What is the Pharmaceutical Continuous Manufacturing Market Overview - definition, scope, and significance?

Pharmaceutical continuous manufacturing (PCM) refers to the end‑to‑end production approach in which active pharmaceutical ingredients (APIs) and final dosage forms are synthesized, processed, and packaged on a single, uninterrupted production line. The scope embraces integrated hardware, semi‑continuous equipment, and advanced control systems used by both full‑scale manufacturers and research & development departments for API synthesis and finished‑product fabrication. Its significance lies in accelerating time‑to‑market, improving product quality, reducing waste, and enabling real‑time release testing, thereby reshaping traditional batch‑centric drug production.

What are the main drivers, restraints, challenges, and opportunities in the Pharmaceutical Continuous Manufacturing Market?

Key drivers include regulatory encouragement for quality‑by‑design, rising demand for personalized medicines, and pressure to cut manufacturing costs. Restraints stem from high upfront capital investment and limited skilled workforce familiar with continuous processes. Challenges involve integration with legacy batch facilities, validation complexities, and supply‑chain synchronization. Opportunities arise from emerging digital twin technologies, expansion into biologics continuous production, and increasing collaborations between equipment suppliers and pharmaceutical firms to lower adoption barriers.

What growth trends are currently shaping the Pharmaceutical Continuous Manufacturing Market?

Current trends feature rapid adoption of modular integrated systems that combine synthesis, filtration, and granulation in a single line. Semi‑continuous platforms are gaining traction for niche APIs where full continuity is not yet feasible. Advanced process analytical technology (PAT) and AI‑driven controls are emerging to enable real‑time monitoring. Additionally, the market is seeing a shift toward sustainability, with manufacturers seeking energy‑efficient continuous lines that lower solvent usage.

How has COVID‑19 impacted the Pharmaceutical Continuous Manufacturing Market and what is the recovery trajectory?

The pandemic highlighted the need for resilient, flexible production capacity, accelerating interest in continuous manufacturing to quickly ramp up vaccine and therapeutic output. Supply‑chain disruptions prompted firms to re‑evaluate batch‑centric facilities, leading to pilot projects and early‑stage deployments of continuous lines. Post‑COVID recovery is steady, with investment pipelines restored and a clear roadmap to expand continuous platforms through 2025, supporting a robust growth outlook.

Who are the major competitors in the Pharmaceutical Continuous Manufacturing Market and what is the competitive landscape?

The market is fragmented yet highly competitive, featuring technology leaders such as ACG, Alexanderwerk, Coperion GmbH, GEA Group, Glatt GmbH, and Thermo Fisher Scientific Inc. These firms differentiate through integrated system offerings, patented control algorithms, and strategic partnerships with pharma companies. Recent consolidation includes joint ventures and acquisitions aimed at broadening product portfolios and enhancing global service networks, fostering a competitive environment focused on innovation and customer support.

