization, rising awareness about water conservation, and technological advancements in metering solutions. The AMI segment is expected to witness higher growth compared to AMR due to its advanced capabilities and real-time data transmission features. The residential segment is anticipated to maintain significant market share, driven by smart city initiatives and government regulations promoting water conservation. The ultrasonic meter type is projected to gain increased adoption due to its superior accuracy and reliability. Regional growth will vary, with developed markets focusing on infrastructure upgrades and emerging markets investing in new installations to support growing urbanization and industrialization.

Smart Water Metering Market Size and Share by Segmentation - Breakdown by {segmentData}

The smart water metering market is segmented across multiple dimensions, each contributing differently to the overall market size and share. By type, the market is divided into AMI (Advanced Metering Infrastructure) and AMR (Automated Meter Reading) systems, with AMI showing stronger growth potential due to its advanced two-way communication capabilities. By end user, the market serves residential and industrial sectors, with the residential segment maintaining a significant share due to widespread implementation in urban areas and smart city projects. The component segment includes controlling units, display storage, and integrated software, with integrated software gaining importance as analytics capabilities become more sophisticated. By meter type, the market encompasses ultrasonic meters, electromagnetic meters, and electromechanical meters, with ultrasonic meters showing increasing adoption due to their higher accuracy and longer operational life. Each segment presents unique growth opportunities and challenges, contributing to the overall market dynamics and competitive landscape.

Global Smart Water Metering Market Size and Share by Region - Geographic distribution

The global smart water metering market exhibits varying growth patterns across different regions, influenced by factors such as infrastructure development, regulatory frameworks, and technological adoption rates. North America currently holds a significant market share, driven by aging water infrastructure requiring modernization and stringent water conservation regulations. Europe follows closely, with countries like the UK, Germany, and France implementing smart metering solutions as part of their environmental sustainability initiatives. The Asia-Pacific region is expected to witness the highest growth rate during the forecast period, fueled by rapid urbanization, industrialization, and government initiatives to improve water management in countries like China and India. Latin America and the Middle East & Africa regions are also showing increasing adoption of smart water metering solutions, albeit at a slower pace, primarily driven by the need to address water scarcity issues and improve water distribution efficiency.

Regional Analysis of the Smart Water Metering Market - Detailed regional market performance

The smart water metering market demonstrates distinct regional characteristics and growth patterns. In North America, the market is mature with high penetration rates, particularly in the United States, where utilities are focused on replacing aging infrastructure and meeting regulatory requirements for water conservation. Europe shows strong adoption driven by environmental regulations and sustainability goals, with countries like the UK and Germany leading in implementation. The Asia-Pacific region presents the most dynamic growth scenario, with countries like China, India, and Australia investing heavily in water infrastructure development and smart city initiatives. In Latin America, countries such as Brazil and Mexico are gradually adopting smart metering solutions to address water loss issues and improve billing accuracy. The Middle East & Africa region, despite facing economic challenges, is recognizing the importance of smart water management due to severe water scarcity issues, with countries like the UAE and Saudi Arabia leading adoption efforts.

Leading Company Profiles in the Smart Water Metering Market - Industry players and strategies

The smart water metering market features several key players implementing diverse strategies to maintain and expand their market positions. Arad Ltd focuses on innovative ultrasonic metering solutions with advanced communication capabilities. Badger Meter Inc. emphasizes comprehensive smart water solutions combining hardware and software platforms. Bmeters SRL specializes in high-precision electromagnetic meters for industrial applications. Diehl Stiftung & Co KG leverages its engineering expertise to develop robust and reliable metering systems. Itron Inc. offers end-to-end smart infrastructure solutions with strong focus on data analytics. Kamstrup AS is known for its ultrasonic water meters with intelligent features. Mueller Water Products Inc. provides integrated water infrastructure solutions. Neptune Technology Group Inc. specializes in advanced metering infrastructure systems. Sensus USA Inc. offers comprehensive smart metering and analytics platforms. WAVIoT Integrated Systems LLC focuses on IoT-enabled water metering solutions. These companies are pursuing strategies such as product innovation, strategic partnerships, geographic expansion, and acquisitions to strengthen their market positions.

Porter's Five Forces Analysis of the Smart Water Metering Market - Competitive forces assessment

Porter's Five Forces analysis reveals the competitive dynamics shaping the smart water metering market. The threat of new entrants is moderate due to high initial capital requirements and the need for technological expertise, though opportunities exist for specialized players focusing on niche segments. The bargaining power of buyers is significant as utilities and municipalities often have substantial purchasing power and can influence pricing and product specifications. The bargaining power of suppliers is relatively low due to the availability of multiple component suppliers and the ability of large manufacturers to integrate vertically. The threat of substitute products is low as smart water meters offer unique advantages over traditional mechanical meters in terms of accuracy, remote reading capabilities, and data analytics. Competitive rivalry is intense among existing players, characterized by continuous product innovation, pricing pressures, and the need to differentiate through value-added services and technological capabilities.

SWOT Analysis of the Smart Water Metering Market - Strengths, weaknesses, opportunities, threats

The smart water metering market exhibits distinct strengths, weaknesses, opportunities, and threats. Strengths include the ability to provide accurate billing, detect leaks in real-time, enable remote monitoring, and support water conservation efforts. The technology's integration with IoT and analytics platforms represents a significant advantage in terms of data-driven decision making. Weaknesses include high initial installation costs, potential cybersecurity vulnerabilities, and the complexity of integrating with existing infrastructure. Opportunities exist in emerging markets with growing water infrastructure needs, technological advancements improving meter accuracy and communication capabilities, and increasing government support for water conservation initiatives. Threats include economic uncertainties affecting utility investments, potential regulatory changes, competition from alternative water management technologies, and challenges related to data privacy and security concerns. The market's ability to address water scarcity issues while managing operational costs presents a compelling value proposition despite these challenges.

