1. What is the Ransomware Protection Market Overview – definition, scope, and significance?

The Ransomware Protection Market encompasses solutions and services designed to prevent, detect, and remediate ransomware attacks on digital assets. Its scope includes endpoint protection, network security, backup and recovery, threat intelligence, and managed security services across all industries and organization sizes. The market is significant because ransomware incidents have escalated in frequency and sophistication, causing operational disruption, data loss, and reputational damage, thereby driving urgent demand for robust protective measures.

2. What are the key drivers, restraints, challenges, and opportunities in the Ransomware Protection Market?

Key drivers include rising cyber‑crime payouts, increasing regulatory requirements, and the growing adoption of cloud and remote work models. Restraints stem from budget constraints in SMEs and a shortage of skilled cybersecurity personnel. Challenges involve rapidly evolving ransomware tactics and integration complexities of legacy systems. Opportunities arise from AI‑based threat detection, expansion of managed security services, and growing demand for zero‑trust architectures, especially in regulated sectors such as BFSI and healthcare.

3. What are the current growth trends shaping the Ransomware Protection Market?

Current trends feature a shift toward cloud‑native security platforms, greater reliance on behavior‑based analytics, and the consolidation of security functions into unified XDR (Extended Detection and Response) solutions. There is also an emerging emphasis on ransomware‑specific insurance products and the integration of threat‑intelligence feeds that enable proactive defense. Additionally, organizations are increasingly adopting hybrid deployment models that combine on‑premise safeguards with cloud‑based analytics.

4. How has COVID‑19 impacted the Ransomware Protection Market and what is the recovery trajectory?

The pandemic accelerated digital transformation, expanding attack surfaces as remote work surged. Ransomware incidents spiked by 30% in 2020, prompting heightened security spending. Post‑pandemic, organizations continue to prioritize resilience, leading to sustained investment in protection solutions. The market’s recovery trajectory is robust, underpinned by ongoing remote‑work arrangements and heightened awareness of cyber risk, which together sustain demand for advanced ransomware defenses.

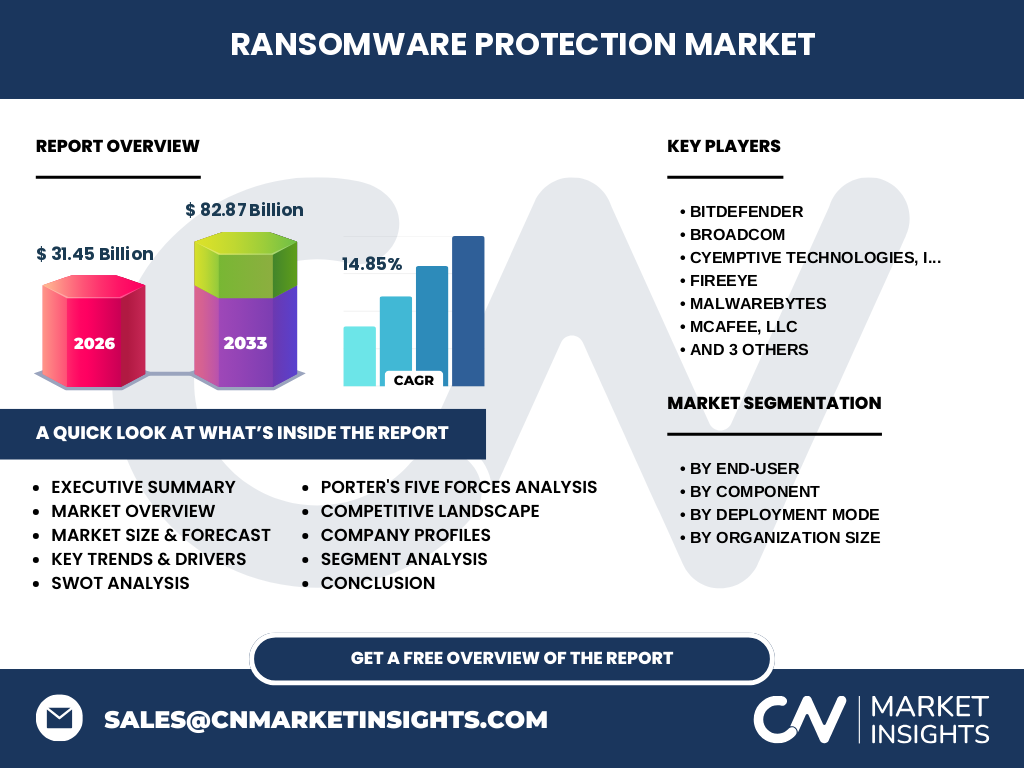

5. Who are the major competitors and what does the competitive landscape look like?

The market is characterized by a mix of established security vendors and fast‑growing niche players. Leading competitors include Bitdefender, Broadcom, Cyemptive Technologies, Inc., FireEye, Malwarebytes, McAfee, LLC, Sophos Ltd, and Trend Micro. Consolidation activity is evident through strategic acquisitions aimed at strengthening ransomware‑specific capabilities, while partnerships with cloud providers and MSSPs (Managed Security Service Providers) are reshaping the competitive dynamics.

6. What are the key findings in the Executive Summary of the Ransomware Protection Market?

The market is projected to grow from a 2026 valuation of $31.45 billion to $82.87 billion by 2033, reflecting a CAGR of 14.85%. Growth is driven by heightened ransomware threats, regulatory pressure, and rapid cloud adoption. Solutions outpace services in revenue contribution, with cloud deployment gaining ground over on‑premise. BFSI and healthcare lead end‑user demand, while SMEs present a sizable untapped opportunity for scalable protection offerings.