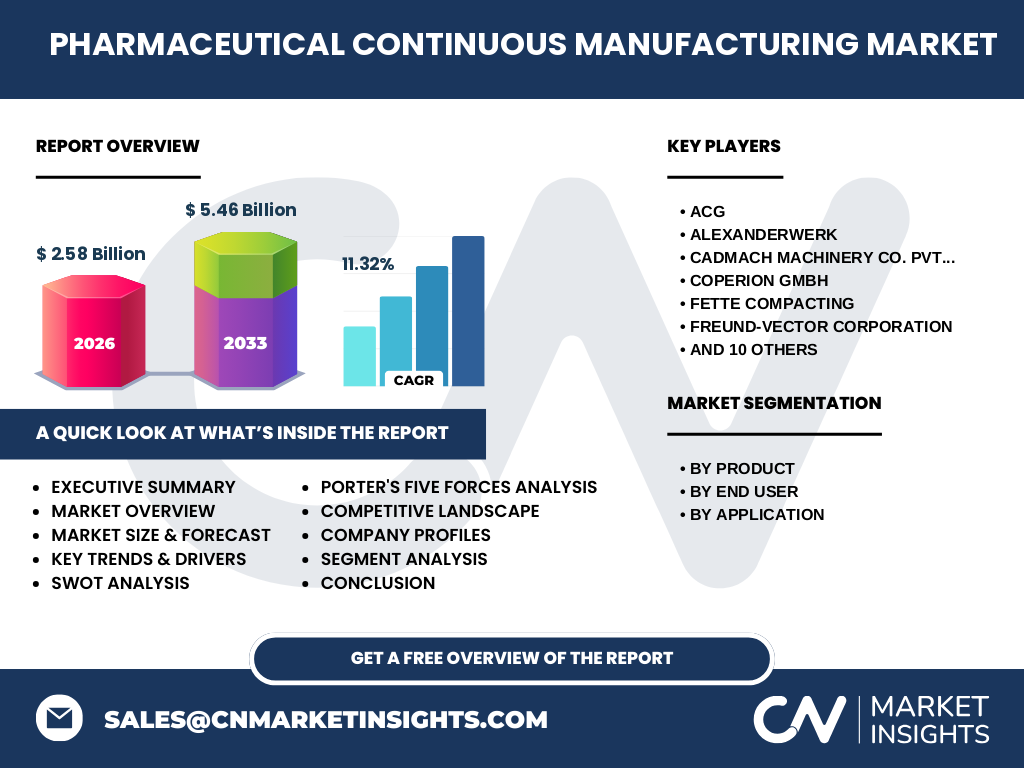

What are the key findings in the Executive Summary of the Pharmaceutical Continuous Manufacturing Market?

The market is valued at $2.58 billion in 2026 and is projected to reach $5.46 billion by 2033, reflecting a CAGR of 11.32 %. Growth is driven by regulatory incentives, cost‑efficiency imperatives, and digitalization. Integrated systems dominate the product segment, while full‑scale manufacturers represent the largest end‑user base. Geographic expansion is evident across North America, Europe, and Asia‑Pacific, with increasing investments in R&D departments accelerating innovation pipelines.

What is the forecast for the Pharmaceutical Continuous Manufacturing Market from 2025 to 2032?

Based on the provided figures, the market is expected to more than double, moving from $2.58 billion in 2026 to $5.46 billion by 2033. This trajectory implies sustained double‑digit expansion throughout the 2025‑2032 period, underpinned by continuous adoption of integrated and semi‑continuous systems, heightened focus on API manufacturing efficiency, and broader implementation of advanced controls across the pharmaceutical value chain.

How is the Pharmaceutical Continuous Manufacturing Market sized and shared by product, end‑user, and application segments?

Segmentation reveals three product categories: Integrated Systems, Semi‑Continuous Systems, and Controls. Integrated Systems command the largest share due to their end‑to‑end capability, while Controls are gaining importance as manufacturers invest in real‑time monitoring. End‑users split between Full‑Scale Manufacturing Companies, which drive the bulk of volume, and R&D Departments, which spearhead pilot and validation projects. Application-wise, End Product Manufacturing leads the market, followed closely by API Manufacturing, reflecting the dual need for continuous dosage‑form and ingredient production.

What is the global geographic distribution of the Pharmaceutical Continuous Manufacturing Market?

The market exhibits strong presence in North America and Europe, where regulatory frameworks and mature pharmaceutical ecosystems encourage early adoption. Asia‑Pacific is emerging rapidly, driven by expanding drug pipelines and government incentives for advanced manufacturing. While exact regional revenue numbers are not disclosed, the overall growth pattern shows balanced expansion across these key regions, supported by local equipment manufacturers and multinational service providers.

What are the detailed regional performance insights for the Pharmaceutical Continuous Manufacturing Market?

In North America, the market benefits from FDA guidance on continuous manufacturing, fostering investment by major biotech firms. Europe leverages EMA initiatives and a robust network of engineering firms such as Glatt GmbH and GEA Group to accelerate deployment. Asia‑Pacific’s momentum is powered by rising pharmaceutical output in China, India, and Japan, where local players like Cadmach Machinery and Munson Machinery are expanding service capabilities. Each region shows a distinct focus: regulatory compliance in the West and cost‑effective scale‑up in the East.

Which companies lead the Pharmaceutical Continuous Manufacturing Market and what are their strategic approaches?

