What is the North America Tortilla Market Overview – definition, scope, and significance?

The North America Tortilla Market encompasses the production, distribution, and consumption of tortilla‑based products across the United States, Canada, and Mexico. It includes both organic and conventional varieties, derived from wheat or corn, and covers product types such as tortilla chips, taco shells, tostadas, flour tortillas, and corn tortillas. The market is significant because tortillas are a staple in Mexican‑American cuisine and a rapidly growing component of convenience and snack segments, driving substantial revenue and influencing broader food‑service trends.

What are the primary drivers, restraints, challenges, and opportunities shaping the North America Tortilla Market?

Key drivers include rising demand for ethnic and convenience foods, health‑focused consumer trends favoring organic and whole‑grain options, and expanding food‑service channels. Restraints stem from volatile commodity prices for wheat and corn and regulatory scrutiny over labeling. Challenges involve intense competition from alternative snack categories and supply‑chain disruptions. Opportunities arise from product innovation (e.g., gluten‑free, low‑carb tortillas), growth of online grocery platforms, and strategic partnerships that expand distribution reach.

What are the current growth trends in the North America Tortilla Market?

Current trends feature a surge in premium and organic tortilla offerings, driven by health‑conscious shoppers. Manufacturers are diversifying product lines with flavored and functional tortillas (e.g., high‑protein, fortified). There is also a clear shift toward omnichannel sales, with online grocery sales accelerating post‑pandemic. Additionally, the snack‑reinvention trend sees tortilla chips being positioned as healthier alternatives to traditional potato chips through better‑for‑you formulations.

How has COVID‑19 impacted the North America Tortilla Market and what is the recovery trajectory?

The pandemic initially disrupted supply chains and reduced food‑service demand, but it simultaneously boosted home‑cooking and snacking, leading to a net positive effect on tortilla sales. Online purchasing surged, prompting manufacturers to strengthen e‑commerce fulfillment. Recovery is solid, with demand stabilizing across all channels and the market poised for continued growth as consumer habits that favor convenient, shelf‑stable products remain entrenched.

