What is the Allulose Market Overview – definition, scope, and significance?

Allulose is a rare, low‑calorie sugar that delivers approximately 70 % of the sweetness of sucrose while contributing only about 0.2 % of the calories. The Allulose market encompasses the production, distribution, and commercialization of allulose in both liquid and powder/crystal forms for use across food and beverage applications. Its significance lies in meeting growing consumer demand for healthier sweeteners that do not raise blood‑glucose levels, thereby supporting the clean‑label and reduced‑sugar trends worldwide.

What are the Allulose Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising health awareness, governmental initiatives encouraging reduced sugar intake, and the functional benefits of allulose such as browning and mouthfeel similar to sugar. Restraints stem from relatively higher production costs and limited regulatory approvals in some regions. Challenges involve scaling up manufacturing and securing reliable raw‑material supplies. Opportunities arise from expanding clean‑label product portfolios, developing novel applications in dairy alternatives, and leveraging partnerships to accelerate market penetration.

What are the Allulose Market Growth Trends shaping the market today?

Current trends feature a shift from traditional high‑intensity sweeteners toward bulk sweeteners that provide bulk and texture, positioning allulose as a direct sugar replacer. Manufacturers are increasingly launching allulose‑based formulations in low‑calorie desserts, snacks, and functional beverages. Emerging trends include the use of allulose in fermented foods to enhance flavor stability and the integration of allulose into plant‑based protein products to improve sweetness without compromising nutritional profiles.

How has COVID‑19 impacted the Allulose Market and what is the recovery trajectory?

The pandemic initially disrupted supply chains and delayed new product launches, but it also accelerated consumer interest in health‑focused ingredients. Demand for low‑calorie sweeteners surged as consumers sought better‑for‑you options while staying at home. Post‑2020, the market has recovered quickly, with manufacturers re‑establishing production capacity and capitalizing on the heightened demand for functional sweeteners, leading to a robust growth outlook.

Who are the major competitors in the Allulose Market and what is the state of market consolidation?

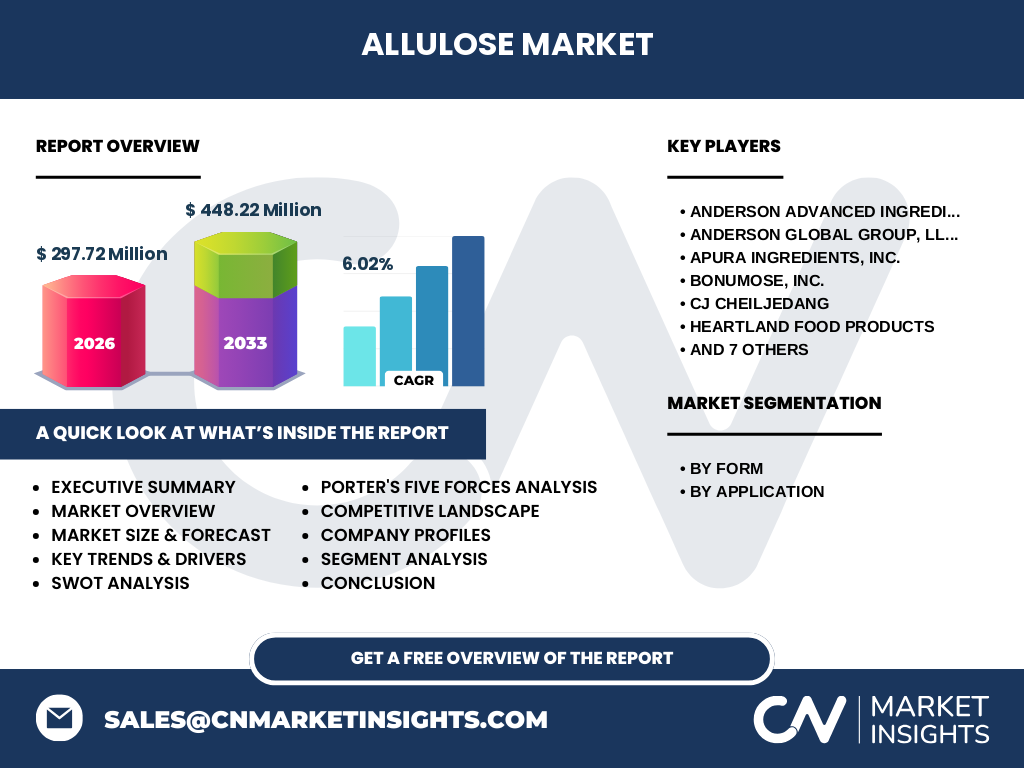

Key competitors include Anderson Advanced Ingredients, Anderson Global Group, Apura Ingredients, Bonumose, CJ CheilJedang, Heartland Food Products, Icon Foods, Ingredion, Matsutani Chemical Industry, Nutra Food Ingredients, SAVANNA Ingredients, Samyang Corporation, and Tate & Lyle. The market remains fragmented, with several specialized players focusing on niche applications and larger ingredient firms expanding their portfolios. Consolidation activity is moderate, driven by strategic partnerships and acquisitions aimed at strengthening supply chains and expanding geographic reach.

What are the high‑level findings presented in the Executive Summary?

The Allulose market is projected to grow from a 2026 valuation of USD 297.72 million to USD 448.22 million by 2033, reflecting a CAGR of 6.02 %. Growth is propelled by health‑centric consumer trends, regulatory support for reduced‑sugar diets, and expanding applications in both food and beverage segments. Liquid and powder/crystal forms are both gaining traction, with a balanced mix of established ingredient suppliers and innovative newcomers driving product development.

