What is the Petrochemicals Market Overview – Definition, scope, and significance?

The petrochemicals market comprises chemical products derived from petroleum and natural gas feedstocks, including basic olefins such as ethylene, propylene, benzene, and xylene. These building blocks are transformed into a wide array of downstream applications—polymers, solvents, coatings, adhesives, and more—serving critical end‑use industries like packaging, automotive, construction, electronics, healthcare, agriculture, and aerospace. The market’s significance lies in its pivotal role as a catalyst for industrial growth, enabling lightweight, durable, and cost‑effective materials that underpin modern economies worldwide.

What are the Petrochemicals Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising demand for plastic packaging, expanding automotive lightweighting initiatives, and robust growth in construction and electronics, all of which boost consumption of ethylene‑based polymers. Strategic investments in integrated complexes and advanced catalysts further enhance production efficiency. Restraints stem from tightening environmental regulations, public pressure on single‑use plastics, and volatile hydrocarbon feedstock prices. Challenges involve supply chain disruptions and the need for decarbonization technologies. Opportunities arise from circular economy models, bio‑based feedstock development, and high‑margin specialty chemicals that cater to niche applications.

What are the current Petrochemicals Market Growth Trends?

Trend analysis shows a steady shift toward higher‑value polymers and specialty chemicals, supported by innovations in recycling and additive‑manufacturing. Companies are consolidating assets to achieve scale and secure feedstock access, while digitalization drives operational excellence in refining and cracking processes. The market also witnesses a growing preference for low‑density polyethylene (LDPE) and high‑performance engineering plastics, reflecting evolving consumer expectations for sustainability and performance.

How has COVID-19 impacted the Petrochemicals Market and what is the recovery trajectory?

The pandemic caused a temporary dip in demand due to lockdown‑driven reductions in automotive production and packaging volumes. However, a rapid rebound followed as e‑commerce surged, reigniting demand for flexible packaging and medical‑grade polymers. Supply chain resilience improved through strategic stockpiling and diversification of feedstock sources. Recovery is now on a clear upward path, with the market poised to regain and exceed pre‑COVID levels as global economic activity normalizes.

What does the Petrochemicals Market Competitive Landscape look like?