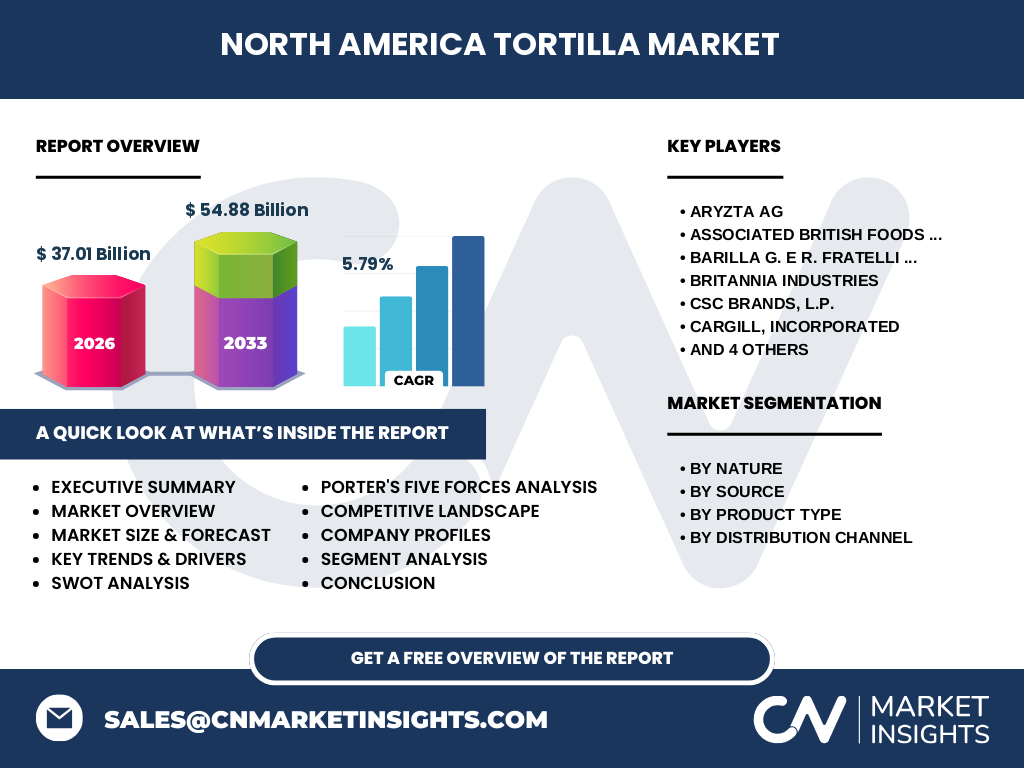

Who are the major competitors in the North America Tortilla Market and what is the state of market consolidation?

Leading players include Aryzta AG, Associated British Foods plc, Barilla G. e R. Fratelli S.p.A, Britannia Industries, CSC Brands L.P., Cargill, Incorporated, Conagra Inc., Finsbury Food Group Plc, Premier Foods Group Limited, and Rich Products Corporation. The market exhibits moderate consolidation, with large multinational food companies leveraging scale to acquire niche organic brands and to expand their product portfolios across the various tortilla segments.

What does the executive summary reveal about the North America Tortilla Market?

The executive summary highlights a robust market valued at $37.01 billion in 2026, with a projected increase to $54.88 billion by 2033, reflecting a 5.79 % CAGR. Growth is driven by health‑centric product innovation, expanding distribution channels, and sustained consumer demand for ethnic convenience foods. Competitive dynamics are shaped by both large conglomerates and agile specialty brands, while digital channels are becoming pivotal for market expansion.

What are the forecasted market dynamics for 2025‑2032 in the North America Tortilla Market?

Forecasts indicate steady expansion, maintaining the 5.79 % CAGR through 2032. Organic tortillas are expected to capture a higher share as consumers prioritize clean‑label foods. Corn‑based products will remain strong, especially in the snack segment, while wheat‑based flour tortillas will continue to dominate the food‑service arena. Online sales are projected to grow at a faster pace than traditional retail, reinforcing the importance of digital strategies.

How is the market size and share distributed by segmentation?

Segmentation by nature divides the market into organic and conventional categories, with conventional products currently holding the larger portion due to broader availability, while organic is gaining traction. By source, wheat and corn are the primary raw materials, each supporting distinct product lines—flour tortillas rely on wheat, whereas corn tortillas and many snack formats depend on corn. Product‑type segmentation includes tortilla chips, taco shells, tostadas, flour tortillas, and corn tortillas, with tortilla chips and flour tortillas representing the highest volume sales. Distribution channels are split among hypermarkets/supermarkets, convenience stores, online platforms, and food‑service outlets, each contributing to the overall market structure.

What is the geographic distribution of the North America Tortilla Market by region?

The market is concentrated in the United States, which leads in both production capacity and consumption volume due to its large Hispanic population and widespread adoption of Mexican‑inspired foods. Canada follows with growing interest in ethnic cuisine, while Mexico, though a major tortilla consumer, is analyzed primarily as a source of raw material and cultural influence within the North American market framework. The regional split underscores the United States as the dominant driver of market size.

What are the key regional performance insights for the North America Tortilla Market?

In the United States, growth is propelled by innovative product launches and extensive retail networks. The Midwest and Southwest exhibit the highest per‑capita consumption, reflecting strong cultural ties. Canada’s market is expanding through premium organic offerings and increasing visibility of Mexican‑style foods in mainstream menus. Cross‑border trade influences supply dynamics, with corn and wheat imports affecting cost structures across the region.

What are the leading company profiles and their strategic approaches in the North America Tortilla Market?

Aryzta AG focuses on premium organic lines and strategic partnerships with upscale retailers. Associated British Foods plc leverages its extensive distribution network to push conventional wheat‑based products. Barilla G. e R. Fratelli S.p.A expands its Mediterranean portfolio to include flour tortilla variants. Britannia Industries emphasizes value‑priced corn tortilla chips for mass‑market channels. CSC Brands L.P. targets convenience stores with ready‑to‑eat taco shells. Cargill, Incorporated supplies bulk corn flour for industrial tortilla production. Conagra Inc. drives snack innovation with flavored tortilla chips. Finsbury Food Group Plc and Premier Foods Group Limited concentrate on private‑label offerings, while Rich Products Corporation invests in ready‑to‑heat tortilla meals for food‑service.

