What is the Water Treatment Biocides Market Overview – definition, scope, and significance?

The Water Treatment Biocides market encompasses chemicals designed to control the growth of microorganisms in water systems used for municipal supply, industrial processes, and recreational facilities. These biocides protect infrastructure, ensure compliance with health regulations, and maintain operational efficiency by preventing bio‑fouling, corrosion, and taste‑odor issues. Their scope spans a wide range of applications—from large‑scale power plants to swimming pools—making them essential for public health, environmental protection, and cost‑effective water management.

What are the key drivers, restraints, challenges, and opportunities influencing the Water Treatment Biocides Market?

Growth is driven by increasing urbanization, stricter water quality regulations, and the expansion of industrial sectors such as oil & gas and mining that require reliable microbial control. Restraints include rising concerns over the environmental impact of certain biocides and the regulatory scrutiny of hazardous chemicals. Challenges involve the need for sustainable, low‑toxicity alternatives and the complexity of selecting appropriate biocides for diverse water chemistries. Opportunities arise from the development of green biocides, digital monitoring technologies, and emerging markets investing in water infrastructure.

What are the current and emerging growth trends shaping the Water Treatment Biocides Market?

Current trends highlight a shift toward non‑oxidizing biocides for their stability and lower by‑product formation, alongside a continued demand for oxidizing biocides in high‑temperature applications. Emerging trends include the integration of smart dosing systems that adjust biocide levels in real time, the rise of bio‑based and biodegradable biocides, and increasing adoption of combined treatment packages that pair biocides with advanced oxidation processes to enhance overall efficacy.

How has COVID‑19 impacted the Water Treatment Biocides Market and what is the recovery trajectory?

The pandemic temporarily slowed capital projects and disrupted supply chains, leading to a short‑term dip in demand for new installations. However, heightened awareness of hygiene and water safety accelerated the adoption of effective biocides in healthcare facilities and public water systems. Recovery is now robust, supported by renewed infrastructure spending and a resurgence in industrial activity, positioning the market for sustained growth.

What does the competitive landscape of the Water Treatment Biocides Market look like?

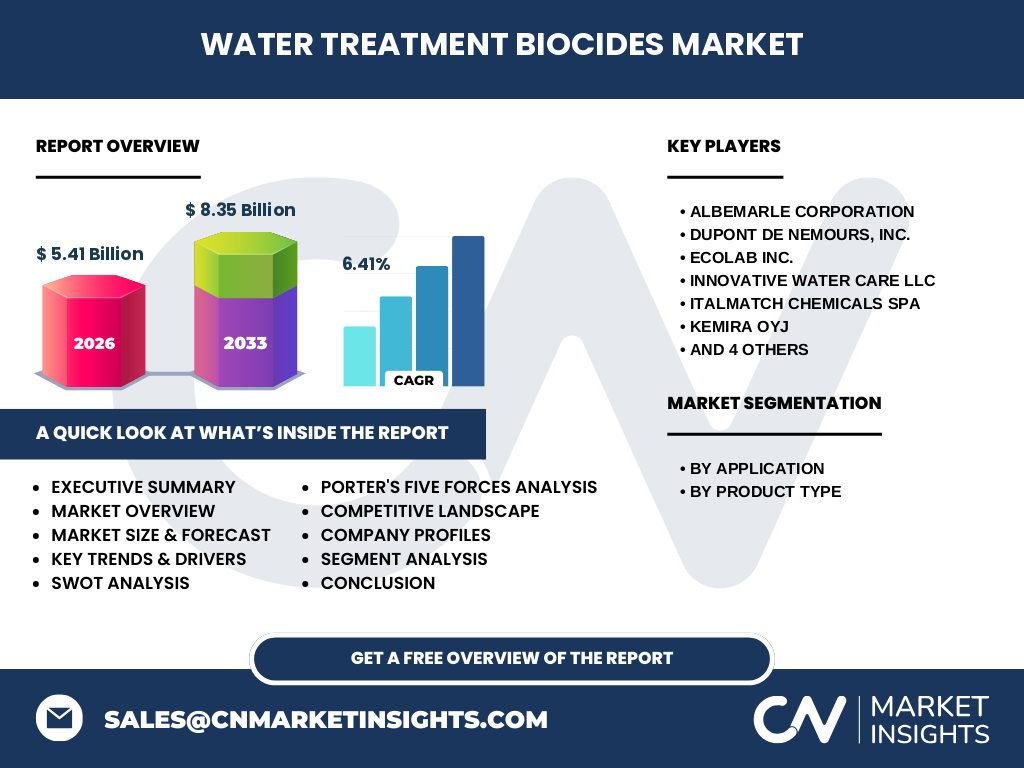

The market is moderately consolidated, featuring several global chemical leaders and specialist firms. Key competitors such as Albemarle Corporation, DuPont de Nemours, Inc., and Ecolab Inc. dominate through extensive product portfolios and strong distribution networks. Recent consolidation activity includes strategic acquisitions and joint ventures aimed at expanding geographic reach and enhancing product innovation, intensifying competition on technology and service quality.

What are the high‑level insights and key findings from the Water Treatment Biocides market executive summary?