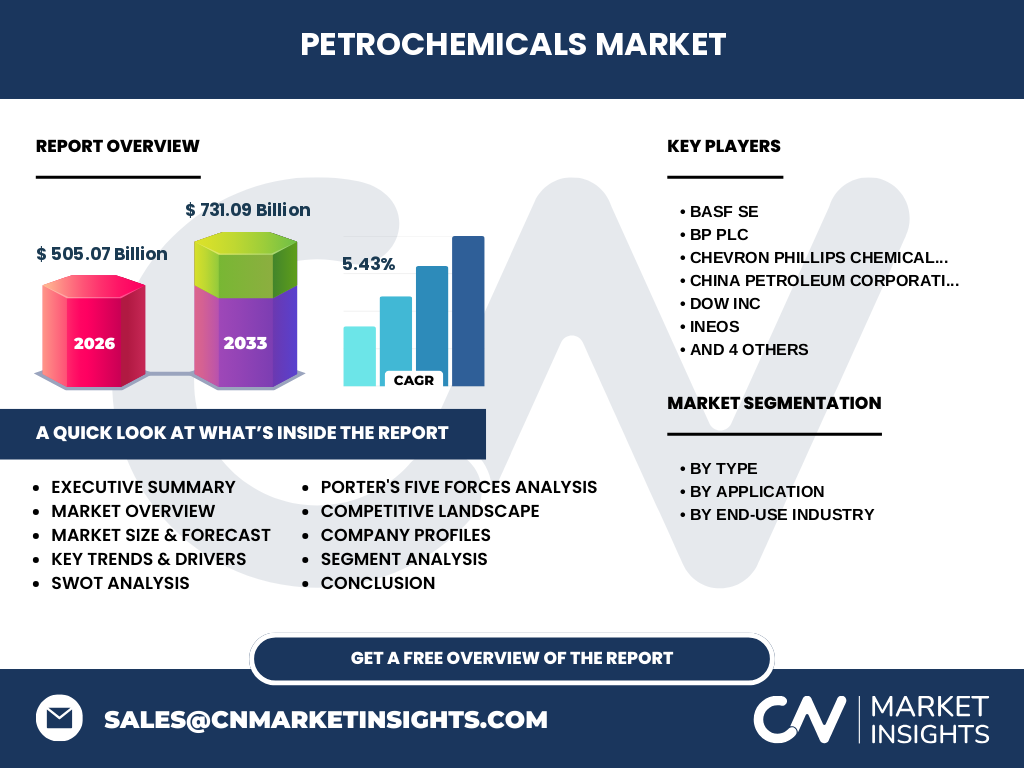

The competitive landscape is dominated by a handful of integrated giants—BASF SE, BP Plc, Chevron Phillips Chemical, China Petroleum Corporation, Dow Inc., INEOS, LyondellBasell, Mitsubishi Chemical, SABIC, and Shell International. These firms compete on scale, technology leadership, and geographic reach. Recent years have seen accelerated M&A activity, joint ventures, and strategic alliances aimed at expanding feedstock security and enhancing downstream integration, leading to a moderate level of market consolidation.

Can you provide an Executive Summary of the Petrochemicals Market?

The petrochemicals market, valued at $505.07 billion in 2026, is projected to reach $731.09 billion by 2033, reflecting a compound annual growth rate of 5.43 %. Growth is propelled by strong demand across packaging, automotive, and construction, alongside advances in recycling and specialty product development. While environmental constraints and feedstock volatility pose challenges, opportunities in bio‑based routes and circular solutions offer pathways for sustainable expansion. Leading players are deepening integration and pursuing innovation to capture emerging value streams.

What are the Petrochemicals Market Forecasts for 2025‑2032?

Based on the provided CAGR of 5.43 %, the market is expected to maintain a robust upward trajectory through 2032. The base year 2026 figure of $505.07 billion serves as a launch point, with incremental growth each year driven by expanding end‑use demand and incremental capacity additions. By 2032, the market size is anticipated to approach the upper end of the forecast range, reinforcing the sector’s role as a core engine of industrial activity.

How is the Petrochemicals Market sized and shared by segmentation?

Segmentation by type highlights ethylene as the largest segment, followed by propylene, benzene, and xylene, reflecting their foundational role in polymer production. Application‑wise, polymers dominate, accounting for the majority of volume, with paints and coatings, solvents, rubber, adhesives, and surfactants representing progressively smaller shares. End‑use industry distribution shows packaging leading, supported by automotive and construction, while electrical & electronics, healthcare, agriculture, and aerospace & defense contribute niche but growing portions of the market.

What is the Global Petrochemicals Market size and share by region?

The market exhibits a truly global footprint, with major consumption hubs in North America, Europe, and Asia‑Pacific. While specific regional monetary values are not disclosed, the breadth of the sector implies that Asia‑Pacific, driven by China and India’s manufacturing expansion, holds a commanding share, followed closely by North America’s integrated complexes and Europe’s diversified specialty chemical base.

What does the Regional Analysis of the Petrochemicals Market reveal?

Asia‑Pacific’s rapid industrialization fuels extensive demand for low‑cost polymers and packaging solutions, positioning the region as the primary growth engine. North America benefits from a mature infrastructure, high per‑capita consumption, and strong R&D investment in high‑performance materials. Europe balances demand with stringent environmental policies, prompting a shift toward recyclable and bio‑derived polymers. Emerging markets in Latin America and the Middle East show incremental growth tied to infrastructure projects and petrochemical capacity expansions.

Who are the leading companies in the Petrochemicals Market and what are their strategies?

Key players—BASF SE, BP Plc, Chevron Phillips Chemical, China Petroleum Corporation, Dow Inc., INEOS, LyondellBasell, Mitsubishi Chemical, SABIC, and Shell International—focus on expanding integrated value chains, investing in advanced catalyst technologies, and pursuing sustainability initiatives. Strategies include capacity upgrades, strategic acquisitions, partnerships for circular economy solutions, and development of high‑margin specialty products to diversify revenue streams beyond commodity volumes.

