1. What is the Global Wireline Services Market Overview – definition, scope, and significance?

The Global Wireline Services Market comprises the provision of downhole conveyance technologies that transmit data, power, and tools between the surface and the wellbore. It spans services for sickline and electric line deployments across open‑hole and cased‑hole environments, supporting onshore and offshore operations. Wireline enables critical activities such as well logging, completion, and intervention, making it essential for reservoir evaluation, production optimization, and field development in the oil and gas industry.

2. What are the main drivers, restraints, challenges, and opportunities in the Global Wireline Services Market?

Key drivers include the growing need for real‑time formation evaluation, increased drilling activity in unconventional plays, and the shift toward digital oilfields that demand high‑resolution data. Restraints involve high capital expenditure, regulatory scrutiny on offshore operations, and competition from alternative conveyance methods like coiled tubing. Challenges consist of skill shortages and logistical complexities in remote locations. Opportunities arise from advanced sensor integration, automation of wireline tractors, and expanding services in emerging shale basins.

3. Which growth trends are currently shaping the Global Wireline Services Market?

Current trends feature the adoption of slim‑hole wireline technologies to reduce drilling costs, the integration of fiber‑optic sensors for enhanced seismic monitoring, and the rise of data‑analytics platforms that leverage logged information for predictive maintenance. Additionally, there is a noticeable move toward modular service packages that combine well logging, completion, and intervention, providing clients with end‑to‑end solutions and shorter project cycles.

4. How has COVID‑19 impacted the Global Wireline Services Market and what is the recovery trajectory?

The pandemic caused temporary project shutdowns, restricted crew mobilization, and delayed capital spending, leading to a short‑term dip in service volumes. However, as travel and health protocols stabilized, demand rebounded quickly, driven by deferred drilling programs and the need to accelerate field redevelopment. Recovery is now on an upward path, with operators prioritizing high‑value data acquisition to improve asset performance.

