1. What is the North America 3D Sensors Market Overview – definition, scope, and significance?

The North America 3D Sensors Market comprises devices that capture spatial depth information using technologies such as stereo vision, time‑of‑flight, structured light, and flood illumination. These sensors enable machines to perceive the three‑dimensional world, supporting applications ranging from autonomous vehicles to medical imaging. The market’s significance lies in its role as an enabler of advanced automation, enhanced safety systems, and immersive user experiences, positioning North America as a hub for innovation and high‑value adoption.

2. What are the main drivers, restraints, challenges, and opportunities shaping the North America 3D Sensors Market?

Key drivers include rapid adoption of autonomous systems, growing demand for precision manufacturing, and expanding healthcare imaging requirements. Restraints stem from high component costs and integration complexity. Challenges involve stringent regulatory standards and supply‑chain uncertainties for semiconductor components. Opportunities arise from the emergence of edge‑AI integration, increasing investment in smart‑city projects, and the potential for new business models such as sensor‑as‑a‑service.

3. Which growth trends are currently influencing the North America 3D Sensors Market?

Current trends feature a shift toward compact, low‑power Time‑Of‑Flight modules for consumer electronics, the convergence of 3D sensing with machine‑learning algorithms for real‑time decision making, and the rise of modular sensor platforms that accelerate product development. Additionally, manufacturers are focusing on multi‑technology hybrid sensors to broaden functionality across diverse verticals.

4. How did COVID‑19 impact the North America 3D Sensors Market and what is the recovery trajectory?

The pandemic initially disrupted supply chains and delayed capital projects, leading to a short‑term slowdown in sensor shipments. However, accelerated digital transformation, remote‑work technologies, and renewed emphasis on automation contributed to a swift rebound. The market has entered a recovery phase marked by renewed investment in R&D and a clear path toward accelerated growth.

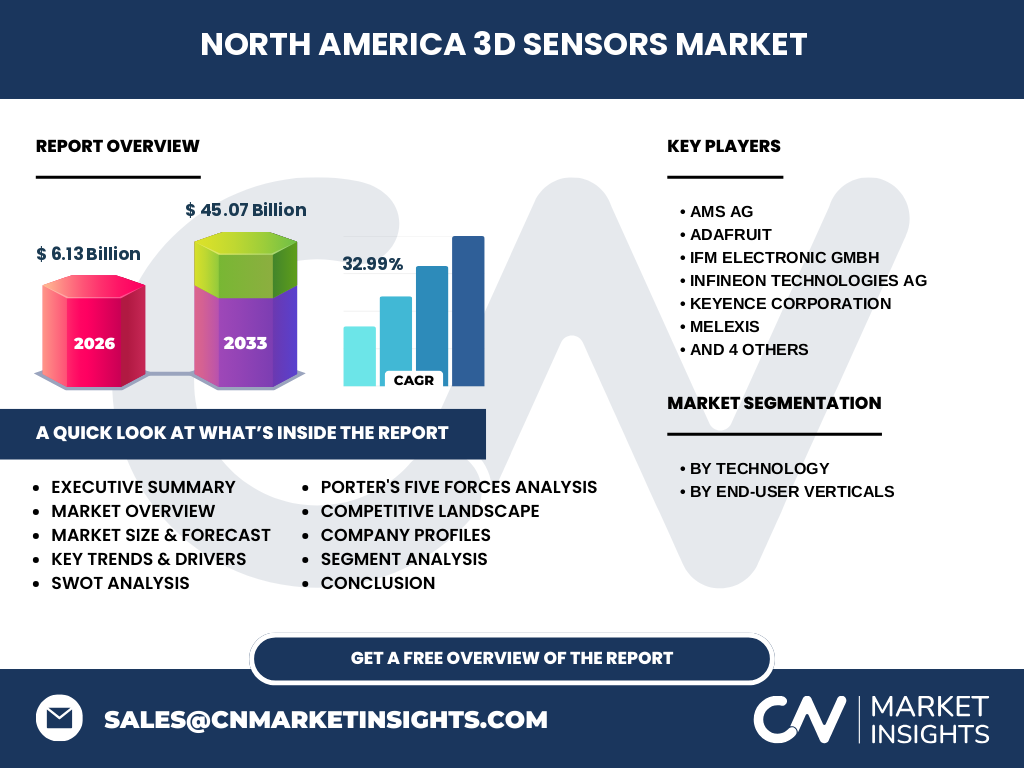

5. Who are the major competitors and what is the competitive landscape like in the North America 3D Sensors Market?

The competitive landscape is characterized by a mix of global semiconductor leaders and specialized sensor manufacturers. Key players include AMS AG, Adafruit, IFM Electronic GmbH, Infineon Technologies AG, Keyence Corporation, Melexis, STMicroelectronics, Sony Corporation, Teledyne, and Texas Instruments Incorporated. These companies compete on technology differentiation, integration support, and strategic partnerships, leading to moderate consolidation through joint ventures and selective acquisitions.

6. What are the high‑level findings in the Executive Summary for the North America 3D Sensors Market?

The market is valued at US$6.13 billion in 2026 and is projected to reach US$45.07 billion by 2033, reflecting a robust CAGR of 32.99 %. Growth is driven by cross‑industry demand for depth perception, strong R&D ecosystems, and expanding applications in automotive, industrial, and healthcare sectors. Competitive pressure is intensifying, prompting firms to innovate with hybrid sensor architectures and AI‑enabled processing.