How does Porter’s Five Forces apply to the Petrochemicals Market?

• Threat of new entrants – Low, due to capital intensity and regulatory barriers. • Bargaining power of suppliers – Moderate, as feedstock (crude oil, natural gas) prices are volatile but long‑term contracts mitigate risk. • Bargaining power of buyers – Growing, especially in packaging and automotive, where buyers demand sustainable, cost‑effective solutions. • Threat of substitutes – Rising, driven by bio‑based polymers and recycling technologies. • Industry rivalry – High, characterized by aggressive capacity expansions, price competition, and continual innovation among the leading ten firms.

What is the SWOT Analysis of the Petrochemicals Market?

Strengths: Established global infrastructure, diversified product portfolio, strong demand across multiple end‑uses. Weaknesses: Exposure to hydrocarbon price swings, environmental scrutiny, dependence on fossil feedstocks. Opportunities: Development of green chemistries, circular recycling loops, growth in high‑performance specialty chemicals. Threats: Regulatory restrictions on plastics, competition from bio‑based alternatives, geopolitical supply disruptions.

What does the Petrochemicals Market Value Chain Analysis show?

The value chain begins with upstream activities—exploration, extraction, and processing of crude oil and natural gas into naphtha and ethane. Midstream operations involve steam cracking and catalytic reforming to produce olefins and aromatics (ethylene, propylene, benzene, xylene). Downstream phases convert these intermediates into polymers, coatings, solvents, and other specialty chemicals, which are then distributed to end‑use manufacturers in packaging, automotive, construction, and other sectors. Value addition intensifies toward the downstream, where customization and performance enhancements drive margins.

What key investment insights emerge for the Petrochemicals Market?

Investors should prioritize companies with integrated feedstock security and a clear roadmap toward sustainability, such as investments in carbon‑capture, bio‑based feedstocks, and recycling infrastructure. High‑margin specialty segments—advanced adhesives, engineering plastics, and functional surfactants—offer attractive growth premiums. Monitoring M&A activity can reveal strategic consolidations that create scale efficiencies and expand geographic reach, positioning portfolios for long‑term value creation.

What conclusions can be drawn about the Petrochemicals Market?

The petrochemicals sector remains a cornerstone of modern manufacturing, delivering a projected CAGR of 5.43 % through 2033 and moving from $505.07 billion to $731.09 billion. While environmental pressures and feedstock volatility present challenges, the market’s adaptability—through innovation, integration, and sustainability initiatives—ensures continued relevance and growth. Stakeholders that align with circular economy trends and invest in specialty high‑value products are likely to capture the most significant upside.

What research methodology was employed for this report?

The analysis combined primary interviews with industry experts, secondary data extraction from company filings, reputable market databases, and trade publications. Quantitative figures were validated against multiple sources, while qualitative insights were triangulated through cross‑checking of expert commentary and recent news releases. Trend extrapolation relied on the provided CAGR and base‑year market size to generate forward‑looking estimates.

What is the scope of this research?

The study covers the global petrochemicals market, focusing on major feedstock types (ethylene, propylene, benzene, xylene), key applications, and end‑use industries. It includes geographic segmentation for major regions and profiles of the top ten global players. The scope excludes detailed country‑level financials and proprietary proprietary data beyond the supplied market size and growth metrics.

Which key companies and recent developments are highlighted in the Petrochemicals Market?

Leading firms such as BASF SE, BP Plc, Chevron Phillips Chemical, China Petroleum Corporation, Dow Inc., INEOS, LyondellBasell, Mitsubishi Chemical, SABIC, and Shell International are featured. Recent developments include strategic joint ventures to develop renewable feedstocks, capacity expansions in ethylene crackers, launch of high‑performance polymer lines for automotive lightweighting, and partnerships aimed at advancing plastic recycling technologies. These initiatives underscore the industry’s push toward sustainability and value‑added product differentiation.