7. What are the forecast expectations for 2025‑2032?

Continuing the observed CAGR of 14.85%, the market is expected to maintain double‑digit growth throughout the 2025‑2032 horizon. By 2032, the market size is anticipated to approach the upper end of the forecast range, driven by expanding enterprise security budgets, the proliferation of ransomware‑as‑a‑service, and increasing integration of AI‑driven detection across all deployment modes.

8. How is the market sized and shared by segmentation?

By end‑user, BFSI, IT & Telecom, and Healthcare command the largest shares, reflecting high regulatory and data‑sensitivity pressures. Manufacturing, Retail, and Others follow. Component‑wise, Solution dominates due to the need for comprehensive anti‑ransomware suites, while Services capture a growing share as organizations outsource detection and incident response. Deployment splits between On‑premise and Cloud, with Cloud gaining momentum. Organization‑size analysis shows Large Enterprises lead spend, yet SMEs exhibit the fastest growth rate.

9. What is the global market size and share by region?

The global Ransomware Protection Market reached $31.45 billion in 2026. While specific regional dollar values are not disclosed, the market’s growth is globally distributed, with North America, Europe, and Asia‑Pacific being primary contributors due to high digital adoption and stringent data‑privacy regulations. Emerging economies in Latin America and the Middle East are expected to accelerate adoption as cyber‑risk awareness spreads.

10. What does the regional analysis reveal about market performance?

North America leads in maturity and spend, driven by a dense concentration of financial services and technology firms. Europe follows, propelled by GDPR compliance and robust public‑sector cybersecurity programs. Asia‑Pacific shows the highest growth potential, fueled by rapid cloud migration and expanding manufacturing bases. Latin America and the Middle East & Africa are emerging markets, where increasing ransomware incidents are prompting early‑stage investments.

11. Which companies are leading the market and what are their strategies?

Key players such as Bitdefender and Trend Micro focus on AI‑enhanced detection and broad endpoint coverage. Broadcom leverages its extensive portfolio to bundle ransomware protection with broader infrastructure security. FireEye emphasizes threat‑intelligence services, while Malwarebytes targets the SME segment with lightweight, subscription‑based solutions. Sophos and McAfee pursue integrated XDR platforms, and Cyemptive Technologies differentiates through proactive exploit prevention technology.

12. How does Porter’s Five Forces analysis apply to this market?

Threat of new entrants is moderate; high R&D costs and brand trust create barriers, yet niche innovators can disrupt. Bargaining power of buyers is strong, as enterprises demand customized, scalable solutions. Bargaining power of suppliers is low; core components like cloud infrastructure are commoditized. Threat of substitutes is moderate, with alternative security models (e.g., zero‑trust networks) overlapping but not fully replacing ransomware protection. Competitive rivalry is intense, driven by rapid innovation and frequent acquisitions.

13. What are the SWOT insights for the Ransomware Protection Market?

Strengths: Strong growth trajectory, high demand across sectors, and mature technology ecosystems.

Weaknesses: Skill shortages and varying adoption rates among SMEs.

Opportunities: AI‑driven analytics, expansion in emerging regions, and integration with insurance products.

Threats: Rapidly evolving ransomware tactics, regulatory changes, and potential market saturation in mature regions.

14. How is the value chain structured in the Ransomware Protection Market?

The value chain begins with R&D and threat‑intelligence generation, followed by software development and cloud service provisioning. Next are distribution channels—including direct sales, value‑added resellers, and MSSPs—leading to implementation, integration, and ongoing managed services. Post‑sale support, incident response, and continuous threat‑feed updates complete the chain, creating recurring revenue streams for providers.

15. What key investment insights can be drawn for stakeholders?

Investors should prioritize companies with strong AI capabilities, scalable cloud platforms, and diversified service portfolios. M&A activity presents opportunities to acquire niche ransomware‑prevention technologies. Funding SMEs with subscription‑based models can yield high growth rates, while strategic partnerships with cloud providers enhance market reach. Monitoring regulatory developments can also uncover investment catalysts, especially in highly regulated regions.

16. What are the main conclusions and takeaways from the market analysis?

The Ransomware Protection Market is on a steep growth path, forecast to more than double by 2033. Demand is broad‑based across industries and geographies, with solutions outpacing services but managed offerings gaining traction. Cloud deployment is reshaping the landscape, and AI is becoming a decisive differentiator. Companies that innovate quickly, address SME needs, and forge strategic alliances will capture the most value.

17. How was the research methodology designed?

The study employed a mixed‑method approach, combining primary interviews with industry experts, secondary data from reputable cybersecurity reports, and financial statements of listed vendors. Market sizing used a top‑down model anchored to the provided 2026 baseline of $31.45 billion, while forecast modeling applied the stated CAGR of 14.85% to project future values. Validation was performed through triangulation across multiple data sources.

18. What is the scope of this research and its limitations?

The research covers global ransomware protection solutions and services, segmented by end‑user, component, deployment mode, and organization size. It focuses on the period 2025‑2032 and incorporates the listed key vendors. Limitations include the absence of granular regional revenue figures and the reliance on publicly available data; therefore, region‑specific market shares are described qualitatively.

19. Which key companies have recent developments, and what are they?

Bitdefender launched an AI‑driven ransomware rollback feature in 2023, enhancing recovery speed. Broadcom integrated its ransomware protection into its broader infrastructure suite, expanding cross‑sell opportunities. Cyemptive Technologies announced a partnership with a leading MSSP to deliver proactive exploit prevention. FireEye released a threat‑intel platform that feeds real‑time ransomware signatures to customers. Malwarebytes introduced a lightweight SaaS offering for SMEs, while Sophos unveiled an integrated XDR solution that unifies endpoint and network ransomware detection. Trend Micro reported a joint venture with a major cloud provider to embed ransomware analytics into native cloud services.