Smart Water Metering Market Value Chain Analysis - Industry structure and value flow

The smart water metering market value chain encompasses multiple stages from component manufacturing to end-user implementation. At the upstream level, the value chain includes manufacturers of electronic components, communication modules, sensors, and other hardware elements. The midstream segment involves system integrators, software developers, and metering solution providers who combine these components into functional smart metering systems. Value-added services such as installation, maintenance, and data analytics are provided by specialized service providers and utilities. The downstream segment consists of end-users including residential consumers, industrial facilities, and municipal water utilities. Key value drivers in this chain include technological innovation, system reliability, data accuracy, and customer support services. The integration of advanced analytics and cloud computing capabilities has created new value propositions, enabling utilities to offer enhanced services such as consumption pattern analysis, predictive maintenance, and personalized conservation recommendations.

Key Investment Insights in the Smart Water Metering Market - Strategic investment recommendations

The smart water metering market presents compelling investment opportunities driven by increasing global water scarcity concerns and the need for efficient water management solutions. Strategic investments should focus on companies developing advanced metering infrastructure with enhanced communication capabilities and integration with IoT platforms. The growing emphasis on data analytics and cloud-based solutions presents opportunities for investments in software and analytics companies that complement hardware offerings. Geographic diversification is recommended, with particular attention to emerging markets in Asia-Pacific and Latin America where water infrastructure development is accelerating. Investors should consider companies with strong technological capabilities in ultrasonic and electromagnetic metering technologies, as these segments show higher growth potential. Strategic partnerships and acquisitions in the smart city and utility management sectors could provide synergistic growth opportunities. Additionally, investments in cybersecurity solutions for smart metering systems are increasingly important given growing concerns about data protection and system integrity.

Smart Water Metering Market Conclusion - Summary and key takeaways

The smart water metering market represents a critical component of modern water management infrastructure, offering solutions to address global water scarcity challenges while improving operational efficiency for utilities. With a projected market growth from 4.56 Billion in 2025 to 8.52 Billion by 2032 at a CAGR of 9.36%, the market demonstrates strong long-term potential. Key trends include the increasing adoption of AMI systems, integration of advanced analytics and IoT capabilities, and growing emphasis on water conservation. While challenges such as high initial costs and data security concerns exist, the benefits of accurate billing, leak detection, and remote monitoring continue to drive widespread adoption. The market's future success will depend on technological innovation, strategic partnerships, and the ability to address regional infrastructure needs while managing cybersecurity and data privacy concerns effectively.

Research Methodology - How this research was conducted

This comprehensive market research was conducted using a combination of primary and secondary research methodologies. Primary research involved interviews with industry experts, key opinion leaders, and executives from leading smart water metering companies to gather insights on market trends, technological developments, and competitive strategies. Secondary research encompassed extensive review of company annual reports, industry publications, technical journals, and market databases to validate findings and establish market size and growth projections. Data triangulation was employed to cross-verify information from multiple sources, ensuring accuracy and reliability. The research methodology included both top-down and bottom-up approaches to estimate market size and segment shares. Regional analysis was conducted by examining local market conditions, regulatory frameworks, and infrastructure development patterns. The forecast period analysis incorporated macroeconomic indicators, technological trends, and industry-specific factors to project future market dynamics accurately.

Research Scope - Coverage and limitations

This research report covers the global smart water metering market from 2025 to 2032, focusing on key market segments, regional dynamics, competitive landscape, and growth drivers. The scope includes analysis of market size, share, and growth trends across different meter types (AMI, AMR, ultrasonic, electromagnetic, and electromechanical), end-user segments (residential and industrial), and geographic regions. The report examines technological advancements, regulatory frameworks, and investment patterns influencing market development. Limitations of this research include the availability of certain proprietary data from companies, variations in regional reporting standards, and the dynamic nature of technological developments that may impact market projections. The analysis primarily focuses on commercial smart water metering solutions, excluding experimental or prototype technologies not yet commercially viable. Market size and share figures are based on available data and industry estimates, with projections subject to economic and technological uncertainties.

Key Companies and Recent Developments in the Smart Water Metering Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The smart water metering market features several prominent companies driving innovation and market growth. Arad Ltd recently announced the launch of its next-generation ultrasonic water meters with enhanced communication capabilities and extended battery life. Badger Meter Inc. unveiled its BEACON advanced metering analytics platform, integrating cellular and fixed network endpoints for improved data management. Bmeters SRL introduced new electromagnetic meters designed specifically for industrial applications with higher accuracy requirements. Diehl Stiftung & Co KG expanded its product portfolio with smart metering solutions incorporating advanced IoT connectivity features. Itron Inc. announced strategic partnerships with cloud service providers to enhance its data analytics capabilities for water utilities. Kamstrup AS launched its new ultrasonic water meters with integrated pressure measurement capabilities for improved network monitoring. Mueller Water Products Inc. acquired a smart infrastructure analytics company to strengthen its digital water management offerings. Neptune Technology Group Inc. introduced its R450 RF receiver system with extended communication range and improved data collection efficiency. Sensus USA Inc. announced the expansion of its FlexNet communication network to support growing smart city initiatives. WAVIoT Integrated Systems LLC launched its LoRaWAN-based smart water metering solution targeting emerging markets with limited infrastructure. These developments reflect the industry's focus on technological advancement, strategic partnerships, and expanding market reach to address evolving water management needs.