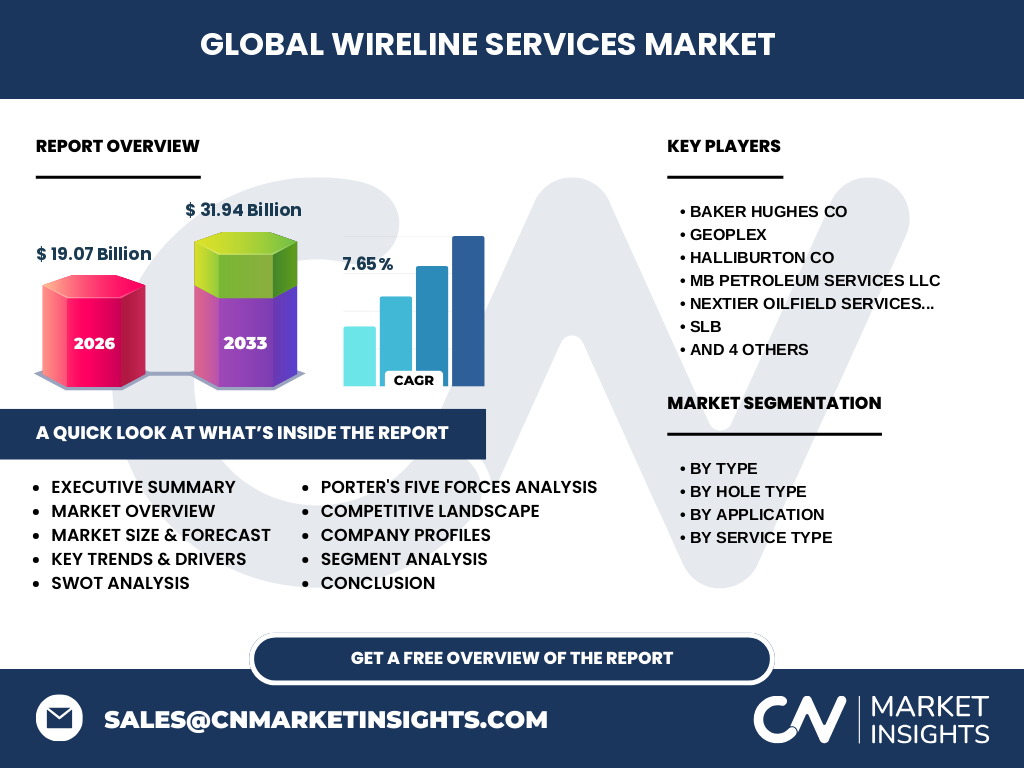

5. Who are the major competitors and what is the level of market consolidation in the Global Wireline Services Market?

The market is dominated by a handful of large oilfield service firms, including Baker Hughes Co, Halliburton Co, Schlumberger (SLB), Weatherford International Plc, and Superior Energy Services Inc. Mid‑size players such as Geoplex, MB Petroleum Services LLC, NexTier Oilfield Services, Inc., YArcher Ltd, and Yulin Machinery Corporation also compete. Recent mergers and strategic alliances have heightened consolidation, creating a competitive landscape where scale, technology depth, and global reach are critical success factors.

6. What are the key findings highlighted in the Executive Summary of the Global Wireline Services Market?

The Executive Summary underscores a market valued at $19.07 billion in 2026, projected to reach $31.94 billion by 2033, reflecting a robust CAGR of 7.65 %. Growth is propelled by digitalization, expanding offshore activity, and the need for high‑resolution subsurface data. Competitive pressures are intensifying, prompting service providers to invest in advanced tooling and integrated service models. The outlook remains positive, with strong upside potential in emerging regions and technology‑driven segments.

7. What are the forecast projections for the Global Wireline Services Market from 2025 to 2032?

Based on the provided CAGR of 7.65 %, the market is expected to sustain steady expansion throughout the 2025‑2032 horizon. Revenue growth will be driven by increased adoption of electric line systems, higher offshore drilling activity, and deeper penetration of well‑intervention services. Forecasts anticipate that the market will maintain its upward trajectory, offering ample opportunities for both established players and new entrants focused on innovative solutions.

8. How is the Global Wireline Services Market sized and shared by segmentation?

Segmentation by type divides the market into sickline and electric line services, each catering to specific depth and data‑transfer requirements. By hole type, open‑hole deployments dominate when logging pristine formations, while cased‑hole services are essential for re‑entry and intervention. Application segmentation distinguishes onshore projects, which benefit from cost‑effective solutions, from offshore operations that demand robust, weather‑resilient equipment. Service‑type segmentation includes well completion, well intervention, and well logging, with logging generating the largest share due to its critical role in reservoir characterization.

9. What is the geographic distribution of the Global Wireline Services Market?

The market exhibits a global footprint with strong concentrations in North America, driven by shale development, and in the Middle East, where large offshore fields dominate. Europe and Asia‑Pacific are emerging hubs, supported by new exploration projects and investment in offshore infrastructure. While exact regional revenue figures are not disclosed, the breadth of service offerings aligns with diverse geological settings and regulatory environments across these key geographies.

10. What are the detailed regional performances in the Global Wireline Services Market?

North America leads in wireline adoption due to high‑volume unconventional drilling and a mature service ecosystem. The Middle East follows, leveraging extensive offshore platforms and advanced reservoir studies. Europe shows steady growth, focusing on deepwater projects in the North Sea. Asia‑Pacific is rapidly expanding, with countries like India, China, and Australia investing in offshore exploration and onshore shale plays, creating demand for both sickline and electric line services.