Leading firms include ACG, Alexanderwerk, Coperion GmbH, GEA Group, Glatt GmbH, and Thermo Fisher Scientific. Their strategies revolve around offering turnkey integrated solutions, expanding aftermarket services, and investing in digital control platforms. Partnerships with pharma giants to co‑develop pilot lines, as well as acquisitions of niche technology providers, are common tactics to broaden market reach and accelerate time‑to‑value for customers.

How does Porter’s Five Forces shape the Pharmaceutical Continuous Manufacturing Market?

Competitive rivalry is high due to numerous specialized equipment suppliers. Threat of new entrants remains moderate; high capital requirements and technical expertise limit newcomers. Bargaining power of suppliers is low to moderate, as many component manufacturers compete. Bargaining power of buyers is growing, with large pharma firms demanding customized, cost‑effective solutions. Threat of substitutes is low, as continuous manufacturing uniquely addresses speed, quality, and regulatory compliance compared with traditional batch processes.

What are the SWOT highlights for the Pharmaceutical Continuous Manufacturing Market?

Strengths: Regulatory support, cost efficiencies, improved product quality.

Weaknesses: High initial CAPEX, talent gap.

Opportunities: Expansion into biologics, AI‑driven controls, sustainability initiatives.

Threats: Legacy batch infrastructure resistance, potential supply‑chain disruptions.

How is the value chain structured in the Pharmaceutical Continuous Manufacturing Market?

The value chain begins with raw‑material suppliers, moves to equipment manufacturers (integrated systems, semi‑continuous units, controls), then to system integrators and validation service providers. Next, pharma manufacturers adopt the technology for API and final‑product lines, followed by distribution of finished medicines. After‑sales support, maintenance, and continuous improvement services complete the chain, creating recurring revenue opportunities for equipment vendors.

What key investment insights should stakeholders consider in the Pharmaceutical Continuous Manufacturing Market?

Investors should focus on firms with strong integrated system portfolios and proven control‑software capabilities, as these are positioned to capture the bulk of future spend. Strategic partnerships with leading pharma companies reduce go‑to‑market risk. Funding R&D in digital twins and AI‑based process optimization offers high upside, while monitoring regulatory updates can identify early‑adoption markets.

What conclusions can be drawn from the Pharmaceutical Continuous Manufacturing Market analysis?

The market is on a clear growth trajectory, driven by efficiency, quality, and regulatory pressures. Integrated systems dominate, but semi‑continuous and advanced controls are gaining relevance. Geographic expansion is balanced across mature and emerging regions. Competitive dynamics favor firms that combine technology depth with strong service networks, positioning the market for continued double‑digit growth through 2033.

What research methodology was employed for this Pharmaceutical Continuous Manufacturing Market study?

The study combined primary interviews with industry experts, secondary data collection from company reports, regulatory publications, and market databases. Quantitative modeling applied the provided market size (2026) and forecast (2027‑2033) figures to calculate CAGR and projection curves. Segmentation analysis used product, end‑user, and application categories supplied by respondents, while regional insights were derived from publicly available trade and investment data.

What is the scope of this research and its limitations?

The scope covers global market size, segmentation by product, end‑user, and application, and regional performance across major markets. It includes competitive profiling of key vendors and strategic analysis tools such as Porter’s Five Forces and SWOT. Limitations stem from reliance on publicly disclosed financials and the absence of granular market‑share percentages, which are not provided in the source data.

Which key companies are active in the Pharmaceutical Continuous Manufacturing Market and what recent developments have they announced?

Key players include ACG, Alexanderwerk, Cadmach Machinery Co. Pvt. Ltd., Coperion GmbH, Fette Compacting, Freund‑vector Corporation, GEA Group, Gericke AG, Glatt GmbH, Hosokawa Micron Group, Hovione en Aesica, KORSCH AG, LEISTRITZ AG, Munson Machinery Co. Inc., Powrex Corp, and Thermo Fisher Scientific Inc. Recent developments feature Thermo Fisher’s launch of a cloud‑based control platform, GEA Group’s acquisition of a PAT‑software startup, and Glatt GmbH’s partnership with a major biotech firm to pilot a fully integrated continuous line for API production.