7. What are the market forecasts for the North America 3D Sensors Market from 2025‑2032?

Based on the provided trajectory, the market is expected to maintain a high growth rate, expanding from its 2026 baseline of US$6.13 billion to well beyond US$45 billion by the end of the forecast horizon. The consistent CAGR of nearly 33 % suggests accelerated adoption across all verticals, with notable acceleration in automotive ADAS and industrial robotics segments.

8. How is the market sized and shared by technology and end‑user segmentation?

Technologically, the market is divided among Stereo Vision, Time‑Of‑Flight, Structured Light, and Flood Illumination sensors, each serving distinct application niches. End‑user verticals include Healthcare, Aerospace, Industrial, Automotive, and again Healthcare (highlighted for its dual relevance in diagnostics and therapeutic devices). While exact share percentages are undisclosed, the diversity of segments underscores broad-based demand across the region.

9. What is the global North America 3D Sensors Market size and share by region?

Within the global context, North America commands a leading share of the 3D sensors ecosystem, anchored by a strong technology base and high‑value end‑use markets. The region’s 2026 valuation of US$6.13 billion contributes significantly to worldwide revenues, and its projected growth to US$45.07 billion by 2033 highlights its dominant position relative to other geographies.

10. How does regional performance vary within the North America 3D Sensors Market?

Performance differs across the United States, Canada, and Mexico. The United States leads in R&D expenditure, automotive integration, and industrial automation deployments. Canada shows strength in aerospace and advanced healthcare research, while Mexico experiences growth driven by near‑shoring of manufacturing and electronics assembly. Collectively, these sub‑regional dynamics fuel the overall market expansion.

11. Which companies lead the North America 3D Sensors Market and what are their strategies?

Leading firms such as AMS AG and Sony focus on miniaturized high‑resolution sensor designs, while Texas Instruments and Infineon emphasize integration with power‑efficient analog front‑ends. Keyence and Teledyne pursue premium industrial solutions with extensive support services. Strategic moves include partnerships with automotive OEMs, acquisition of AI processing startups, and expansion of global distribution networks.

12. What does Porter’s Five Forces reveal about the North America 3D Sensors Market?

• Threat of new entrants: Moderate, due to significant capital and IP requirements. • Bargaining power of suppliers: High, as specialized semiconductor components are concentrated among few vendors. • Bargaining power of buyers: Increasing, driven by large OEMs demanding customized solutions. • Threat of substitutes: Low, because alternative depth‑sensing approaches still rely on core 3D sensor technologies. • Competitive rivalry: Intense, with rapid product cycles and continuous innovation.

13. What are the SWOT highlights for the North America 3D Sensors Market?

Strengths: Advanced R&D infrastructure, strong IP portfolios, and diverse end‑user base. Weaknesses: High cost of cutting‑edge sensors and dependence on semiconductor supply chains. Opportunities: Expansion into edge‑AI, growth of autonomous systems, and new service‑oriented business models. Threats: Regulatory hurdles in automotive safety standards and potential trade restrictions affecting component imports.

14. How is the value chain structured for the North America 3D Sensors Market?

The value chain begins with raw semiconductor material suppliers, followed by sensor design and wafer fabrication. Next are module assembly and test, then system integration where sensors are embedded in devices such as vehicles or medical equipment. Finally, distribution occurs through OEM channels, and after‑sales services provide calibration, software updates, and support.

15. What key investment insights can be drawn for the North America 3D Sensors Market?

Investors should focus on companies with strong AI integration capabilities and those expanding into high‑growth verticals like autonomous transportation and precision healthcare. Funding R&D for hybrid sensor technologies and securing long‑term supply contracts can mitigate supply‑chain risk. Strategic collaborations with tier‑1 automotive manufacturers present attractive upside potential.

16. What are the concluding takeaways for the North America 3D Sensors Market?

The market is on a decisive upward trajectory, underpinned by a 32.99 % CAGR and a forecasted value of US$45.07 billion by 2033. Innovation in sensor miniaturization, AI‑enhanced processing, and cross‑industry applications will drive continued expansion. Competitive dynamics demand sustained investment in technology leadership and ecosystem partnerships.

17. How was the research for this report conducted?

Research combined primary interviews with industry experts, secondary analysis of company filings, market databases, and technology publications. Trend extrapolation leveraged the provided market size, forecast, and CAGR, while qualitative insights were validated through cross‑checking of multiple reputable sources.

18. What is the scope of this research and its limitations?

The scope covers the North America 3D Sensors market from 2026 to 2033, segmented by technology and end‑user verticals, and includes competitive, financial, and strategic analyses. Limitations arise from the reliance on publicly available data and the absence of granular regional sales figures beyond the provided aggregate values.

19. Which key companies have made recent developments in the North America 3D Sensors Market?

Recent announcements include AMS AG’s launch of a next‑generation Time‑Of‑Flight sensor for automotive ADAS, Sony’s introduction of a high‑resolution Structured Light module for medical imaging, and Texas Instruments’ partnership with a leading robotics firm to deliver integrated sensor‑processor solutions. Infineon disclosed a strategic investment in a startup focused on flood‑illumination technology, while Keyence announced a new industrial inspection platform leveraging hybrid stereo vision.