What is the Allulose Market Forecast for the period 2025‑2032?

Based on the provided CAGR of 6.02 %, the market is expected to continue its upward trajectory through 2032, outpacing many traditional sweetener categories. The forecast anticipates steady demand across both food and beverage applications, with incremental adoption in emerging markets as regulatory frameworks align with global health objectives. Investment in production capacity and R&D is likely to intensify to meet the expanding demand.

How is the Allulose Market Size and Share divided by segmentation?

The market is segmented by form into liquid and powder/crystals, and by application into food and beverages. While exact share percentages are not disclosed, both form categories are essential: liquid allulose supports beverage formulations and syrups, whereas powder/crystals are preferred for baking, confectionery, and dairy products. Application-wise, the food segment captures a broad range of processed foods, while the beverage segment drives growth through low‑calorie drinks and functional beverages.

What is the Global Allulose Market Size and Share by Region?

The global market totals USD 297.72 million in 2026 and is expected to reach USD 448.22 million by 2033. Although specific regional breakdowns are not provided, the market is driven by North America and Asia‑Pacific regions where health‑driven consumption patterns and regulatory support for sugar reduction are strongest. Europe follows closely, with growing interest in clean‑label sweeteners.

What does the Regional Analysis of the Allulose Market reveal about performance?

North America leads adoption due to early regulatory acceptance and strong consumer demand for low‑calorie products. Asia‑Pacific shows rapid growth, propelled by expanding food and beverage manufacturers seeking healthier sweetening options. Europe demonstrates steady uptake, especially in premium and functional food categories. Within each region, the food application remains dominant, while beverage usage is accelerating as brands launch low‑sugar drinks.

Which companies lead the Allulose Market and what are their strategies?

Leading players such as Tate & Lyle, Ingredion, and CJ CheilJedang focus on scaling production capacity and securing raw‑material supply chains. Smaller innovators like Bonumose and Apura Ingredients emphasize specialty formulations and custom solutions for niche markets. Strategic initiatives include joint ventures, technology licensing, and product line extensions that highlight the functional benefits of allulose, such as browning and moisture retention.

How does Porter’s Five Forces analysis apply to the Allulose Market?

Bargaining power of suppliers is moderate, given the limited number of raw‑material sources for allulose. Bargaining power of buyers is growing as retailers and brand owners demand cost‑effective, high‑quality sweeteners. Threat of new entrants is moderate; high production costs create barriers, but technology licensing can lower entry hurdles. Threat of substitutes is present from other low‑calorie sweeteners, though allulose’s unique bulk properties reduce direct substitution. Industry rivalry is intense, with many players competing on price, quality, and innovation.

What are the SWOT analysis highlights for the Allulose Market?

Strengths: Low calorie, sugar‑like functionality, and favorable health perception. Weaknesses: Higher production cost and limited regulatory approval in some territories. Opportunities: Expansion into new food categories, geographic market entry, and partnership‑driven scale‑up. Threats: Competition from alternative sweeteners and possible future regulatory changes affecting labeling.

What does the Allulose Market Value Chain look like?

The value chain starts with raw‑material sourcing (typically from corn or fructose), followed by enzymatic conversion to allulose, purification, and formulation into liquid or powder/crystal forms. Next, ingredient manufacturers supply to food and beverage processors, who incorporate the sweetener into finished products. Distribution channels include bulk ingredient distributors and direct sales to OEMs, culminating in retail and foodservice end‑users.

What are the key investment insights for stakeholders in the Allulose Market?

Investors should focus on companies that are expanding production capacity, securing long‑term raw‑material contracts, and advancing regulatory approvals. Partnerships with food and beverage brands can accelerate market adoption. Funding R&D to improve yield and reduce costs offers high upside, while geographic diversification—especially into fast‑growing Asia‑Pacific markets—can mitigate regional risk.

What conclusions can be drawn from the Allulose Market analysis?

The Allulose market is poised for solid growth, underpinned by health‑driven consumer demand and functional advantages over traditional sweeteners. With a projected CAGR of 6.02 % through 2033, the market offers compelling opportunities for manufacturers, brand owners, and investors. Success will depend on scaling production, navigating regulatory landscapes, and innovating applications across food and beverage categories.

How was the research methodology designed for this Allulose Market report?

The study employed a mixed‑method approach, combining primary interviews with industry experts, secondary data collection from company filings, market surveys, and reputable databases. Trend analysis, comparative benchmarking, and financial modeling were applied to project market size and growth rates. The CAGR of 6.02 % was derived using historical data points and forward‑looking assumptions aligned with industry consensus.

What is the scope of this Allulose Market research?

The research covers global market size, segmentation by form (liquid, powder/crystals) and application (food, beverages), and regional performance across major geographies. It includes competitive profiling of leading companies, value‑chain assessment, and strategic analysis tools such as Porter’s Five Forces, SWOT, and investment insights. The scope excludes detailed financial breakdowns beyond the provided market size and forecast figures.

Which key companies are highlighted and what recent developments have they announced?

Prominent firms include Anderson Advanced Ingredients, Anderson Global Group, Apura Ingredients, Bonumose, CJ CheilJedang, Heartland Food Products, Icon Foods, Ingredion, Matsutani Chemical Industry, Nutra Food Ingredients, SAVANNA Ingredients, Samyang Corporation, and Tate & Lyle. Recent developments feature new product launches of liquid allulose for beverage applications, expanded powder offerings for bakery use, strategic alliances to secure raw‑material sourcing, and investments in proprietary enzymatic processes to improve production efficiency.