The market is valued at $5.41 billion in 2026 and is projected to reach $8.35 billion by 2033, reflecting a 6.41 % CAGR. Growth is propelled by regulatory pressure, infrastructure development, and the demand for safer, more effective biocidal solutions across multiple sectors. Innovation in non‑oxidizing and environmentally friendly biocides, coupled with digital dosing technologies, offers a clear pathway for companies to capture value and differentiate themselves.

What are the forecast expectations for the Water Treatment Biocides Market from 2025 to 2032?

Based on the projected CAGR of 6.41 %, the market is expected to expand steadily, reaching the forecasted $8.35 billion figure by 2033. The forecast period will likely see increased penetration of biocides in emerging economies, continued adoption of advanced dosing systems, and a gradual shift toward greener formulations, all contributing to consistent revenue growth.

How is the Water Treatment Biocides market sized and shared by application and product type?

Segmented by application, the market serves municipal water treatment, oil & gas, power plants, pulp and paper, mining, and swimming pools. By product type, it is divided between oxidizing biocides, which are favored for high‑temperature and high‑pH environments, and non‑oxidizing biocides, preferred for stability and lower toxicity. Both segments capture significant demand, reflecting the diverse operational requirements across end‑use industries.

What is the global geographic distribution of the Water Treatment Biocides market?

The market exhibits a worldwide presence, with strong demand in North America and Europe due to stringent water quality standards, while Asia‑Pacific shows the fastest growth driven by rapid urbanization and industrialization. Latin America and the Middle East & Africa present emerging opportunities as water infrastructure investments increase.

What are the detailed regional performances within the Water Treatment Biocides market?

In North America, mature regulatory frameworks and extensive industrial activity sustain high adoption rates. Europe balances strict environmental regulations with innovative product development, especially in the non‑oxidizing segment. Asia‑Pacific’s expanding municipal water networks and booming oil & gas sector drive the fastest uptake. Latin America benefits from growing mining operations, and the Middle East & Africa see rising investments in desalination and water reuse projects.

Which leading companies operate in the Water Treatment Biocides market and what are their strategic approaches?

Key players include Albemarle Corporation, DuPont de Nemours, Inc., Ecolab Inc., Innovative Water Care LLC, Italmatch Chemicals SpA, Kemira OYJ, Nouryon, Solenis, Suez, and Veolia. Their strategies focus on expanding product portfolios, investing in R&D for eco‑friendly biocides, forming strategic alliances, and leveraging digital platforms for customer support and dosing optimization.

How does Porter’s Five Forces analysis apply to the Water Treatment Biocides market?

• Threat of new entrants is moderate due to high R&D costs and regulatory barriers. • Bargaining power of suppliers is low, as raw material sources are diversified. • Buyer power is significant, with utilities and large industrial users demanding cost‑effective, compliant solutions. • Threat of substitutes is limited, given the unique efficacy of biocides compared with physical cleaning methods. • Competitive rivalry is intense, driven by product innovation and service differentiation.

What are the strengths, weaknesses, opportunities, and threats identified in the SWOT analysis of the Water Treatment Biocides market?

Strengths: Established demand, regulatory support, and diverse applications.

Weaknesses: Environmental concerns and reliance on chemical synthesis.

Opportunities: Development of biodegradable biocides, digital dosing, and expansion into emerging economies.

Threats: Stricter environmental legislation and potential shifts toward alternative water treatment technologies.

What does the value chain of the Water Treatment Biocides market look like?

The value chain begins with raw material procurement (e.g., chlorine, phosphorous compounds), followed by chemical synthesis and formulation. Next, manufacturers conduct rigorous testing for efficacy and regulatory compliance. Distribution channels include direct sales to large utilities, distributors, and specialized service providers. End‑users apply biocides through automated dosing systems, supported by after‑sales service and technical consulting.

What key investment insights can be drawn for stakeholders in the Water Treatment Biocides market?

Investors should prioritize companies with strong R&D pipelines focused on low‑toxicity, high‑performance biocides and those adopting digital dosing platforms. Strategic acquisitions in emerging regions can accelerate market entry, while partnerships with engineering firms enhance service offerings. Monitoring regulatory trends will be crucial for aligning product development with future compliance requirements.

What are the main conclusions of the Water Treatment Biocides market analysis?

The market is on a solid growth trajectory, underpinned by regulatory imperatives and expanding water infrastructure worldwide. Both oxidizing and non‑oxidizing biocides will remain essential, but a shift toward greener, more sustainable solutions is evident. Companies that innovate in product safety, digital integration, and regional expansion are poised to capture the greatest share of the anticipated $8.35 billion market by 2033.

How was the research for this Water Treatment Biocides market report conducted?

The study combined primary interviews with industry experts, secondary data from reputable market databases, regulatory publications, and company financials. Trend analysis, forecasting models, and competitive benchmarking were applied to ensure accuracy and relevance of the insights presented.

What is the scope of this research and its limitations?

The research covers global market size, segmentation by application and product type, regional performance, and competitive dynamics. Limitations include the reliance on publicly available data and estimates for future periods, which may be affected by unforeseen regulatory or economic changes.

Which key companies have made recent developments in the Water Treatment Biocides market?

Recent activities include Albemarle’s launch of a new non‑oxidizing biocide line, DuPont’s partnership with a digital dosing technology provider, Ecolab’s acquisition of a specialty biocide manufacturer, and Veolia’s expansion of its water treatment services in Asia‑Pacific. These moves illustrate a focus on product innovation, geographic growth, and integrated service solutions.