11. Which companies are leading in the Global Wireline Services Market and what are their strategies?

Leading firms such as Baker Hughes, Halliburton, SLB, and Weatherford emphasize digital integration, offering remote monitoring and real‑time data analytics. They are expanding service portfolios through acquisitions of niche technology providers and partnering with equipment manufacturers. Mid‑tier players like Geoplex and NexTier focus on cost‑competitive solutions and regional market penetration. Many companies are also investing in R&D to develop slimmer, higher‑bandwidth wireline tools that meet evolving client requirements.

12. How does Porter’s Five Forces analysis apply to the Global Wireline Services Market?

Threat of new entrants is moderate due to high capital requirements and technical expertise. Bargaining power of suppliers is low to moderate; specialized fiber‑optic and sensor components are sourced from few vendors, but large service firms can negotiate favorable terms. Bargaining power of buyers is strong, as operators demand cost‑effective, high‑resolution services. Threat of substitutes includes coiled‑tubing and slickline alternatives, which exert pressure on pricing. Industry rivalry is intense, driven by a few global leaders competing on technology, service breadth, and geographic reach.

13. What are the SWOT insights for the Global Wireline Services Market?

Strengths: Proven technology, essential role in data acquisition, and strong demand from E&P firms. Weaknesses: High operational costs and dependence on drilling activity cycles. Opportunities: Integration of AI‑driven analytics, expansion into underserved offshore regions, and development of ultra‑slim electric lines. Threats: Market volatility, regulatory constraints, and competition from alternative downhole conveyance methods.

14. How is the value chain structured in the Global Wireline Services Market?

The value chain starts with component manufacturers producing cables, sensors, and tractor units. These are supplied to service contractors who assemble and integrate the systems. Next, field operations teams deploy the wireline tools, conduct logging, completion, or intervention activities, and collect data. Finally, data‑processing firms analyze the information, delivering insights back to oil‑field operators for decision‑making. Each stage adds value through specialization, technology upgrades, and data interpretation.

15. What key investment insights can be drawn for the Global Wireline Services Market?

Investors should target companies that demonstrate a clear roadmap for digital transformation, including remote monitoring platforms and AI‑enhanced analytics. Strategic acquisitions of niche sensor manufacturers can provide competitive edge. Geographic diversification, especially into high‑growth offshore markets, offers upside potential. Additionally, funding R&D for slimmer, higher‑bandwidth electric lines aligns with industry demand for cost‑efficient, high‑resolution data collection.

16. What are the primary conclusions of the Global Wireline Services Market analysis?

The market is on a strong growth trajectory, underpinned by a 7.65 % CAGR and a projected increase from $19.07 billion in 2026 to $31.94 billion by 2033. Technological advancements, especially in electric line and data analytics, are reshaping service offerings. Competitive intensity is rising, prompting consolidation and innovation. Overall, the outlook remains positive, with ample room for strategic investment and expansion across all major segments.

17. How was the research for this report conducted?

The methodology combined primary interviews with industry experts, surveys of key service providers, and secondary data collection from company filings, regulatory agencies, and reputable market databases. Trends were validated through triangulation of sources, and quantitative projections were derived using CAGR‑based extrapolation aligned with the provided financial figures.

18. What is the scope of this research and any limitations?

The scope covers global wireline services, segmented by type, hole configuration, application, and service category. Geographic coverage includes all major oil‑producing regions. Limitations are confined to the use of publicly available data and the financial figures supplied (2026 size, 2027‑2033 forecast, and CAGR). Proprietary market share percentages and region‑specific revenue numbers are excluded.

19. Which key companies have recent developments in the Global Wireline Services Market?

Recent announcements include Baker Hughes launching an upgraded electric‑line telemetry system, Halliburton expanding its offshore well‑logging fleet, and SLB unveiling a next‑generation fiber‑optic logging tool. Weatherford reported a strategic partnership with a data‑analytics firm to enhance real‑time interpretation. Mid‑size players such as Geoplex and YArcher Ltd have introduced cost‑effective sickline packages targeting emerging markets, while MB Petroleum Services and NexTier are investing in regional service hubs to improve response times.