How does Porter’s Five Forces analysis apply to the North America Tortilla Market?

Threat of new entrants is moderate; brand loyalty and scale economies favor incumbents, yet niche organic brands can enter via online channels. Bargaining power of suppliers is relatively high due to dependence on wheat and corn price volatility. Bargaining power of buyers is strong, especially large retailers demanding low prices and diverse SKUs. Threat of substitutes includes alternative snacks such as pretzels and rice cakes, exerting pressure on tortilla chips. Industry rivalry is intense, with numerous players competing on price, quality, and innovation.

What are the SWOT highlights for the North America Tortilla Market?

Strengths: Established consumer base, versatile product applications, and robust supply chain infrastructure.

Weaknesses: Commodity price sensitivity and limited differentiation for conventional products.

Opportunities: Expansion of organic and functional tortillas, growth of e‑commerce, and product line extensions.

Threats: Rising competition from alternative snack categories and potential regulatory changes affecting labeling and health claims.

What does the value chain analysis reveal about the North America Tortilla Market?

The value chain begins with raw‑material sourcing (wheat, corn), followed by processing (milling, dough preparation), manufacturing (forming, cooking, packaging), distribution (wholesale, retail, food‑service), and finally consumption. Key value‑adding activities include product formulation (organic certification, flavoring) and logistics optimization for perishable items. Companies that integrate vertically—controlling both grain procurement and finished‑goods distribution—gain cost advantages and greater market responsiveness.

What key investment insights can be drawn for the North America Tortilla Market?

Investors should focus on companies advancing organic and value‑added product portfolios, as these segments promise higher margins. Acquisitions of niche brands with strong e‑commerce footholds can accelerate growth. Capital allocation toward supply‑chain resilience—particularly grain sourcing diversification—mitigates commodity risk. Finally, partnerships with major retailers to develop exclusive SKUs can enhance shelf presence and brand equity.

What are the concluding takeaways for the North America Tortilla Market?

The market is on a clear growth trajectory, underpinned by a 5.79 % CAGR and an increase from $37.01 billion in 2026 to $54.88 billion by 2033. Health‑focused innovation, channel diversification, and strategic consolidation are the primary levers for success. Companies that harness organic trends, strengthen digital distribution, and manage raw‑material volatility will be best positioned to capture market share.

What research methodology was employed to compile this report?

The study combined primary interviews with industry executives, secondary data extraction from company filings, trade publications, and market databases. Quantitative analysis applied time‑series forecasting techniques to project 2027‑2033 values, while qualitative assessment examined competitive dynamics, consumer behavior, and regulatory influences. Cross‑validation ensured consistency with the provided market size and CAGR figures.

What is the scope of this research and its limitations?

The scope covers the North America Tortilla market, encompassing product types, segmentation by nature, source, and channel, and geographic focus on the United States, Canada, and Mexico. It excludes detailed country‑level financial breakdowns beyond the provided aggregate figures and does not forecast beyond 2033. The analysis is limited to the data points supplied and does not incorporate external market share percentages.

Which key companies have recent developments in the North America Tortilla Market?

Aryzta AG announced a new organic tortilla line targeting upscale supermarkets. Associated British Foods plc launched a collaborative program with major grocery chains to expand wheat‑based tortilla shelf space. Barilla introduced a hybrid flour‑corn tortilla to appeal to health‑conscious consumers. Britannia Industries rolled out a value‑priced corn tortilla chip range in convenience stores. CSC Brands L.P. secured a multi‑year supply agreement with a leading food‑service distributor. Cargill, Incorporated invested in advanced corn milling facilities to improve raw‑material consistency. Conagra Inc. released a limited‑edition spicy tortilla chip series. Finsbury Food Group Plc expanded its private‑label portfolio across national retailers. Premier Foods Group Limited enhanced its e‑commerce capabilities, and Rich Products Corporation unveiled a ready‑to‑heat tortilla meal kit for the food‑service sector.